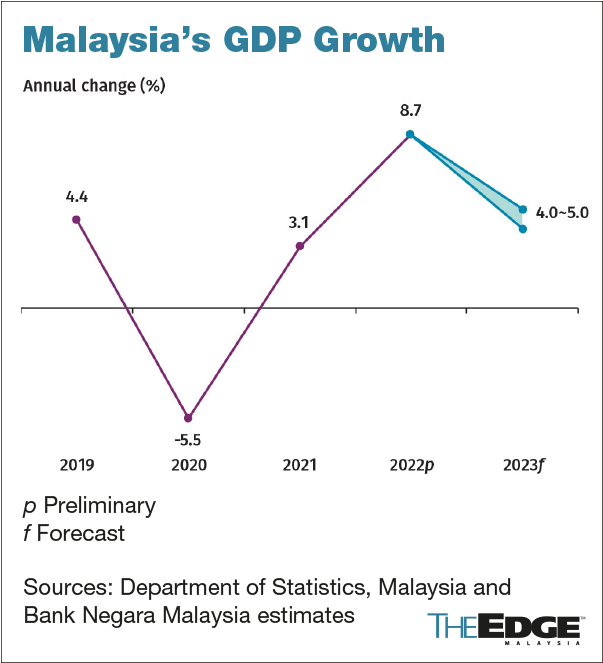

KUALA LUMPUR (March 29): Malaysia’s economic or gross domestic product (GDP) growth is projected to ease to between 4% to 5% this year, as slowing global growth is anticipated to weigh on exports while concern about elevated costs of living and input costs are expected to impact spending by households and businesses.

Bank Negara Malaysia (BNM)’s GDP growth projection is within the government’s official forecast of 4.5% growth in the country’s GDP for the year. In 2022, Malaysia’s economy achieved the highest growth rate over two decades, expanding by 8.7%.

“The risks to Malaysia’s growth projection are fairly balanced. Downside risks emanate primarily from external factors, mainly from weaker-than-expected global growth stemming from a sharp tightening in global financial markets amid tighter monetary policy or worsening sentiments,” according to the central bank’s Economic and Monetary Review 2022 report.

Further escalation of geopolitical conflicts could also dampen Malaysia’s trade performance, said BNM.

On the domestic front, the central bank said higher-than-expected inflation would lower the purchasing power of households, while a steep rise in input costs could affect firms’ profits.

Nevertheless, better-than-expected labour market conditions, stronger pick-up in tourism activities, as well as the implementation of projects — including from the recently re-tabled Budget 2023 — may lift domestic growth outlook, BNM added.

Domestic demand remains the anchor of growth

Domestic demand, particularly private sector spending, will remain the anchor of growth for the Malaysian economy in 2023, according to the central bank.

Private consumption is projected to continue growing, albeit at a more moderate pace at 6.1% in 2023, from 11.3% in 2022. While households are expected to further adjust spending in response to elevated cost of living, consumption spending will be underpinned by continued improvements in labour market conditions.

Unemployment rate is expected to improve to 3.5%, with a more broad-based expansion in income.

In addition, government policy measures, including the implementation of a higher minimum wage by small firms, the expansion in the coverage of employees entitled for overtime pay, the revision in individual income tax rates in Budget 2023, as well as cash transfers, are expected to provide further support to household income.

Meanwhile, the growth of private investment, which is projected to slow down to 5.8% this year from 7.2% last year, will be supported by the realisation of new and ongoing investment projects across key economic sectors.

“Further progress in key infrastructure projects such as the Malaysia Digital Economy Blueprint (MyDIGITAL) and continued drive for greater automation and digitalisation would also support investment activity.

“Furthermore, ongoing efforts by the government, particularly through the various initiatives under the new investment policy to attract and facilitate the implementation of investment projects, would provide additional support to investment activity,” read the report.

Public investment to expand by 7%, public consumption growth to slow

Public investment is expected to expand by 7% in 2023, compared with 5.3% in 2022, attributable to higher capital spending by both the general government and public corporations amid the continued progress of large-scale infrastructure projects, such as the East Coast Rail Link (ECRL), the Light Rail Transit Line 3 (LRT3), and the Pan Borneo Highway.

Investments by several major public corporations to support the transition to net zero carbon emission by 2050 is expected to provide additional lift to growth for public investment.

