This article first appeared in Capital, The Edge Malaysia Weekly on January 8, 2024 - January 14, 2024

Construction

Overweight

RHB RESEARCH (JAN 3): The total value of projects awarded to contractors in 2023 stood at RM127.4 billion, 22% lower y-o-y than the RM163.2 billion in 2022, according to the Construction Industry Development Board. Nonetheless, we view this as a temporary blip — contract rollouts are expected to be backed by the government’s RM90 billion development expenditure (DevEx) allocated for 2024, with 21% of the DevEx focusing on the transport subsector compared with 18% in 2023.

Government projects awarded saw a 33% y-o-y drop in value in 2023, reaching RM29 billion. Among the types of projects, infrastructure recorded the largest annual drop in terms of project value at a y-o-y decline of 47%, followed by residential at a y-o-y drop of 37%. However, non-residential projects bucked the trend, rising 4% y-o-y to reach RM76.8 billion.

In 1H24, awards may pertain to flood mitigation projects, the Penang light rail transit (LRT), Pan Borneo Highway Sabah Phase 1B and the reinstatement of the five LRT3 stations. As for the Mass Rapid Transit 3 (MRT3), we take comfort that the government is going ahead with the land acquisition process for the project. According to MRT Corp, the notification of identified land is expected to start in 2Q24, with the finalisation of the land to be acquired taking place in 3Q24. Therefore, we assume that MRT3 contract awards could take place from 4Q24.

Upcoming catalysts for the sector include a higher participation of Malaysia-based contractors in Indonesia’s new capital project. So far, IJM Corp is eyeing the Nusantara state civil servant housing project, while several other Malaysian companies submitted letters of intent in 2022, which are being evaluated by the Nusantara Capital Authority. Another catalyst is a quicker-than-expected rollout for the proposed three lines of the Johor Bahru LRT.

The Bursa Malaysia Construction Index is trading at a PER of 13 times, slightly above its 10-year mean of 12.7 times. With commendable catalysts in store for the sector, we view the current valuation of the index to be undemanding and, as such, an attractive level to enter. Our top picks are Gamuda Bhd, Sunway Construction Group Bhd and Kerjaya Prospek Bhd.

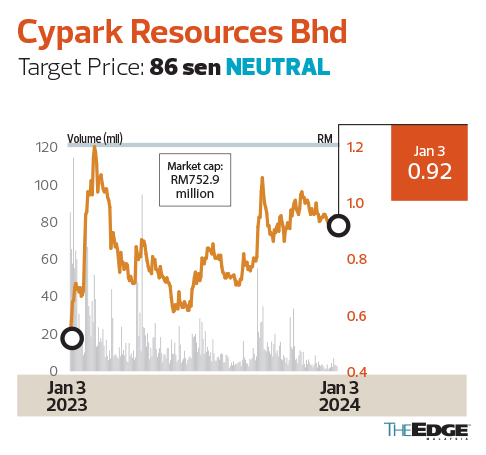

Cypark Resources Bhd

Target Price: 86 sen NEUTRAL

PUBLIC INVEST RESEARCH (JAN 2): Cypark reported a wider core net loss after tax and minority interest (Latami) of RM4.8 million in 2QFY24 from a core net Latami of RM2.3 million in 1QFY24. This was due to its waste-to-energy segment recording a wider loss before tax of RM9.1 million in 2QFY24, compared with an LBT of RM6.2 million in 1QFY24. The loss came on the back of lower sales of green energy arising from plant outages that required maintenance during the period. Management guided that the plant has resumed normal operations and is expected to reach maximum capacity soon. Nevertheless, we lower our forecast to reflect the gradual optimisation of the plant from its current state. On a positive note, discussions on the revision of the tipping fee have received a favourable response from the authorities, which will improve its margins and cash flow significantly upon approval.

Cypark has not changed the completion date of December 2023 for the Large-Scale Solar 2 and LSS3 projects. However, it had yet to declare a new commercial operation date at the time of writing. Therefore, we do not discount a slight delay in the completion date, although it has resumed active progress on both projects after an injection of funds from its new major shareholders via a perpetual sukuk.

