KUALA LUMPUR (May 10): More Bursa Malaysia-listed companies have seen analysts revising downwards their earnings forecasts recently, data compiled by The Edge showed, hinting at more negative than positive earnings surprises so far this year.

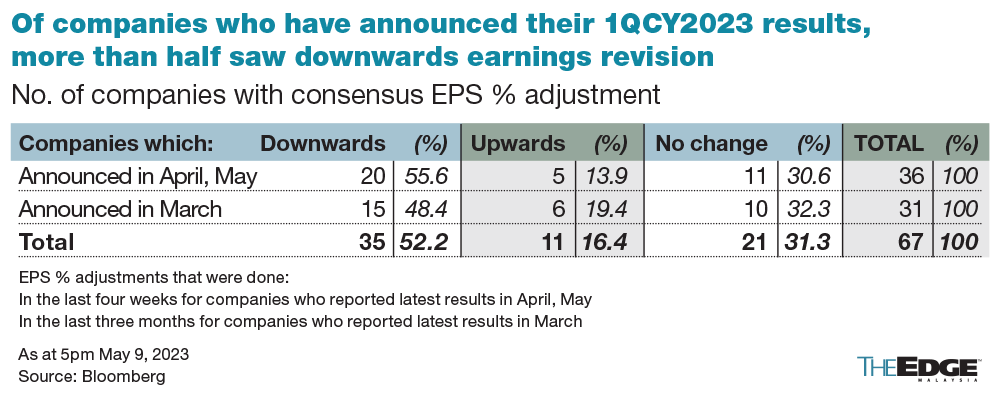

Of the 36 companies with analyst coverage that have released their latest quarterly results since April, 20 or 55.6% of these companies saw their consensus full-year earnings forecasts revised downwards, while just five companies or 13.9% saw their earnings forecasts adjusted higher.

As for those who have yet to announce their results for the first quarter corporate earnings season of the year (1QCY2023), 27 companies had their EPS forecasts adjusted lower in the last four weeks, against 20 companies with upward earnings adjustment in the same period, data compiled from Bloomberg showed.

In the last three months, 149 or 45.6% of companies who saw revisions to their earnings forecasts were downward adjustments, as opposed to 90 or 27.5% that saw upward revisions, according to the data, which screened 327 Bursa-listed companies with analyst coverage.

And despite rising interest rates and recovering consumer spending, those that saw downward revisions were banks — with revisions of between 0.16% and 3.31% — and companies involved in consumer products.

Other sectors with downward bias include plantation, property and construction, the data showed.

