This article first appeared in The Edge Malaysia Weekly on September 12, 2022 - September 18, 2022

Malaysians just celebrated Merdeka Day, marking our 65 years of independence, last week. And Malaysia Day is just around the corner, on Sept 16. This should be the time to rejoice, to inspire, to be proud of the nation’s success. Hence, we understand that this article may upset some people, perhaps even raise questions about our agenda. Do we have one? You bet we do. Pretending to be an ostrich, burying your head in the sand, serves absolutely no purpose. Not acknowledging the underlying issues does not mean they do not exist. Problems will not be magically resolved. On the contrary, they create uncertainties and cautious expectations and, as we know, investors work on expectations. Indeed, to understand the enormity of the challenges the country is now facing — as we do — and to not speak up is the least patriotic thing any Malaysian can do.

We do not know if you have noticed, but many of our recent articles have focused on one key issue — investments. Investment is the single most important driver of economic growth in a nation. Investments create employment and raise the income level and well-being of the people. The role of the government is to facilitate a business environment that is most conducive to attract investments, be it by the domestic private sector or foreign investors.

The fact is Malaysia is falling behind in terms of attracting foreign direct investments (FDI) in the region. Our share of FDI flowing into Asean has fallen from 24% in 1977-1997 to just 8% in 2000-2020. And the fact is Malaysians (corporates, institutions and individuals) have been sending money out of the country at an accelerated pace (after capital controls were lifted in December 2002 and the ringgit-US dollar peg removed in July 2005) for more attractive returns instead of investing domestically. Investment as a percentage of GDP has fallen sharply since the Asian financial crisis (AFC). We have written at length on why this is so — the failure to properly address underlying structural weaknesses that have persisted for years, all of which have made Malaysia increasingly less competitive as an investment destination.

As a result, the country suffered from premature deindustrialisation. As investments declined, successive governments have sought to boost economic growth with short-term fixes. These included encouraging domestic consumption without corresponding income growth, which only led to falling savings rates and rising household debts. Raising government spending to stimulate demand and growth, à la Keynesian theory, is also largely a myth. Yes, it works in the short term but it is not sustainable and there are costs. To a certain extent, this is a weakness of all democratic governments. Most are, in effect, practising BNPL (buy now pay later) economic policies, that is, win over voters now, pay later. But snowballing debts must be repaid.

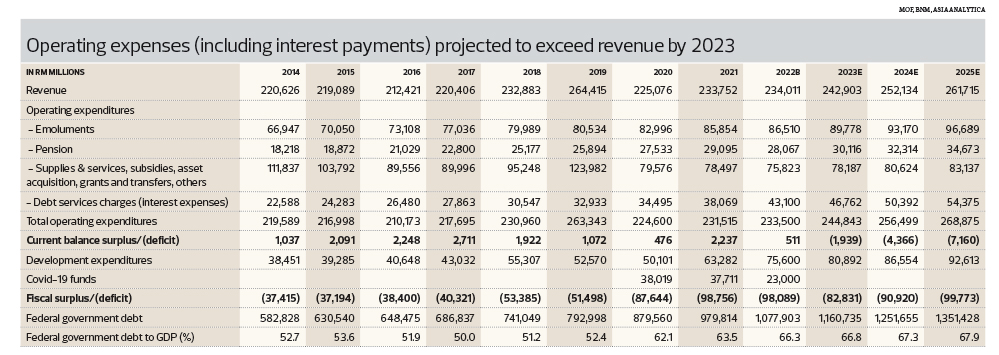

And this is where Malaysia now stands — on the edge of a precipice. There is no sugar-coating it. The table on Page 14 shows a summary of the financial situation of the public sector — total government revenue, operating expenses, debt servicing costs and development expenditures. (This would be similar to the profit and loss statement and capex of a company, but bearing in mind that the government uses cash accounting instead of the accrual method of accounting.) These are the actual historical figures for 2014 to 2021 plus the budgeted 2022 numbers as well as our projections for 2023-2025 (based on the average rates of change between 2014 and 2019, before the distortions due to the Covid-19 pandemic).

The most ominous statistic, based on the country’s current trajectory, is the expected current balance deficit in 2023 — and critically, its widening trend in 2024 and beyond. A current balance deficit means that revenue is insufficient to cover operating and interest expenses. If we were to look at Malaysia as a corporate body, then Federal Government Bhd would be making net losses.

