This article first appeared in The Edge Malaysia Weekly on March 13, 2023 - March 19, 2023

THE retail sector, which has seen a robust rebound since the reopening of the economy last April, is expected to remain strong this year despite inflationary pressures and higher interest rates, say analysts.

Indicators such as healthy footfall in shopping malls and the Malaysian Institute of Economic Research’s Consumer Sentiment Index for the fourth quarter last year rising to 105.3 from 98.4 in the previous quarter have been telling of better job and income prospects, as well as the softening of inflationary pressures.

“[These have been] pointing towards sustained consumer spending, supported by the reopening of the economy and the return of shoppers, commuters, the office crowd and international tourists. Second, financial assistance to the low-income group and subsidies for fuels, electricity and selected food items have [helped to] keep the cost of living in check. Third, the job market is relatively stable and the M40 group has healthy household balance sheets,” Kenanga Research analyst Tan Jia Hui tells The Edge.

Similarly, analysts at MIDF Research expect inflation to trend downwards this year, which will bring about a corresponding pause in interest rate hikes. In addition, the festive season of Hari Raya next month, coupled with the various assistance packages provided by the government as well as the lower rate of unemployment, is expected to continue to drive momentum in the retail sector and boost the earnings of consumer companies, in particular those selling consumer staples, says the research house.

As for the implementation of the 20 sen per kWh electricity surcharge for medium and high voltage users for the period from January to June, a fivefold increase from 3.7 sen per kWh last year, retailers and hoteliers are awaiting a response from the government after pleading for a moratorium until December so that their businesses can recover from the impact of the pandemic.

In a joint statement on Feb 8, seven associations representing retailers and the owners and operators of hotels, theme parks and shopping malls — including the Malaysia Retailers Association, the Malaysia Shopping Malls Association, Malaysian Association of Hotels and Malaysian Association of Hotel Owners — lamented to the government that their monthly energy bills had gone up by at least 20% to 30% from the previous year, despite similar usage levels.

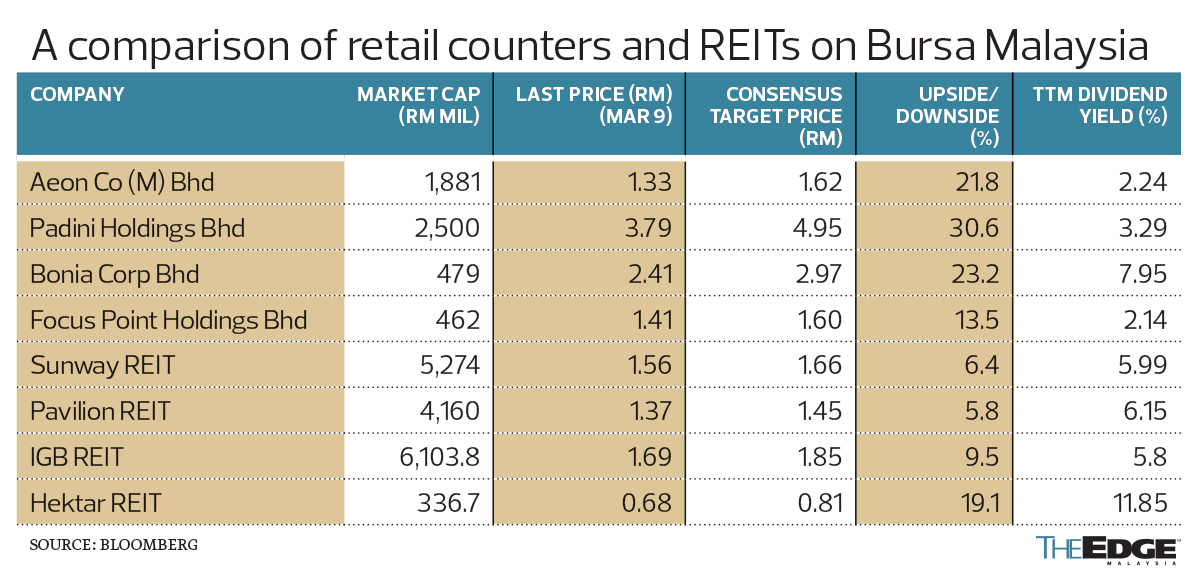

The higher electricity tariff is expected to increase the operating costs of retail real estate investment trusts (REITs) as electricity cost typically makes up about 30% of property operating expenses, MIDF Research notes.

It explains that there are limited measures to blunt the impact of higher electricity costs apart from replacing lighting with energy-saving bulbs. An analyst who declines to be named notes that Aeon Co (M) Bhd and Padini Holdings Bhd, which are major tenants in shopping centres, have installed solar panels in their buildings and warehouses respectively to blunt the impact of the higher electricity costs.

“Overall, the electricity cost will remain higher as more activities [are taking place] at malls now, such as events that consume more electricity. However, the higher rental income is expected to cushion the higher operating cost. Margins were squeezed last year, but most companies have been able to pass on the additional costs to consumers,” says MIDF Research.

RHB Research associate Ammar Affan adds that the impact of the new electricity tariff on REITs is manageable.

“While electricity makes up about 90% of REITs’ utility costs (making up about 20% of the total property operating expense), some of the trusts’ management teams have guided for a minimal impact on distribution per unit of about 3%. Furthermore, REITs could opt to pass on the increase in electricity cost to tenants to further mitigate the rate hike,” he says.

