This article first appeared in Forum, The Edge Malaysia Weekly on January 23, 2023 - January 29, 2023

Digitalisation and automation have increasingly become more than buzzwords. We have seen businesses and governments seek to modernise the way they operate to become efficient and effective under the “new normal”. Malaysia is no different, with many aspects of our lives now being able to function remotely and seamlessly.

However, one area in which we have not seen significant levels of digitisation and automation is tax reporting. It is still commonplace for Malaysian businesses to handle a lot of their tax reporting manually, with significant investment in human resources to undertake the various reporting exercises. Tax audits and interaction with tax authorities continue to be done through non-electronic means and, in the case of audits, through manual checking and inspection of documents.

However, recent announcements on the introduction of electronic invoicing by the government and the Inland Revenue Board (IRB) could significantly change how we interact with tax authorities in the future. These changes would bring greater efficiency and transparency, especially in the areas of tax reporting and audits.

What is electronic invoicing?

Electronic invoicing, or e-invoicing, is a process that automates the digital exchange of invoice information directly between a vendor and a customer’s accounting systems. The information would be transmitted between the parties through a third-party network, which in some cases is administered by the government or the tax authority. This is a more secure and efficient way for information to be shared and should not be confused with sending invoices as PDFs via email or other more commonly used methods.

What has been the global practice?

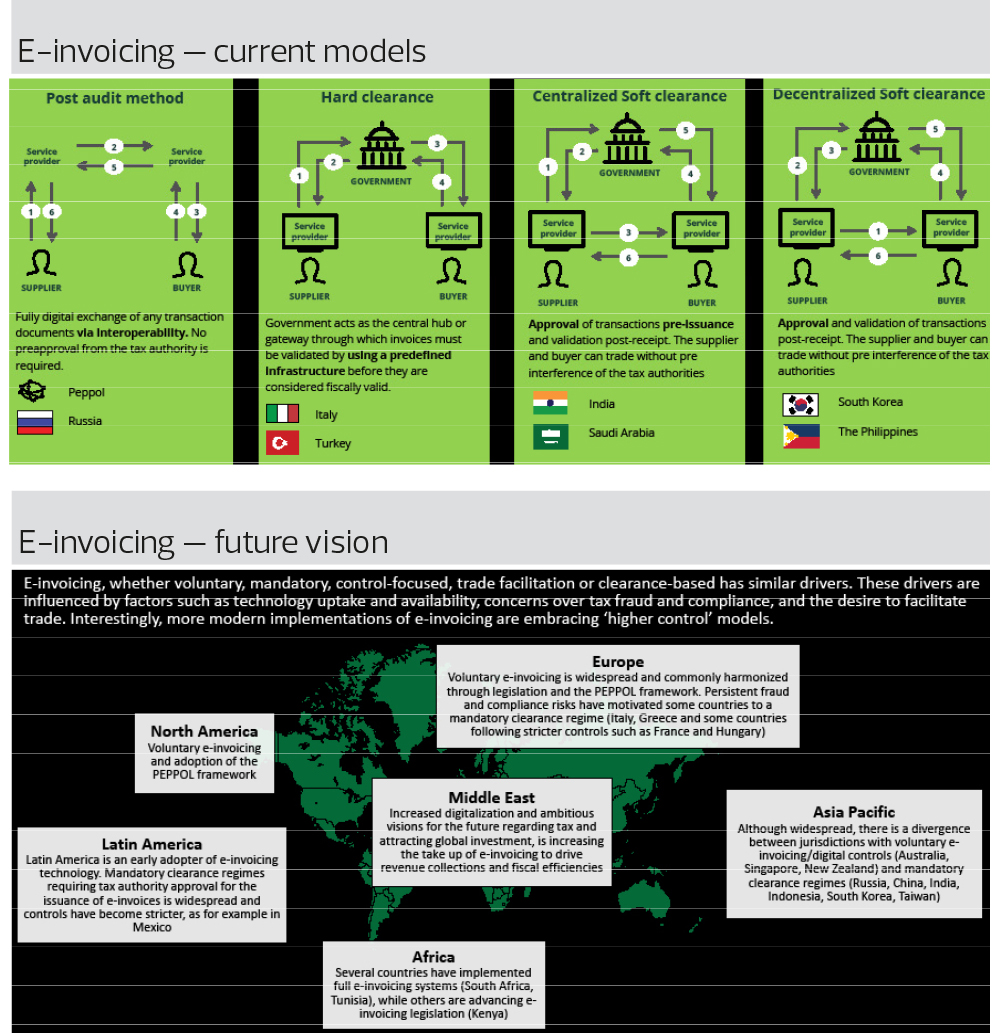

E-invoicing adoption is increasing globally in countries across Europe, Latin America and Asia. Closer to home, we have observed that countries such as China, India, South Korea, Australia, Singapore, the Philippines and Vietnam have all either implemented, or are in the process of implementing e-invoicing. The aim currently is for all business transactions to occur under some form of an e-invoicing model or framework before the end of this decade.