While Malaysia has run fiscal deficits every year since the AFC, the government has always only had to borrow to finance development expenditure (capex). But our projections show that the country, by 2023, will have to borrow to service its debts! The thing is, once a company has to borrow to make interest payments, debt servicing costs will snowball — with more and more borrowings required to cover higher and higher interest expenses. Lenders will then surely demand higher interest rates (to compensate for rising risks) and finally, stop lending altogether. At that point, the company will be insolvent. A country will have more room to manoeuvre but make no mistake, there will be very serious fallouts.

How did we end up in this looming debt spiral?

As we mentioned, Malaysia has always had enough revenue to cover all operating expenses, including interest, save for two short years — 1986 and 1987. Indeed, in the immediate years following this shortfall, current balance surplus increased strongly and remained at healthy levels — until about 2008. That was a major turning point when expenses began growing faster than revenue, resulting in significantly smaller surpluses (see Chart 1).

As a result of dwindling current balance surpluses, Malaysia has had to rely more and more on borrowings to finance development expenditures. And as the total amount of debts grew, so did debt servicing expenses. In the five years before the pandemic (2014-2019), interest expenses grew by 7.8% per annum on average, the fastest clip among all other major expense line items. And remember, this was the period when globally, interest rates were in secular decline. In other words, the cost of borrowing was dropping, making debt cheaper. This trend has now reversed and interest rates are moving higher, at least for the foreseeable future. Even after the current hot inflation has peaked and price stability restored, interest rates may not return to previous lows for some time. In short, our projections are based on the best-case assumption — that the average interest cost remains unchanged from current levels. The reality, therefore, will likely be worse.

So, Federal Government Bhd was barely eking out “profits” for years. No thanks to years of profligate spending — made worse by unchecked wastages and theft — there was very little saved for a rainy day. And that rainy day came — in 2020. When the pandemic hit, much of the additional spending to alleviate economic hardship had to be funded through borrowings. The statutory debt ceiling was repeatedly raised, from 55% of GDP to 60% in 2020 and then 65% in 2021. There are now expectations that this will imminently be lifted to 70%.

The spike in borrowings puts a huge strain on the country’s financial position. Debt servicing as a percentage of revenue jumped from an average of 12% in 2014-2019 to 16.7% in 2020-2022. In other words, more government revenue now has to go towards servicing debt. This percentage is projected to keep rising in 2023 and beyond. Clearly, the current course that Malaysia is on is not sustainable.

What can (and cannot) be done?

Obviously, when expenses are greater than revenue, the answer would be (1) increase revenue and/or (2) reduce expenses. The latter could be through a combination of steep cost-cutting measures and debt restructuring — for instance, lower the interest costs. How probable is either action?

Government revenue, the biggest chunk of which is derived from various taxes (direct and indirect), has grown at a far slower rate than GDP over the past six years (2014-2019) — at 3.8% per annum on average, compared with 7% nominal GDP growth. We attribute this to the country’s narrow tax base, low income levels and stagnating corporate earnings growth.

We have written extensively on the structural problems leading to falling earnings for Malaysia’s largest listed companies — the earnings per share (EPS) on the FBM KLCI trended broadly lower between 2014 and 2019, which translated into flattish corporate income tax (see Chart 2). Note that the spike in 2021 was primarily due to RM5 billion in additional taxes from glove makers (which, as we know, have already fallen back sharply) and to a lesser extent, plantation companies, on the back of higher crude palm oil prices.

Tax contributions from plantation should remain relatively high in the short term but commodity prices are volatile and, therefore, not reliable as a steady source of revenue. Similarly, interest and returns on investment — primarily from Petronas — are closely correlated to global oil prices. We discussed some weeks back how Malaysia’s economy remained overly reliant on primary commodities despite years of industrialisation.

Meanwhile, only 16.5% of the country’s 15 million-strong workforce pay income tax, that is about 2.5 million (or less than 8%) out of Malaysia’s 32.7 million population. This is a very small base. Plus, there is a limit to how much higher personal income tax collection can go, especially if the country is not creating enough high-paying jobs.

Last year, the government announced a one-off prosperity tax in Budget 2022 to help pay for pandemic expenses. And there are calls to reintroduce the Goods and Services Tax (GST), which is a broad-based consumption tax. GST was hugely contentious and was a big issue during the last general election, GE14. It was eventually scrapped in 2018, after the change in government. We think it is highly unlikely to be reintroduced anytime soon, and especially not with the upcoming general election.

Raising taxes to pay for higher expenses does not promote investments or savings

But even if it could be done, finding additional tax revenue to pay for higher operating expenses is a bad option. Higher taxes will simply lead to an uncompetitive business environment. It does not promote investments or savings.

