This article first appeared in The Edge Malaysia Weekly on March 6, 2023 - March 12, 2023

MALAYSIA has fallen behind and needs to catch up. Without the foundational infrastructure like internet connectivity and 5G, we would not be able to attract technology investments, be they foreign, such as Microsoft, AWS and Google, or local new start-ups. This will deprive the nation of the tremendous growth opportunities that lie ahead and the high-paying jobs we need to create. According to Qualcomm, the full 5G value chain of eMBB (enhanced Mobile Broadband), uRLLC (ultra-Reliable Low Latency Communications) and mMTC (massive Machine Type Communications) in a digital economy will generate revenues of up to US$13.2 trillion by 2035 and provide as many as 22 million jobs globally.

According to an EY economic impact study, the faster availability of 5G and at lower cost per GB as contemplated by the SWN model would add RM650 billion to Malaysia’s GDP from 2022 to 2030 and create 750,000 new high-income jobs (see Diagram 2).

But why couldn’t we leave this to the existing MNOs to invest and roll out instead of DNB?

There is no question that this would have been the preferred avenue. These MNOs already own their customers and the 4G infrastructure and spectrums. They are private entities, driven for profits and know business best. Why reinvent the wheel, and commit government resources into what is deemed a private economic sphere? It is a good logical conclusion. Except …

a. These MNOs were not willing to come together to put up a shared 5G infrastructure, as was the case in 2018/2019.

b. To each put up their own 5G infrastructure requires huge investments. The equivalent cost of coverage for 5G over 4G is at least three times more. And unless there is demand, how would these MNOs justify their investments? 5G is an enterprise application with no known killer apps for retail use (at least till today).

c. The question then was, should the nation roll out 5G based on demand-led, build only when sufficient customers want it? Unlike 3G and 4G, where the use is mostly for retail, to make calls and text messages, to do Google searches or download short videos, 5G has no immediate retail applications that are critical, except for gaming, to an extent. It does not justify the cost of investments for a profit-driven private enterprise. The existing MNOs had indicated that they did not plan to roll out 5G at least until 2024. From the perspective of a private enterprise, this is totally understandable and responsible. But does this serve the national interest? Private and national interests do not always align, which is why we need regulations.

d. As private enterprises, the telcos must also maximise the returns to their shareholders. Many of them are listed on Bursa Malaysia. The way to maximise profits is to sweat out the assets where they have already put a lot of investments into, the 4G infrastructure.

e. The challenge to public policy is: What are the risks of delays in rolling out 5G? Not only is Singapore ahead of us, but so are the Philippines, Thailand, Vietnam and Indonesia, among our neighbours (see Diagram 1). Forget the advanced economies and China, Taiwan, South Korea and so forth. We know technology is a “winner takes all” global marketplace (unless your market size is that of China or the US, you are part of the global supply chain). While initial investments are huge, owning the intellectual properties and the customers creates the moat through very low to literally zero marginal costs once scale is achieved. It is why we see many market segments dominated by a few global players, whether in cloud, in search, in ride sharing, in deliveries and so on. Labour costs progressively become less important, which is why workers are better paid. And once these huge companies locate elsewhere, would they also invest in Malaysia? And, more critically, for start-ups, if Malaysia does not provide the infrastructure for them to do their innovations and R&D, and these ideas and talents migrate and germinate in neighbouring countries, would they still benefit Malaysia and create the jobs here?

SWN, owned by the government, will lower the costs by 50% to the rakyat and with better service quality

f. In other words, is 5G to be supply-led as a catalyst and facilitator for the digital transformation of the nation? Build and they come? Much like roads (remember the North-South Expressway?), electricity (Bakun Dam) and ports (West Port). All these catalysts required the government to step in, and there were many sceptics, too. Has the internet moved from a “nice to have” to become a “necessity of life and livelihood”? If it has, is it not the role of the government to ensure adequate provision for all, at lowest possible costs, in order to enable better lives, businesses to find opportunities, to propel the nation’s development forward, much like providing policing for safety, electricity and water, and road connectivity?

