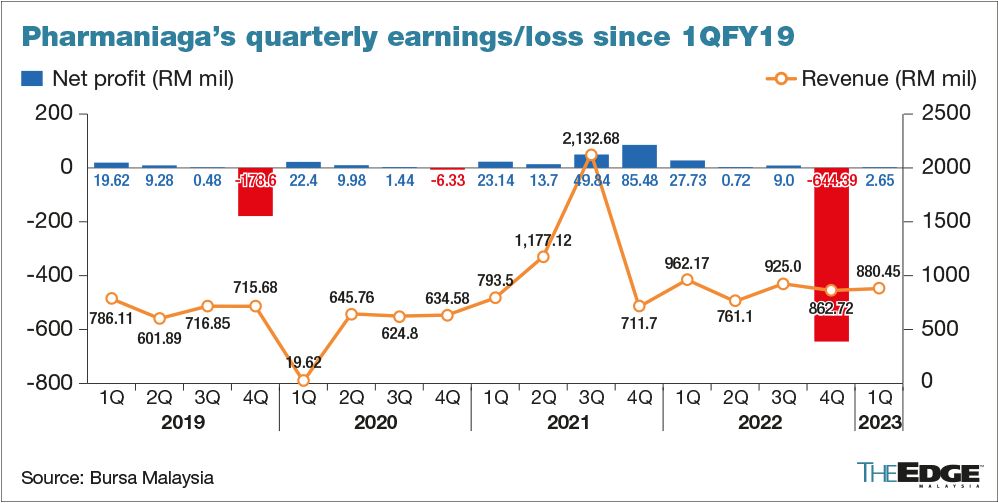

KUALA LUMPUR (May 18): Pharmaniaga Bhd’s net profit plunged to RM2.65 million in the first quarter ended March 31, 2023 (1QFY2023), barely 10% of the RM27.73 million it made a year earlier.

The latest figures were also a far cry from its pre-pandemic levels. Pharmaniaga posted a net profit of RM19.6 million in 1QFY2019 on a revenue of RM786.1 million.

The public hospitals’ generic drug supplier attributed the big earnings contraction to lower customer demand in both its concession and Indonesia operations. On top of that, it incurred higher financial cost as a result of the increase in the Overnight Policy Rate.

Quarterly revenue fell 8.5% to RM880.45 million from RM962.17 million in 1QFY2022.

“The higher revenue in the previous year's corresponding quarter (1QFY2022) was primarily due to a surge in demand following the resumption of normal business operations post-pandemic.

“However, the demand has levelled off in 2023, and the group was able to generate substantial revenue despite the challenging market conditions,” said Pharmaniaga, which suffered a massive RM552.3 million impairment of its Covid-19 vaccine inventory and a RM50.3 million write-down of goodwill for its Indonesia manufacturing unit in the preceding quarter.

Earnings per share came in sharply lower at 0.20 sen in 1QFY2023 compared with 2.12 sen for 1QFY2022, according to its bourse filing.

