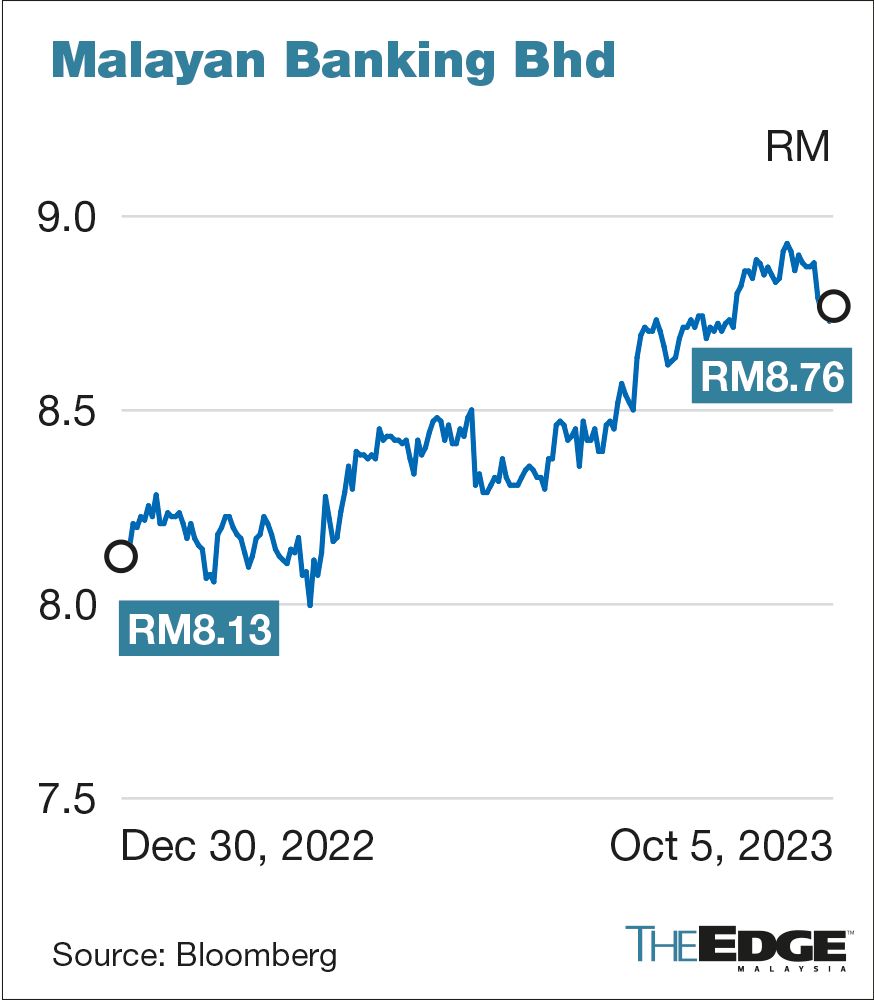

KUALA LUMPUR (Oct 5): After Malayan Banking Bhd's share price hit a record high last month, investors appear to be taking profit against the country's largest public-listed company amid growing concerns over the group’s rising costs while expectations of “higher and longer” global interest rates weigh on risk appetite towards the capital markets.

The stock’s adjusted closing price, which reached its highest of RM8.93 on Sept 18 after climbing 9.8% since the start of the year, has since pared some of these gains. On Thursday, the bank, largest in the country by asset size, closed at RM8.76, three sen or 0.3% higher than the day before, but 1.9% lower than its recent high.