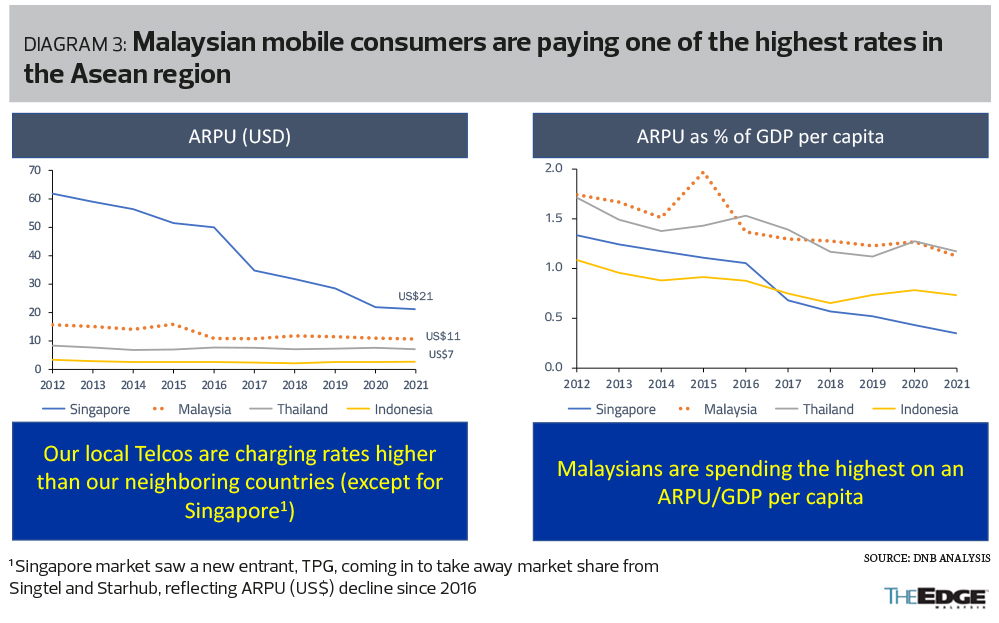

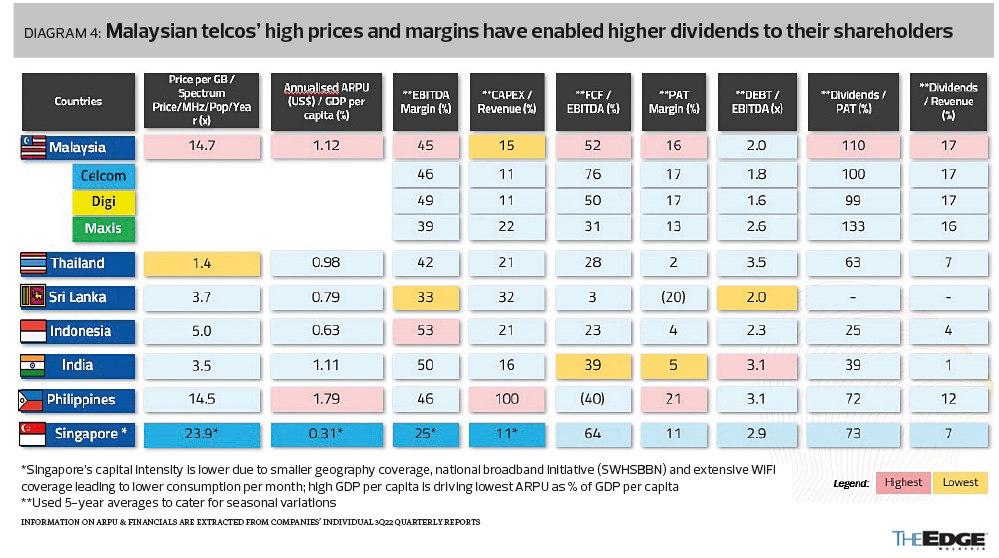

g. What about costs to consumers and quality of services? Diagrams 3 to 5) show that the prevailing price per GB in Malaysia is high in comparison to our neighbours, with no better-quality service. Shareholders have reaped these benefits with high dividends paid to themselves instead of reinvesting into the company to upgrade and provide better-quality services.

h. It is therefore no surprise that a tycoon confronted me and said that it is silly to have only one 5G provider under the SWN model in the country. A second operator licence (yes, just the licence) would easily be worth over RM1 billion, to whomever it is given. For clarity, he was not talking about the spectrum fee to MCMC.

i. It is a fact that the existing telco marketplace is an oligopoly. You cannot reap such excess economic returns otherwise. I do not imply any collusion or that their profits are undeserving. In fact, many of our telcos are highly efficient and well managed. And they have made great contributions to the nation, whether it is jobs, or taxes or values to the Employees’ Provident Fund (EPF), Khazanah Nasional and so on. What I want to explain is why it is an oligopoly, and new competitors cannot enter the fray. In other words, we have allowed and built the existing telcos to be the “gatekeepers” of our digital ecosystem (we are not the only ones — scan the QR code and watch this YouTube video on Canada: “Why are Canadian phone plans so expensive?”)

Since the spectrums and the 4G infrastructure are owned by the existing telcos, it is practically impossible for new entrants. MVNOs (mobile virtual network operators) must buy their connectivity to sell.

Imagine that our public roads are private, owned by four companies. Each built their own networks of roads. And they also sell their own cars. And to use the road, from points A to B, from your office to your house, Telco A owns that road and that road is accessible only to Car type A that Telco A markets. So, they can extract high prices and there is little you can do. And even if two or more of them own separate roads on the same route, they will compete by advertisements, frills and gimmicks to maximise their profits, because they know new competition is not possible.