While governments are keen to implement e-invoicing, their motivations for doing so vary. This has translated into the different models adopted globally. The broader reasons for adoption fall on a mix of motivations, particularly around achieving efficiencies in tax, business, digital or trade processes. The drivers for tax have been on achieving greater tax transparency and reducing tax leakages from the shadow economy. These two key drivers resonate strongly with the Malaysian tax authorities, who have long highlighted the shadow economy as a significant concern. The benefits in terms of tax collection are supported by real data. For example, in Mexico, e-invoicing reduced the tax gap from indirect tax collections by over 50% and brought over 4.2 million micro-businesses into the formal economy. In Brazil, e-invoicing increased tax revenues by US$58 billion, thus reducing the tax gap. In considering these numbers, it is easy to see why many governments and tax authorities are clamouring to introduce these measures.

In terms of the models adopted, the most common form of e-invoicing in our region is the “clearance model”, followed closely by the “post audit” model. The clearance model has been adopted or is in the process of being adopted in India, China, South Korea, Vietnam, Thailand and the Philippines. It requires the invoice information to be transmitted to a tax authority’s system and be “cleared” before it can be sent. The “post audit” model is usually regulated by the European Union-backed Pan-European Public Procurement Online (Peppol) framework and more widely seen in Europe and is now adopted or is in the process of being adopted in Singapore, Japan, Australia and New Zealand. It involves the use of a third-party exchange for the information to be transmitted without any tax authority’s involvement. Consequently, the tax authority can conduct audits to verify taxpayers in the normal manner that we see today.

What is Malaysia planning to do?

Last year, former finance minister Tengku Datuk Seri Zafrul Tengku Abdul Aziz announced in the federal budget that e-invoicing would be implemented in stages from this year. This was followed by another announcement in October that the IRB and the Malaysian Digital Economy Corporation (MDEC) had entered into a memorandum of understanding to “establish strategic cooperation for the implementation of the national e-invoicing initiative”.

The announcement also makes clear that this initiative is part of a wider digitisation agenda for business documents — with a view to facilitate local and cross-border trade. IRB CEO Datuk Dr Mohd Nizom Sairi noted that e-invoicing would “create more transparent business transactions” that would aid in addressing the problem of the shadow economy.

Despite these announcements, there is little publicly available information that details Malaysia’s proposed strategy for adoption and implementation. We note that the country will implement it in phases, in accordance with what we have seen elsewhere. It is possible that Malaysia may do an initial pilot with selected companies or perhaps implement it on business-to-government (B2G) transactions before moving on to business-to-business (B2B) transactions. It is unlikely that we would see mandatory e-invoicing for all transactions in 2023.

It is also possible that the initial model implemented may be a post-audit model involving a third-party network not connected to the tax authority. The post-audit model would be easier to implement in a shorter space of time, as there is no need for the government or the IRB to invest heavily in building a network or infrastructure to enable the transmission and validation of the invoice data. Unfortunately, the post-audit method without the tax authority’s involvement would severely limit the IRB’s ability to target the shadow economy, as no data would be flowing directly to it.

What are the likely considerations for Malaysian businesses?

The planning would need to go beyond tax, as there are impacts to front-end and back-end systems and processes. Businesses will need to review their more permanent (master data) and transactional data to ensure information transmitted from their enterprise resource planning (ERP) through to its billing systems is correct in both format and substance. Customer, vendor management and existing standard operating procedures will also need to be reviewed and adjusted where necessary to ensure robust and sturdy processes exist around the e-invoicing transmission flow.

It is also likely that businesses would need to invest in software that would enable the transmission of data to the government/third-party network and to the customer. This software, also known as middleware, would need to be closely considered. Based on what we have seen in other countries, there are a number of approaches to this. Some businesses opt to create their own custom tools, some look to their ERP provider for add-ons or tools which are pre-made for their systems, while others look to third-party middleware vendors for software that sits external to the ERP but can interface across multiple financial systems.

Final thoughts

Tax in many organisations in Malaysia continues to be an afterthought, with little investment in technology or automation and a rather heavy reliance on manual processes. Consequently, business owners and heads of finance and tax do not have access to readily available, detailed and accurate tax-related information.

If this practice continues, there will be a significant risk as the government and the tax authority advance their digitisation journey for the authorities to have access to more significant and accurate data of a taxpayer’s business than the taxpayer.

Access to data, coupled with advanced analytics, will arm future tax auditors with significantly more tools and firepower than what many in-house tax teams will have at their disposal to counter potential findings made. The sooner businesses start focusing on transforming their tax functions, the greater the likelihood of keeping pace with the tax authorities, both locally and regionally.

Senthuran Elalingam is the tax technology consulting leader at Deloitte Malaysia

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Alibaba’s sudden American depositary receipt discount shows fear of US-China decoupling

- SNS Network partners with Nvidia to launch Malaysia’s first fully managed AI cloud service

- Insurance and takaful industry proposes measures to tackle rising healthcare costs, promote transparency

- China had record US$540b of exports in two months in rush to beat tariffs

- U Mobile, China Unicom Operations (Malaysia) forge partnership for IoT, smart mobility growth

- Wall St opens lower as jobs data disappoints; Powell's remarks awaited

- Recognise women judges for their legal acumen, not gender

- US energy chief will seek US$20b to refill oil reserve

- Capital A, Bumi Armada, SNS Network, MN Holdings, TNB, Econpile, Swift Energy, UEM Edgenta, Northeast, WTK

- US job growth picks up in February; unemployment rate rises to 4.1%