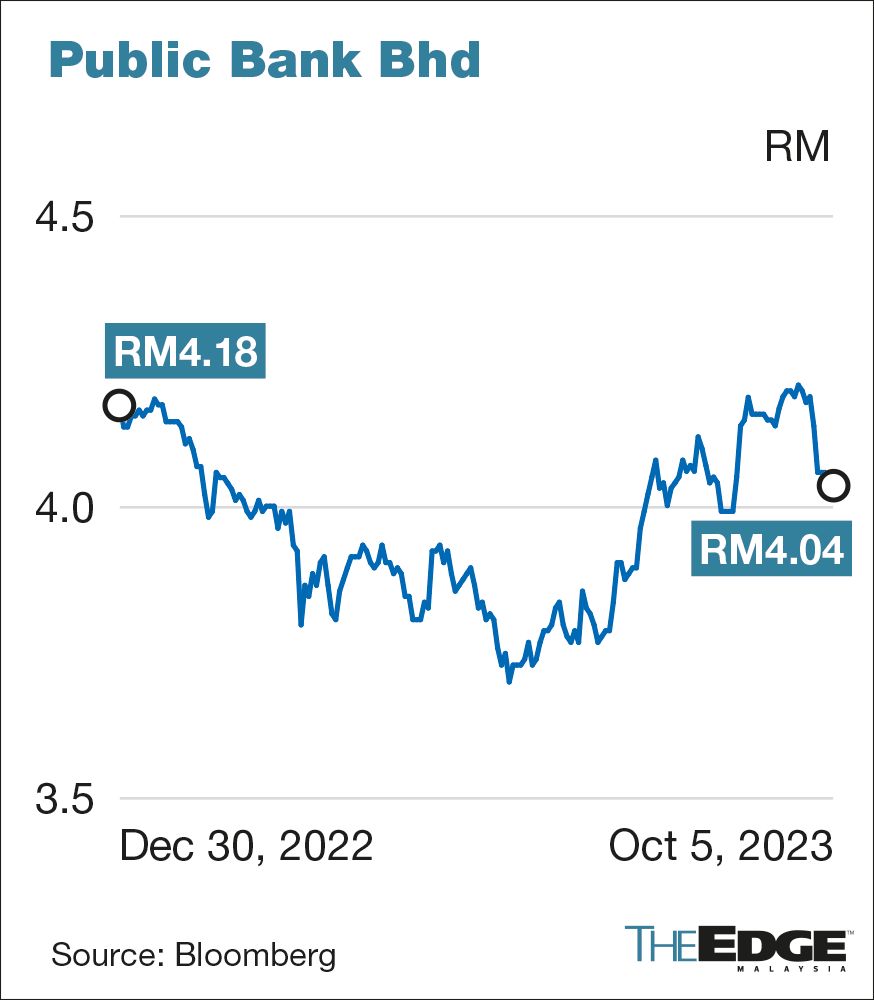

The latest valuation gave Maybank a market capitalisation of RM105.65 billion, still the most valuable stock on Bursa Malaysia, followed by its other large banking peers — Public Bank Bhd with RM78.42 billion and CIMB Group Holdings Bhd with RM57.7 billion.

Maybank’s recent share price weakness raises the question of whether a longer term downtrend has come, marking a more affordable entry-point into a famous dividend payer.

The bank recently declared its first interim dividend of 29 sen per share for the financial year ending Dec 31, 2023 (FY2023), more than the 28 sen it distributed a year ago.