Why are new entrants not possible? Because the infrastructure to enable road usage is already controlled by these oligopolists. A new entrant cannot offer the same connectivity, certainly not quickly. And although the regulator can insist that new entrants must be given the right to access these roads, the existing oligopolists will charge a high fee on these new competitors to ensure they cannot offer a price that is lower.

j.By shifting the 5G to an SWN shared by all the telcos, telcos and new players will have to shift their focus and investments into the other enablers of the digital ecosystem (see Diagram 6). It is important to remember that the provision of the 5G infrastructure is just that, the foundational infrastructure. Ultimately, the value proposition is in the provision of 5G solutions. This requires cloud and data centres, fiberisation and edge computing platforms, in addition to a host of digital software and solutions. In other words, the telcos must broaden their expertise and services beyond provision of infrastructure to value-added services.

k.Finally, besides the initial capitalisation of RM500 million provided by the Ministry of Finance to DNB, there is no further government funding. Banks will be funding the entire 5G rollout nationwide. This proves that the SWN model is financially sustainable (see Diagram 7).

What are the promises of using an SWN model to deliver 5G?

Besides the reasons above for an SWN model, what are the other benefits of SWN, instead of allocating the spectrums to the telcos as was done in the past, or even a Dual Wholesale Network (DWN) model?

1.As an SWN operator, with one single 5G infrastructure serving the nation, costs will be lower. Building a single four-lane highway will be cheaper than building four parallel one-lane highways. The current cost to generate 4G by the MNOs is 45 sen to 55 sen per GB. DNB will generate 5G at 11 sen to 13 sen per GB. Consequently, consumers will enjoy lower prices, estimated to fall from the average RM2 per GB for 4G now to RM1 per GB for 5G (see Diagrams 8 and 9).

2.Quality of service will also be enhanced, not just in relation to the existing 4G services in Malaysia but also in comparison to 5G download and upload speeds globally. With 5G now available in some parts of the country, this is now verified by OpenSignal. Indeed, the actual download speeds of 376 Mbps is faster than what was promised by DNB at 100 Mbps (see Diagram 10). A single eight-lane highway will always be more efficient than four double-lane highways running parallel to each other (see Diagram 11). 5G is a spectral efficient technology that creates a massive increase in capacity. The SWN approach enables large blocks of spectrum to be provisioned for use by all MNOs, instead of silo usage per MNO if not shared. MOCN (multi-operator core network)-sharing technology used by DNB is a well-proven technology with dynamic sharing of spectrum that ensures maximum efficiency, which will lead to lower prices for Malaysians, at much higher and consistent speeds.

3.DNB is achieving one of the fastest 5G rollouts in the world. As acknowledged by the prime minister in his Budget 2023 speech, DNB has already connected 50% of the population and will connect with 80% of the population by the end of this year (see Diagram 12).

The last question relates to what the government can receive if the spectrum were to be tendered out by MCMC as in the past.

This is a red herring argument articulated by those who oppose the SWN model. The fact is, spectrum auction has NEVER been conducted in Malaysia. It has always been through a “beauty contest”, where the price is fixed but bidders compete on other qualitative criteria. Why? Because MCMC wants to keep prices low for consumers. The auction price must eventually be passed on to all Malaysians anyway. The total of all past fees paid by Maxis and Celcom for all the spectrums they own is only RM1.1 billion each. U Mobile and Digi’s are a lot less (see Diagram 13).

DNB, in contrast, is fully government-owned. By all Malaysians. And as I have shown in Diagram 7, DNB is financially sustainable at 8% IRR (internal rate of return). It will probably be worth RM15 billion to RM20 billion at the end of the 10-year licence period. Would this not be better than for MCMC to get RM1 billion now? And if it is the desire of the government to monetise some of its future earnings, get in a decent investment banker and I have no doubt that a RM5 billion bond issuance will be easily underwritten and earned by the government now.

I have no doubt that I have seriously offended many. But I must stay true to my convictions. I believe the SWN approach is right for Malaysia.

Read also:

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia hit with 24% US reciprocal tariff effective April 9

- CIDB issues apology, retracts statement on devastating gas pipeline inferno

- Apple production hubs, including Malaysia, hit by tariffs

- Malaysian stocks decline following Trump reciprocal tariff

- Global companies face a new reality of Trump tariff chaos

- Malaysian stocks decline following Trump reciprocal tariff

- Nike falls as Trump’s reciprocal tariff plan sinks retailers

- China services growth picks up with economy pressured by tariffs

- OCBC aims to fund S$17b over five years to support FDI into United Kingdom

- Australia says US tariffs 'not act of a friend' but rules out reciprocal move