KUALA LUMPUR (Jan 3): AmInvestment Bank Bhd has maintained its end-2024 target for the FBM KLCI at 1,545 points — higher than its 2023 close of 1,454.66 points — as it is optimistic about a better market close by the year end, driven by higher corporate earnings growth, enticing dividend yields, strong outlook for the Malaysian ringgit and renewed expectations for infrastructure expansion, supported by a firm government mandate.

However, the research house noted that the outlook of the local market will be tempered by the rising probability of a global recession from the aftermath of an extended 500 basis points (bps) US interest rate hike cycle, which will drive volatility across all markets.

“[We] maintain base-case end-2024 FBM KLCI target at 1,545, pegged to an unchanged 2024F P/E (price-earnings) of 14.9 times — at parity to its five-year median, albeit at three standard deviations below pre-pandemic 2017-2019 median of 17 times,” the research house said in a note.

AmInvestment has projected the benchmark indice’s corporate earnings in 2024 to grow by 14.4% — driven largely by oil and gas, plantation, power and financial services — comparable to Bloomberg consensus’ earnings growth of 13.6%.

In comparison with other Southeast Asian countries, Vietnam is expected to lead the pack with an impressive corporate earnings growth of 52%, followed by Indonesia (35%), Thailand (18%), and the Philippines (16%).

“For 2025F, we are projecting FBMKLCI earnings growth of 7.0% (versus Bloomberg’s 5.8%), anchored by financial services, oil and gas (O&G) and transportation,” said AmInvestment.

“Even so, we acknowledge that uncertain macro headwinds from global recessionary and inflationary prospects, coupled with the timing of the US Federal Reserve’s interest rate pivot this year, could lead to significant revisions to corporate earnings prospects,” it said.

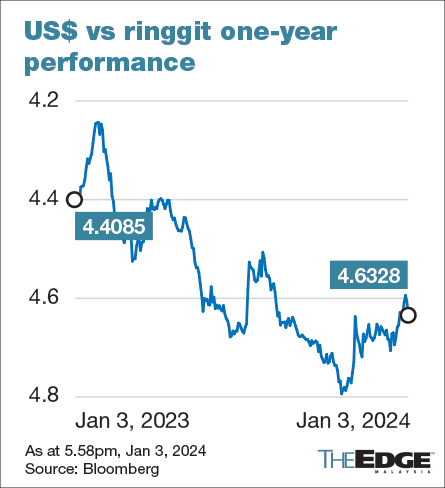

Soft landing baseline scenario, with ringgit to trade at 4.50

AmInvestment maintains its initial baseline scenario of a “soft-landing” for the US economy, though it notes an increased downside risk compared to earlier assessments. The research house opined that the probability of a rate cut occurring before mid-2024 is now less likely.

Moreover, it said the lag effects from the tightening measures should continue to surface in the coming months.

“Recall that the Fed has pushed the Fed Funds Rate to 5.25%-5.50%, reflecting 525 bps hikes since the monetary policy tightening campaign was initiated early last year.

“Where the USD/MYR is currently trading at, our economist has recently reinforced our 2024F year-end target of 4.50, as the US dollar weakness is expected to resurface once US economic indicators soften further, paving the way for a back-loaded rate cut,” it added.

Overweight on O&G, construction, technology, manufacturing, ports, power, property, REITs, gloves and transportation

AmInvestment has issued “overweight” recommendations for various sectors, namely O&G, construction, technology, manufacturing, ports, power, property, real estate investment trust (REIT), glove and transportation.

The research house’s top picks within these sectors include CIMB Group Holdings Bhd, RHB Bank Bhd, Tenaga Nasional Bhd, Telekom Malaysia Bhd, Gamuda Bhd, Dialog Group Bhd, Sunway Bhd, Yinson Holdings Bhd, Pavilion REIT, and Mah Sing Group Bhd.

“We also like small cap stocks with strong brand names which can safely navigate inflationary pressures, such as Spritzer and niche agrichemical producer Ancom Nylex Bhd, as well as grossly undervalued companies such as Deleum Bhd.

“Our ESG (environmental, social and governance) champions are Maybank (Malayan Banking Bhd), Petronas Chemicals Group Bhd, Petronas Gas Bhd, IHH Healthcare Bhd, Telekom Malaysia Bhd, Westports Holdings Bhd, Inari Amertron Bhd, Sunway Holdings, Sunway REIT (Real Estate Investment Trust) and Gamuda Bhd,” it said.

The research house highlighted the importance of sector and stock selection, stating that these decisions will play a crucial role in achieving relative outperformance. This strategic approach is seen as particularly important, in light of the increasing risks associated with a potential US-led global recession in the first half of 2024.

Additionally, the potential impact of subsidy rationalisation plans and slightly higher inflation on local consumption spending, will add further complexity to the investment landscape, it added.