This article first appeared in The Edge Malaysia Weekly on April 24, 2023 - April 30, 2023

ACE Market-listed data storage and cloud specialist Kronologi Asia Bhd, whose operations in China count Baidu Inc as a client, reveals that it is in talks with Amazon Web Services (AWS), Alibaba Cloud, Tencent, Ping An Cloud and Microsoft Azure to offer them its enterprise data management (EDM) services.

Baidu is one of the largest artificial intelligence and internet companies in the world.

Kronologi is a hybrid and cloud EDM technology and solutions provider with a diversified customer base, comprising government sectors, large enterprises, food and beverage companies, banks, financial institutions, stock exchanges, as well as media and broadcasting companies. It provides EDM solutions to Baidu.

“In terms of where we are on the value chain, both AWS and Kronologi are cloud service providers. But if you look at how we are serving Baidu’s hyperscale infrastructure in China, there is a possibility that AWS could also be our client in Malaysia,” says Kronologi CEO and executive director Edmond Tay Nam Hiong.

“But then again, it’s not just AWS. We would like to think that all hyperscalers (large cloud service providers) could potentially be our clients. We could provide EDM solutions to them and we could be a hybrid cloud enabler.”

He says AWS’ decision in March this year to invest RM25.5 billion in Malaysia by 2037 has validated Kronologi’s proposition on the growing importance of data and rising demand for cloud storage.

This is AWS’ first cloud computing infrastructure investment in Malaysia.

“Overall, we are happy to see more hyperscalers coming to Malaysia. It’s good for the whole market. It shows that the cloud market is buoyant. Everybody will be enjoying a bigger slice of an enlarged pie,” Tay continues.

Unlike hyperscalers, Kronologi does not own data centres, which are capital intensive. Instead, the group leases space from data centre providers.

But for Tay, it is Kronologi’s business in China that gets him excited.

Higher contribution from China

In November 2018, Kronologi invested in a 16.67% stake in China-based digital infrastructure outfit Quantum China Ltd (QCL) for US$3 million.

About two years ago, Kronologi acquired the remaining 83.33% stake in QCL for RM150 million via a 50:50 cash-plus-share deal, in a move to expand its sales, marketing and customer coverage footprint in China.

Tay says that it has been a successful acquisition by Kronologi, as QCL has met its profit guarantee targets and fulfilled the terms of the deal.

“China is a market that we have to be in. The growth in Asia surrounds China. If we want to grow bigger and faster, we have to participate in the country. Today, we are not a big player there, but even then, China is already contributing to about 28% of our group’s revenue.

“We see huge growth potential in China. The way I see it, we are merely scratching the surface of the Chinese enterprise data market. By virtue of its size and business momentum, I think China has the potential to overtake Singapore as the top contributor to our group in the near term,” he elaborates.

The bulk of Kronologi’s turnover in FY2023 came from Singapore, amounting to RM106.82 million (34% of total revenue), followed by China and the Philippines, which contributed 28% and 24% of the group’s top line respectively.

“Moving forward, we expect more Chinese hyperscalers and multinational corporations to use our total solutions to serve their ever-growing data management requirements.

“Definitely, we hope to secure more clients in China. Besides hyperscalers, we are also targeting webscalers in various countries. For example, some telcos want to participate in the cloud market. They are not as big as hyperscalers, but they are our potential customers,” says Tay.

By product category, the EDM infrastructure technology segment continued to dominate Kronologi’s turnover, amounting to RM248.44 million or 79% of its total revenue, with EDM as-a-service making up the balance.

Tay observes that Kronologi’s performance in various markets has been “pretty good”, and the group intends to strengthen its financial performance in the coming years.

“Our core strength is our ability to provide ‘as-a-service’, ‘pay-per-use’, consumption-based and subscription-based services in the area of data management,” he says.

Despite various global challenges, such as a weakening IT spending environment, Kronologi aims to double its turnover and triple its earnings before interest, taxes, depreciation and amortisation (Ebitda) within the next three to five years.

In March this year, IT consulting and research firm Gartner Inc said that global IT spending contracted by 0.2% to US$4.38 trillion in 2022. Earlier, in January, it had forecast a 2.4% growth for worldwide IT spending this year — less than half its previous estimate last October — as economic uncertainties continue to rattle markets.

Tay acknowledges that the macro environment is expected to remain challenging this year, but he is confident that the group will continue to register growth in the coming years.

“Conservatively, we work towards a 10%-15% growth for both top line and bottom line every year. But our long-term goal is to double our group’s revenue and triple our Ebitda in the next three to five years,” he says.

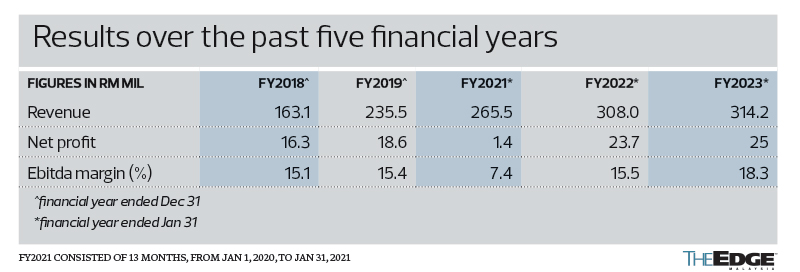

For the financial year ended Jan 31, 2023 (FY2023), Kronologi saw its net profit grow 5.7% to RM25 million, from RM23.65 million a year ago. The technology firm’s revenue increased 2% to RM314.24 million in FY2023, from RM308.01 million the year before.