Public consumption, on the other hand, is expected to grow at a slower pace of 1.3% this year, compared with 3.9% last year. This moderation is due mainly to contraction in supplies and services spending due to the lapse in Covid-related expenditure.

Emoluments spending, however, is expected to be higher, driven by Special Additional Annual Salary Increment of RM100 for civil servants and the absorption of contract officers to permanent positions — particularly in the health and education services.

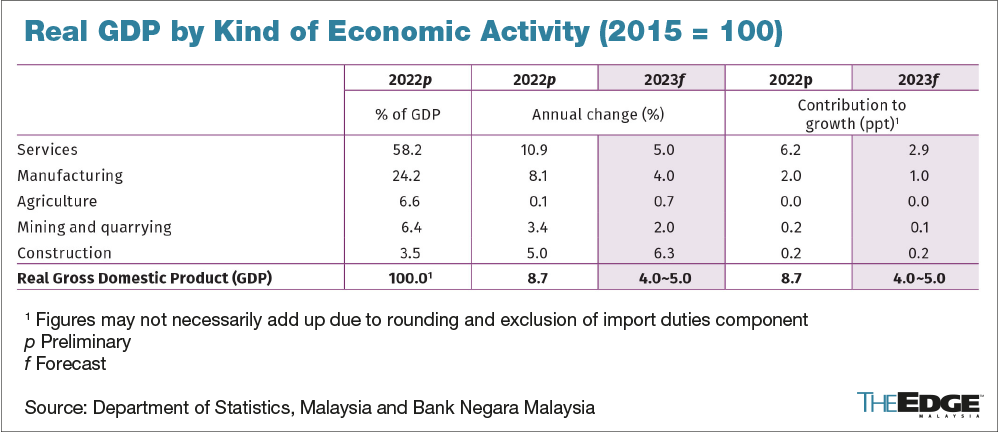

Most economic sectors to expand more moderately

According to BNM, most economic sectors are projected to expand at a more moderate pace amid the expectation of slower global growth and the normalisation of high growth recorded last year.

“Broadly, growth will be driven by continued expansion in consumer and tourism-related subsectors, while export-oriented subsectors are expected to moderate, in line with slower global growth,” it noted.

Nonetheless, the easing of supply chain disruption and the resolution of labour shortages will lend support to all economic activities.

Growth in the services sector is expected to ease to 5% from 10.9% in 2022; that growth will be underpinned by consumer- and tourism-related activities amid further recovery in global tourism activity.

Business-related services will remain supportive of growth, although at a slower pace, in line with the continued expansion in construction activity and external demand. Sustained demand for data services, mainly in support of e-commerce and e-payment activities, is expected to provide further impetus to the information and communication subsectors.

Growth in the manufacturing sector is expected to be moderate to 4% this year from 8.1% last year, with the electrical and electronics (E&E) cluster projected to grow below its long-term average of 6.2%, in tandem with the anticipated slowdown of global semiconductor sales.

Growth in the consumer-related manufacturing cluster would also be lower, amid the normalisation in household spending activities.

The construction-related manufacturing cluster, in contrast, is forecast to record modest growth, supported by investment in structures. This primary-related cluster is projected to expand at a faster pace, partly supported by higher capacity utilisation at a major oil refinery in Johor.

Mining sector growth is projected to moderate to 2% this year, from 3.4% last year. While the operationalisation of new facilities in Peninsular Malaysia and higher production in existing oil and gas facilities — including Block SK320 in offshore East Malaysia — will provide support to growth, this will offset the loss of output from maintenance-related closures in several facilities and maturing oil and gas fields.

As for the construction sector, it is expected to record stronger growth in 2023, buoyed mainly by continued improvement in activities within the civil engineering and residential subsectors. Faster progress of existing large transportation and utility projects will lift growth in the civil engineering subsector.

Higher new housing launches, in tandem with the expected expansion in demand following better income and employment prospects, will provide support to the residential subsector.

Similarly, the agriculture sector is projected to improve, growing at 0.7% this year as opposed to 0.1% last year, and will be supported mainly by higher oil palm production, as labour supply improves.

Heavier rainfall in the early part of the year is also expected to improve soil moisture, thereby increasing oil palm yields in the later part of the year.

Additionally, the gradual recovery in raw material supplies, especially fertiliser and animal feed, is anticipated to support growth in livestock and other agriculture subsectors.

Don't miss the other highlights of the BNM Annual Report 2022. Read the articles here.