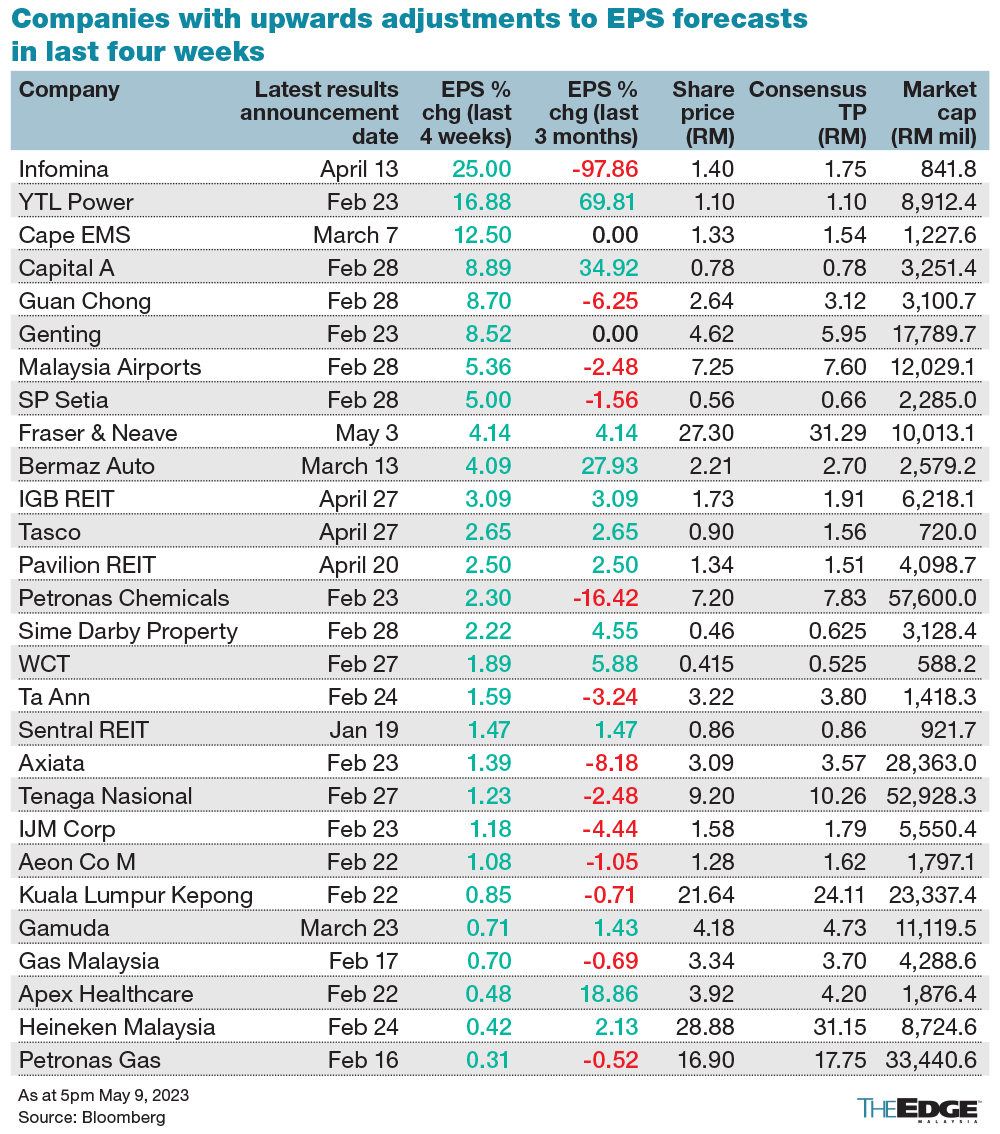

On the flip side, the companies with recent upward adjustments to their earnings forecast include utility companies like YTL Power International Bhd, whose earnings for this year has been raised by 16.9% on sustained demand, coupled with improving overseas performance; as well as sectors driven by tourist footfalls, including aviation group Capital A Bhd (8.9% higher from previous consensus forecasts), Malaysia Airports Holdings Bhd (5.4% higher) and Genting Bhd (8.5%).