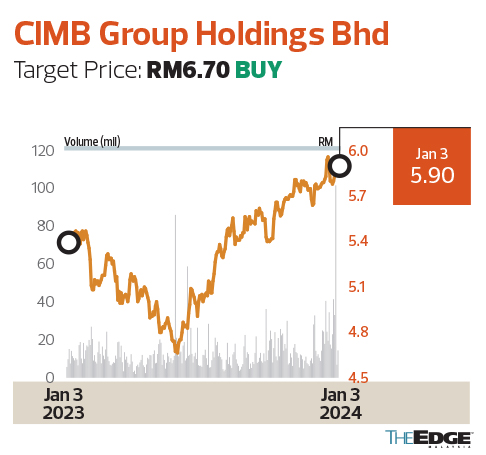

CIMB Group Holdings Bhd

Target Price: RM6.70 BUY

MAYBANK INVESTMENT BANK RESEARCH (JAN 1): CIMB has fully divested its remaining 25.01% and 25% shareholding in CGS-CIMB Securities International Pte Ltd (CSI) and CGS-CIMB Holdings Sdn Bhd (CCH) respectively to CGS International Holdings Ltd (CGSI; formerly known as China Galaxy International Financial Holdings Ltd). CIMB will receive about RM780 million from this sale, taking the total proceeds for the sale of its 100% original stockbroking business to about RM2.5 billion.

Investors will recall that in 2018, CIMB entered into a 50:50 partnership agreement with CGSI to operate a regional stockbroking business in Asia, through the sale of CIMB’s stockbroking business to the CGSI-CIMB JV. In December 2021, CIMB sold 24.99% and 25% of its shareholding in CSI and CCH respectively to CGSI, under the latter’s first call option. With this second disposal, CIMB will not have a stockbroking entity in the group for now, at least until the potential acquisition of KAF Equities is finalised.

We do not expect a profit-and-loss impact from this disposal as CIMB had fully recognised all potential gains earlier on. There could be some uplift to capital from the sale, but we expect this to be largely offset by the potential acquisition of KAF Equities.

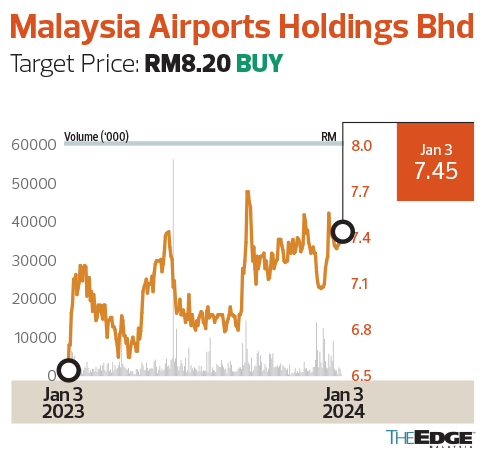

Malaysia Airports Holdings Bhd

Target Price: RM8.20 BUY

TA SECURITIES RESEARCH (JAN 2): MAHB recorded 6.6 million in passenger movements for its Malaysia operations in November, down 2.9% m-o-m but up 27.4% y-o-y. The growth in international traffic remained robust in November 2023, offsetting the seasonal weakness in domestic traffic. For 11M23, the growth in cumulative passenger movements in Malaysia moderated to 61.2% from 65.6% a month earlier, to 74.1 million. The continuous traffic growth in November was partly due to the introduction of four new services from the Kuala Lumpur International Airport to the UAE.

Malaysia’s domestic volume contracted 6.3% m-o-m to 3.2 million, slipping to 75% of 2019 levels. We believe the weakness was due to increased allocation of seat capacity to the international sector for higher fare and better yield by airline companies. For the international sector, the total passenger movements rose to 3.4 million in November, showing a steady recovery to 78% of 2019 levels.

For 2024, we have selected MAHB as one of our top picks as we believe the company will benefit from growing travel demand to China and Malaysia, thanks to the establishment of visa-free entry effective Dec 1, 2023.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.