Festivities, tourist arrivals to sustain sales

For the second quarter ended Dec 31, 2022 (2QFY2023), Padini’s net profit rose 20.1% to RM73.14 million from RM60.89 million the previous year. The apparel retailer attributed the higher earnings to the sustained recovery from the pandemic, which also resulted in a 19.3% increase in quarterly revenue to RM509.48 million from RM427.17 million. Padini has declared a third interim dividend per share (DPS) of 2.5 sen, to be paid on March 31.

Kenanga Research’s Tan, who has an “outperform” call on the counter with a target price of RM6, acknowledges that it is a lofty target price for the stock, which is currently trading at the RM3.79 level, as she believes the brand will benefit on several fronts, such as wardrobe replenishments, affordability for impulse buys and strong spending power of its primary group of buyers, the M40. She says the group’s strong net cash position enables it to purchase inventory ahead of price hikes and potential supply disruptions, and that the impact of escalated raw material costs came off for Padini as supply chain disruptions in China eased.

“The higher tourist arrivals, especially from China, are anticipated to prosper retail trade in Malaysia, and the better retail sales outlook will help retailers of general products like AEON Co. Moreover, the potential cash aid and incentives to low-income groups in the forthcoming Budget 2023 could raise disposable incomes and boost consumer spending on essential items,” says MIDF Research, which has a “buy” call on AEON Co with a target price of RM1.81 as it believes the general merchandise store (GMS) will continue to see steady sales ahead in the trading of daily essential goods.

AEON Co’s net profit for 4QFY2022 sank 64.9% to RM24.92 million from RM70.98 million in the year before on account of an increase in promotional activities, maintenance costs and lower reversal of impairment for receivables. It declared a final DPS of four sen for FY2022, which is higher than the three sen paid in FY2021.

Despite AEON Co’s lower net profit, analysts believe the GSM operator will chart steady sales ahead in its daily trading of essential goods.

Kenanga’s Tan, who has an “outperform” call on AEON Co with a target price of RM1.80, notes that the group has completed its digital transformation and has begun introducing self-checkout terminals at its 42 stores. She believes this will result in cost savings and partial mitigation of labour shortage issues.

Bonia Corp Bhd posted a net profit of RM20.3 million for 2QFY2023, a slight improvement from RM19.4 million the year before. Revenue came in at RM112 million, up 9.6% from RM102.2 million earlier.

The retailer, which carries brands such as its namesake, Renoma and Valentino Rudy, declared an interim DPS of two sen for 2QFY2023, bringing the cumulative FY2023 dividend to four sen per share.

Bonia attributed the higher revenue to its brand building strategy, opening of new stores and retail facelift of its existing stores and effective digital marketing programme. The company also declared an interim DPS of two sen for 2QFY2023, bringing the cumulative FY2023 dividend to four sen per share.

CGS-CIMB analysts Walter Aw and Khoo Zhen Ye say in a Feb 21 note that they expect “solid 2HFY23F results despite high inflationary pressures, driven by Bonia’s strong brand equity, novel product launches, effective marketing campaigns and growing loyal customer base”. Aw and Khoo believe the group’s 2HFY2023F sales could be driven by festive sales, namely Chinese New Year and Hari Raya, as well as the company’s ongoing store expansion, in which there are plans this year to open two to three new boutique outlets with attractive designs, making up about 4% of its total boutiques.

Aw and Khoo point out that Bonia’s 1HFY2023 core net profit of RM31.5 million “beat expectations and accounted for 70% of our estimates and 78% of Bloomberg consensus’ FY2023F estimates”. The research house has an “add” call on Bonia with an unchanged target price of RM3.50.

The net profit of eyewear retailer Focus Point Holdings Bhd, which has a food and beverage (F&B) arm as well as franchise businesses, including Lasik centres, rose 12.5% to RM10.45 million for 4QFY2022, from RM9.29 million the year before. Revenue was RM68.4 million, rising 7.4% from RM63.7 million earlier.

“We believe it will be an exciting year ahead for Focus Point’s F&B division as more corporate customers have been secured for the supply of products from its central kitchens. Note, however, it may be challenging to further grow its optical business from the elevated FY2022 earnings base that was partially boosted by pent-up demand, particularly tourists from Singapore and the various spending boosters,” says a second analyst who declines to be named.

Bloomberg data show that the only analysts covering the stock, TA Securities Holdings’ Kevin Tan Kong Jin and Hong Leong Investment Bank’s Syifaa Mahsuri Imail, have “buy” calls on Focus Point, with target prices of RM1.59 and RM1.61 respectively.

Meanwhile, MIDF Research is also positive on the outlook for owner/operators of retail malls Pavilion REIT, IGB REIT and Sunway REIT, thanks to “high occupancy rates of malls in their portfolio, namely Pavilion Kuala Lumpur, Mid Valley Megamall and Sunway Pyramid respectively”.

“Shopper footfall has recovered to pre-pandemic levels and tenant sales have improved. Hence, rental reversion of the malls is expected to be positive going forward and support earnings growth,” says the research house, which has “buy” calls for all three REITs with target prices of RM1.63, RM1.86 and RM1.73, in the order above.

Meanwhile, AmInvestment Bank research analyst Zing Sheng Khoo has a “buy” call with a target price of 81 sen for Hektar REIT, which has an average portfolio occupancy rate of 82% for the six neighbourhood malls it operates.

While the year-end to Chinese New Year stretch, as well as Hari Raya, are typically high-growth periods in the retail calendar, it remains to be seen whether the sales momentum will actually extend into the coming quarters, bearing in mind that the industry is still coming off last year’s low base.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.