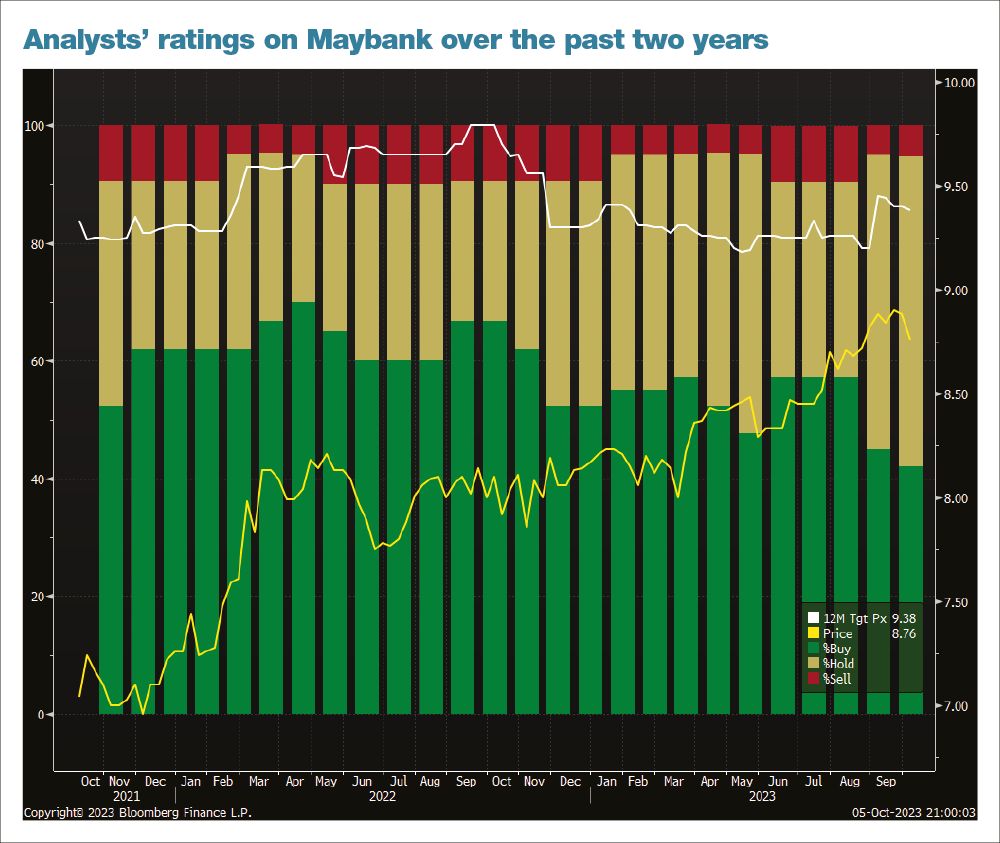

Analysts are mixed on Maybank’s prospects. Bloomberg shows the stock has eight 'buy' ratings, 10 'hold' recommendations and one 'sell', with target prices ranging between RM8 and RM10.50 for a consensus of RM9.38.

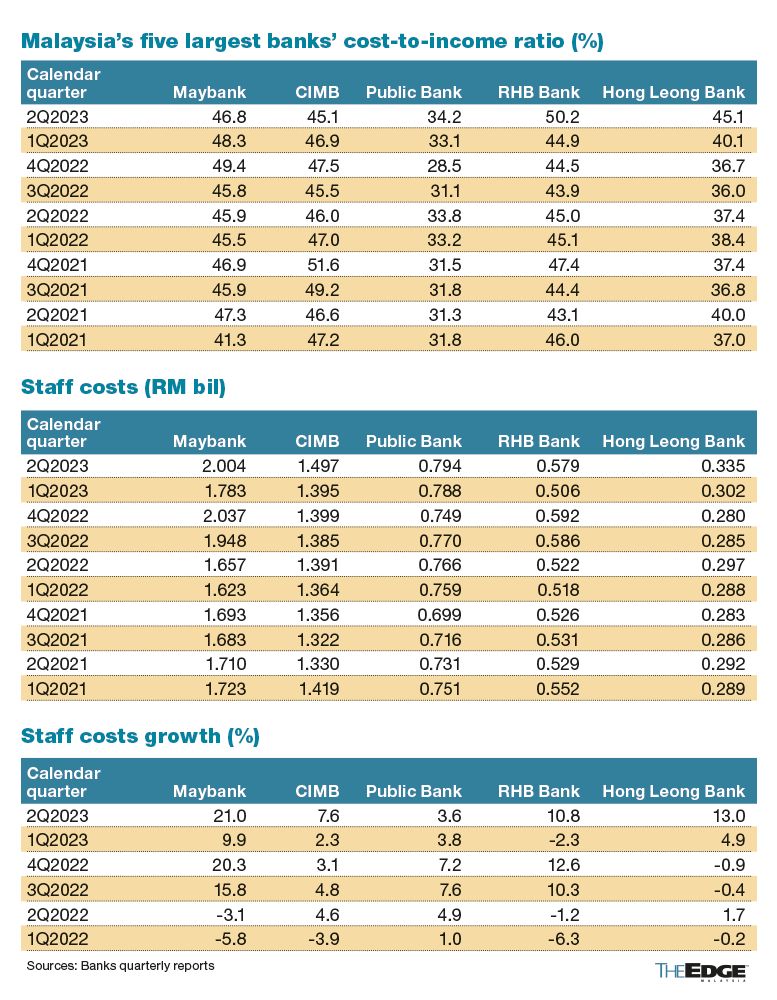

“CIMB used to incur a higher cost-to-income ratio (CIR) than Maybank. But in recent quarters, we noticed it has been the other way round. And if you look into their staff costs, not only is Maybank the highest among its peers, it is also growing at a higher pace,” said an analyst who declined to be named.