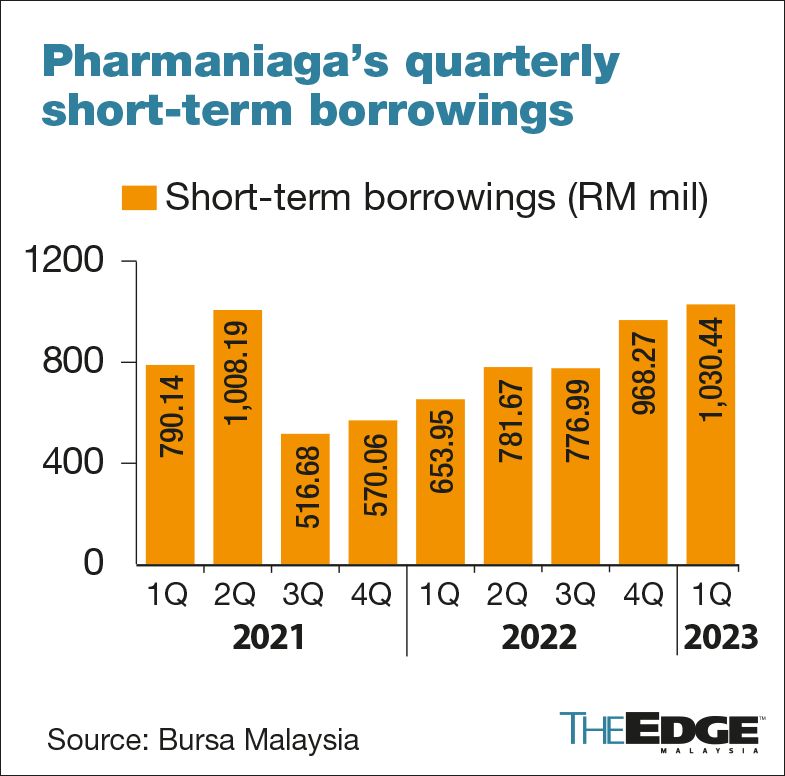

The group’s balance sheet, as at March 31, shows that its short-term borrowings, which would be due within six months, ballooned to RM1.03 billion from RM968.27 million as at Dec 31, 2022. Its long-term borrowings increased to RM222.78 million from RM190.63 million.

Pharmaniaga’s receivables expanded to RM552.36 million from RM351.66 million as at Dec 31, 2022. Its cash balance increased slightly to RM56.62 million from RM52,84 million a year ago but it had a net negative operating cash flow of RM65.63 million during the quarter under review. Meanwhile, its inventory dropped to RM732.51 million from RM 767.26 million previously.

On a quarter-on-quarter (q-o-q) basis, Pharmaniaga posted a net profit in 1QFY2023 from a net loss of RM644.39 million in 4QFY2022, while revenue slipped 2.06% from RM862.72 million recorded for the immediate preceding quarter.

On prospects, the group said it remains steadfast in its commitment to meeting its obligations to the Ministry of Health (MOH).

“We continue to negotiate with MOH on our logistics and distribution concession agreement, which is expected to be concluded by the end of the interim period of June 30, 2023,” it said.

Meanwhile, the group shared that it is on track to become a leading halal vaccine manufacturing plant, as its biopharmaceutical facilities are set to produce commercial batches of halal vaccines and insulin by 2025.

Pharmaniaga said that the group registered an encouraging 15% year-on-year growth in the private market as a result of aggressive sales efforts and new products launched.

"At the same time, we are proactively working to enhance the manufacturing division's operational efficiency, expand its product portfolio, and increase its global presence.

At this juncture, Pharmaniaga said that the Indonesian market remains its key growth driver and it will further penetrate the market and improve its position as a reliable healthcare provider in the region.

On its Practice Note 17 (PN17) status, the group said that it will complete the implementation of the regularisation plan by 1QFY2024.

“We are undeterred and confident that the upcoming regularisation plan will improve our shareholders’ equity and liquidity through prudent debt management and strategic capital allocation,” it added.

Pharmaniaga shares gained half a sen at 38 sen on Thursday (May 18), for a market capitalisation of RM497.88 million.

- Malaysian stocks broadly lower, KLCI plunges to one-year low after Wall Street's sharp drop

- US stocks tumble, Nasdaq has its worst day since 2022

- Capital A, TDM, MGB, Lim Seong Hai Capital, JF Technology, Kerjaya Prospek, Pestech, Sapura Resources, Oasis Harvest, Annum

- Asian stocks slide as market sell-off deepens on US growth worries

- China’s aluminium firms set to enjoy sharp rebound in profits on stunning drop in raw material costs

- Japan's trade minister fails to win tariff exemption assurance from US

- Citi cuts US stocks, raises China on pause in US exceptionalism

- Japan downgrades 4Q GDP, US tariffs cloud outlook

- GuocoLand lodges RM500m medium-term notes programme with SC

- Fire-fighting operations at oil palm plantation and forest in Gebeng completed