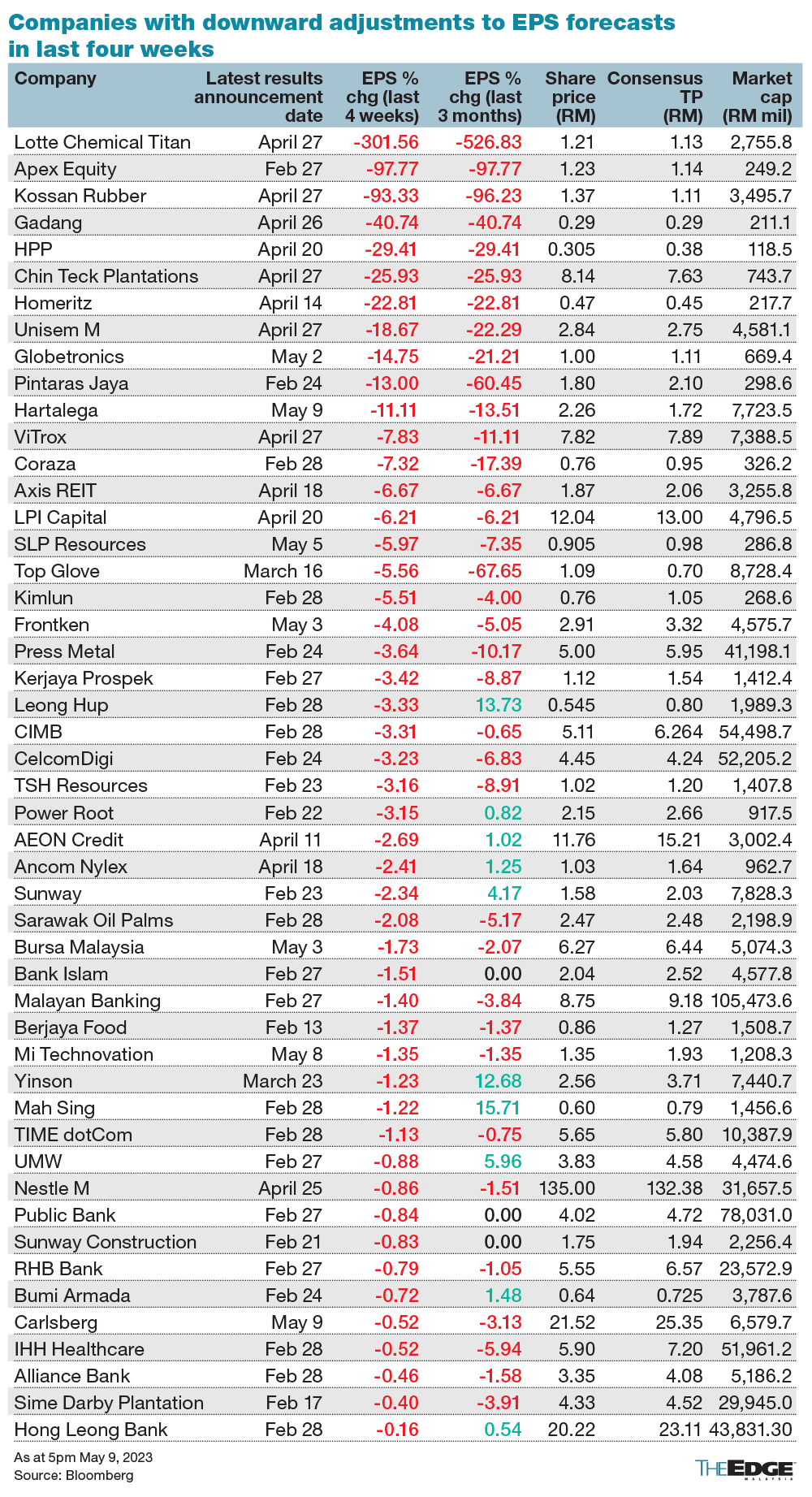

Companies who posted lower-than-expected earnings in the their first quarter earnings of 2023 include Bursa Malaysia Bhd, which recorded lower market trades; and petrochemicals group Lotte Chemical Titan Holding Bhd, which was affected by lower selling prices and plant utilisation.

Others who missed expectations have been facing sectoral headwinds, including technology counters Frontken Corp Bhd, ViTrox Corp Bhd and Unisem M Bhd on weaker global semiconductor market; and glovemaker Kossan Rubber Industries Bhd on oversupply.

Stronger headwinds?

When contacted, MIDF Research head of research Imran Yassin Md Yusof told The Edge that the research house expects “1QCY2023 to see better growth in terms of quarter-on-quarter (q-o-q) and year-on-year (y-o-y), based on the absence of Cukai Makmur and the fact that our economy has reopened for more than a year now”.

“The reopening of China’s economy may also provide some boost,” Imran said.

Malacca Securities Sdn Bhd’s head of research Louie Low Ley Yee concurred on the China factor, adding that the recovery play momentum seen the last year “should sustain in the quarter”.

“And we believe that the growth of Malaysia’s GDP would be around 4%-5% for 1Q2023; that should provide some potential impetus of momentum towards all the corporate earnings going into the May reporting season,” Low said.

A potential risk is the rising interest rate regime that could affect highly-geared companies, said Low, pointing to the overnight policy rate (OPR) increase to 2.75% in November 2022, and 3% last week, from 1.75% in March 2022.

Areca Capital Sdn Bhd CEO Danny Wong said the sentiment “is not so bullish in 1H2023 due to rising interest rates, potential US economic weakness and geo-political risks”.

“Another reason for forecast revisions are increases in costs linked to labour and utilities,” Wong said in a reply to The Edge.

“Import costs have also increased due to weakness in the Malaysian ringgit...2H may be better on the basis that interest rates and inflation rate have peaked, and demand may come back for those whose products may need to be restocked,” Wong added.

Following the rise in non-domestic electricity tariffs surcharge to 20 sen/kwh for certain segments from 3.7 sen/kwh in 1H2023, companies such as hard disk drive component manufacturer Dufu Technology Corp Bhd and flour miller FFM Bhd have warned that higher electricity costs would impact their earnings.

As for the ringgit, it has pared its strength to trade at 4.4370 against the US dollar at the time of writing, compared to 4.2435 at its strongest in February. The currency averaged 4.3965 against the greenback in 1Q2023.

While Malaysia’s headline inflation has moderated for the seventh month to 3.4% in March, stickier inflation may eat into earnings, as some industries have opted for price increases in 2021 and 2022.

Nestle M Bhd, in releasing its 1Q results, said it believes it is mostly done with price adjustments for now, following the last price hikes in March. TA Research, in a note dated April 28, attributed Nestle’s recent top-line growth to price adjustments, citing its parent company’s regional performance, where 9.1% of organic growth came from repricing, while only 1.3% came from real internal growth.

Inter-Pacific Securities head of research Victor Wan, meanwhile, noted that “revenge spending is tapering down”. Spending was previously supported by Employees Provident Fund (EPF) withdrawals and financial support, and government handouts, coupled with festive spending in 1Q and 2Q2023, Wan said.

China’s impact has also not really come-in in a big way, Wan said, pointing to reports of how many still prefer to spend on the mainland, while direct flights to the world’s second largest economy have not rebounded to pre-Covid levels.

“On a q-o-q basis, the fourth quarter results were not so pronounced and I expect that trend to continue in 1Q2023… generally, the economy is at a slower pace,” said Wan.

“The ringgit is one reflection of the strength of the economy,” he added. “If domestic demand weakens in 2H at the same time with sustained weaker exports, then we are in for a tough time.”