For the second quarter ended June 30, 2023 (2QFY2023), Maybank recorded a CIR of 46.8%, down from 48.3% in 1QFY2023 and 49.4% in 4QFY2022.

This compares to CIMB’s CIR of 45.1% in 2QFY2023, 46.9% in 1QFY2023 and 47.5% in 4QFY2022.

The most recent quarter when CIMB had a higher CIR than Maybank was in 2QFY2022.

“Maybank’s cost is rising even when they push back some of their scheduled investments from M25+, so we are expecting a more elevated cost level in the following years,” the analyst added.

Under its multi-year corporate strategy M25+, Maybank will invest between RM3.5 billion and RM4.5 billion within a five-year period, mainly to boost the group’s technology in banking infrastructure.

MIDF Research analyst Samuel Woo, who has Maybank on 'neutral' with a TP of RM9.28, said the bank's costs could come in lower-than-expected for FY2023, as its allocation for M25+ this year may not be fully used.

“Fundamentally, Maybank is intact — asset quality should not be too much of an issue, loan growth prospects in the second half are better and good non-interest income contribution should persist,” he told The Edge when contacted.

“[Management] said there is upside to Singapore loan growth, and there should be better corporate [loan] pipeline post-election, as with other banks,” he noted.

Hong Leong Investment Bank analyst Chan Jit Hoong, however, was more doubtful on Maybank’s prospects, though he noted its share price performance has been more resilient than its peers.

“Maybank’s 2QFY2023 [financial] performance was supported by NOII (non-interest income), driven by their treasury business, but it is unclear whether they can sustain, given the rising risk-free rate. Asset quality-wise, if cost of living continues to go up, [further] writebacks [of provision] can be quite far fetched in 2024,” he said.