The group’s Ebitda grew 21% to RM57.6 million in FY2023, from RM47.6 million the previous year.

As at end-January, its debt ratio stood at less than 0.3 times, while its cash and cash equivalents amounted to over RM100 million.

Tay highlights that Kronologi had been well positioned to benefit from the continued recovery of demand for data management solutions in the second half of 2022.

“Our group is well poised and confident in taking advantage of the secular growth trend in data-driven digitalisation and hybrid cloud. We believe data remains key and mission critical for enterprises,” he says.

Is Kronologi undervalued?

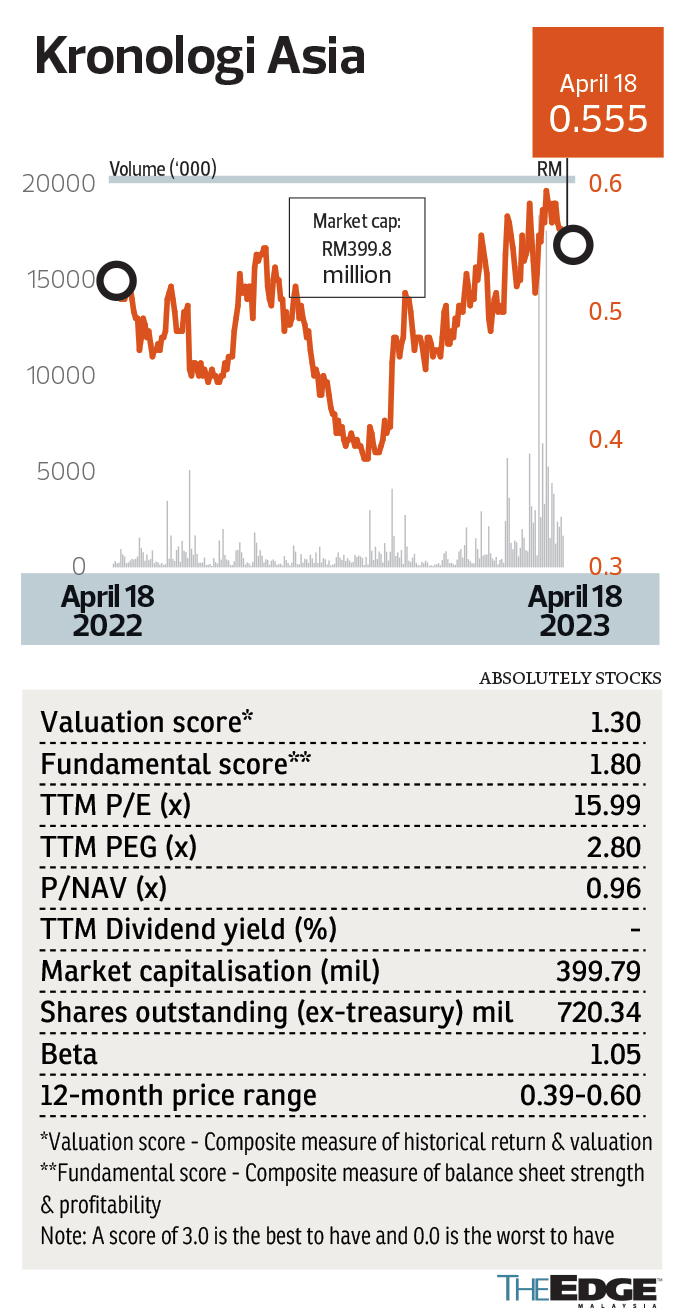

Year to date, Kronologi’s share price has risen 16% to close at 55.5 sen last Tuesday, giving the company a market capitalisation of RM399.8 million. The counter is currently trading at a historical price-earnings ratio (PER) of 16 times.

Kronologi executive director and chief operating officer Tan Jeck Min believes that the group’s pan-Asia business footprint offers exposure to the growing data markets across the region, including China.

“In the business segment that we are in, we feel that our stock valuation should be seen in the same light as other digital service providers such as ITMAX System Bhd and LGMS Bhd, which are trading at much higher stock valuations,” he says.

ITMAX is trading at a historical PER of 36 times, whereas LGMS’ is at 42 times.

Although Kronologi meets the requirements to transfer its listing to the Main Market, Jeck Min says the board is still deliberating on the benefits of making the transfer. “Other than a higher mandate for institutional investors, we are reviewing if there are any other clear advantages of going to the Main Market.”

According to its Annual Report 2022, as at May 5 last year, Kronologi had three substantial shareholders, namely Desert Streams Investments Ltd (14.7%), Lavender Blooms Investments Ltd (12.57%) and Jeck Min (7.67%).

In a March 30 research report, Apex Securities Bhd analyst Jayden Tan Kean Dick maintains a “buy” call on Kronologi, with a higher target price of 67 sen, up from 56 sen previously.

“We favour Kronologi for its sustainable income, promising industry outlook driven by the digitalised data era, as well as its robust balance sheet [which] minimises risk amid the economic downturn,” he writes.

Jayden also points out that as Kronologi exclusively serves the Asian market, the group is anticipated to capitalise on the region’s economic growth.

“We understand that Kronologi is engaging with some corporate giants in China. Hence, we are optimistic on the group’s China operations, [which are expected] to grow further moving forward, supported by the reopening of China’s economy,” he adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.