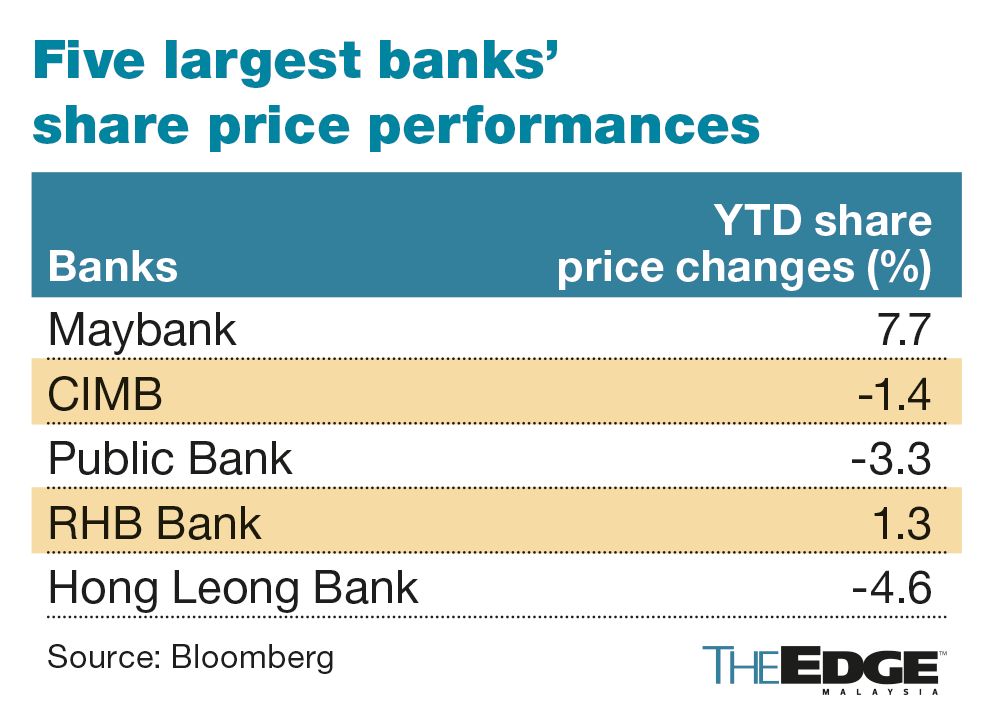

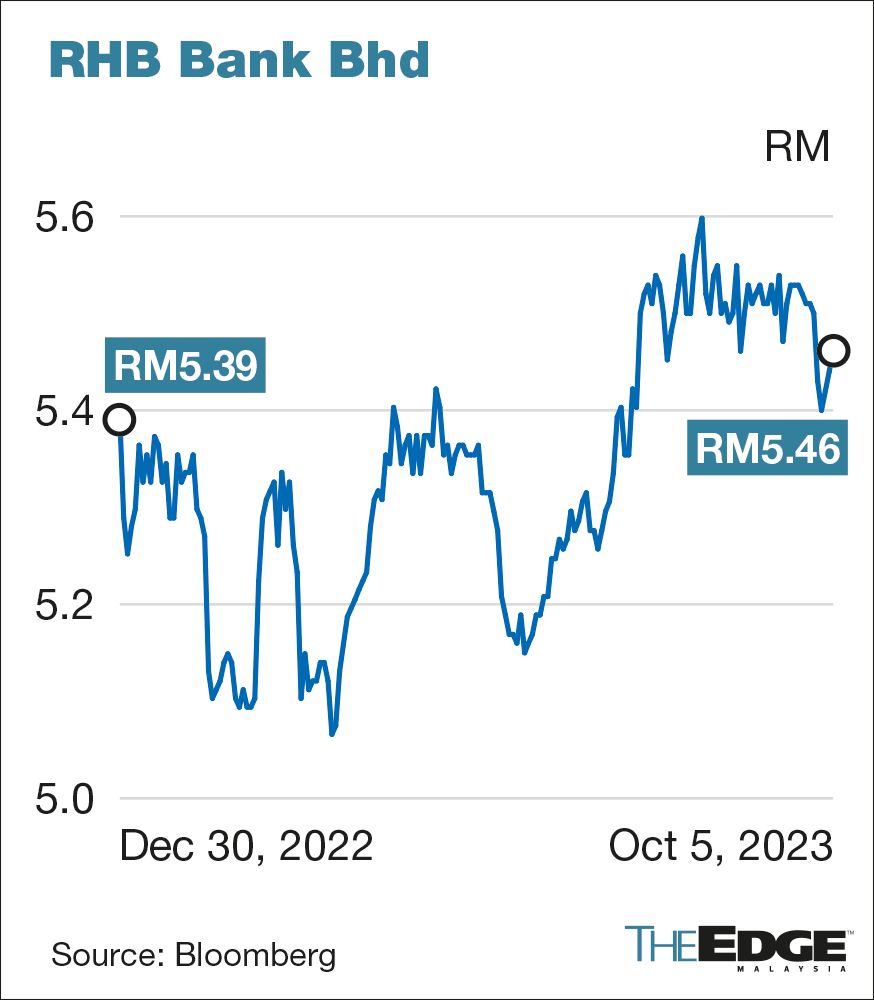

Year to date, Maybank has gained 7.7%, compared with CIMB's 1.4% decline and Public bank's 3.5% drop; RHB Bank is up 1.3% while Hong Leong Bank has fallen by 4.6%.

- Maybank customers can now make QR payments through MAE app in Cambodia

- Perak Sultan hails mosque, Hindu temple's inclusive aid for Putra Heights fire victims

- Malaysia to bear brunt of weaker exports to US, Macquarie flags

- U Mobile to roll out 5G network with Huawei, ZTE; sees 'similar' rates to DNB

- TNB bags RM705 mil maintenance contract from Kuwait’s Ministry of Electricity, Water and Renewable Energy

- European rating agency Scope sends US downgrade warning

- First phase of PKR election completed, focus shifts to second phase — Zaliha

- EU expects most US tariffs to stay as talks make little progress

- Scope Industries to exit manufacturing via RM96.7 mil sale of subsidiary

- Trump threatens Harvard’s tax-exempt status after school’s rebuke