Government must reduce operating expenses

Therefore, the best solution is for the government to reduce expenses. Cutting expenses, especially on wastages, however, has proved to be equally daunting over the years. This is perhaps less surprising.

The democratic form of government can be a double-edged sword. Elections, at regular intervals, can prevent unchecked accumulation and abuse of power. But few, if any, populist governments have the political will to make the hard decisions that inflict pain on voters. Populist policies, on the other hand, are often short-term solutions that are not beneficial to the country in the long run. As we mentioned above, most democratic governments practise BNPL economic policies. This is a fundamental challenge for all democracies — and quite possibly one of the biggest weaknesses for this form of government.

Malaysia has extensive subsidy programmes, including for petrol and numerous food products. Petrol subsidies, in particular, have ballooned with higher global oil prices. Total subsidies are now estimated to reach RM80 billion, nearly five times the RM17 billion budgeted for 2022 — the higher subsidies will be partly offset by an additional RM25 billion in dividends from Petronas. There has been talk of replacing (or reducing) the current blanket subsidies with more targeted subsidies for the lower-income households. Again, is this politically palatable?

For the same reasons, there is zero chance of a smaller civil service or a cutback in salaries, emoluments and pension payments in the foreseeable future. In fact, we are seeing more populist policies, such as direct cash transfers to the people, to boost popular support.

If the reality is limited options for increasing revenue and cutting expenses, then more government borrowings appear inevitable. This is, in fact, what has been happening over the past few years. But we are very close to, if not already at, the point where we can no longer afford to kick the can down the road — without serious consequences.

Crowding out private-sector investments

One important fallout from rising public debt levels is the crowding out effect on the private sector. This is clearly evident in Chart 3. It is worrying that the percentage of government bonds bought by foreign investors has decreased over the past few years, and more government issuances are taken up by domestic institutions.

Obviously, lenders will always gravitate towards borrowers they perceive to be least risky (government) and/or require relatively higher premiums for riskier borrowers (private sector). In particular, the banking sector and, to a lesser extent, local institutions (such as the Employees Provident Fund and Kumpulan Wang Persaraan Diperbadankan), are holding an increasingly large percentage of government bonds.

As the government absorbs more of the available domestic pool of savings, it leaves less — and costlier — funding for the private sector. That means fewer investments, which as we have pointed out, repeatedly, is THE most important driver of future economic, productivity and income growth.

Of note, Bank Negara Malaysia’s holdings of government bonds have risen significantly over the last two years. In other words, the central bank is financing some of the government debts, whether directly or indirectly in the secondary market — or as the world calls it, quantitative easing (QE).

Limited QE during the pandemic crisis is a defensible move, to ensure sufficient liquidity and keep interest costs low to mitigate shocks to the financial system. A more protracted QE, though, will raise the perception that the central bank is monetising government fiscal deficits. This will, without doubt, damage investor confidence in its independence and in the country. And by printing more money, it will also create inflationary pressures — and asset bubbles. In the worst-case scenario, it could trigger runaway inflation. Case in point is Argentina, where inflation hit 71% in July this year.

Some may argue that Malaysia is not Argentina and that Japan is the poster child for unlimited QE, which the Bank of Japan (BoJ) has undertaken for more than a decade. The Japanese government has consistently run huge deficits, increasingly financed by the BoJ — and the yen has yet to suffer major repercussions, at least until recent months. But, in fact, the financial positions of Malaysia and Japan are very different (see sidebar for a more in-depth discussion on this topic).

Keeping interest rates low has serious long-term consequences

Yes, keeping interest rates low will make it easier for the people and government to service their debt levels. And yes, inflation will reduce the real value of debt, that is, future repayments will be worth less than the value when they were borrowed.

This is the obvious solution for most populist regimes — do not make the difficult (and unpopular) decisions. It is more palatable to keep interest rates low and allow the ringgit to depreciate, which is then easily blamed on global foreign exchange movements that are beyond a government’s control. But at what consequences to the future generation?

Make no mistake, maintaining ultra-low interest rates is a form of wealth transfer — from lenders (savers) to the borrowers (government) and asset owners. If we go down this road, responsible Malaysian savers will be penalised and asked to subsidise the less fiscally-disciplined, including government spending.

Worse, low interest rates discourage saving — especially if the interest rate is so low that it cannot even offset inflation (in effect, savers would be earning negative real returns) — and/or encourage people to invest in higher return assets abroad. This will result in even less money available domestically for investments.

Inevitably, capping domestic interest rates (relative to the rest of the world), and adding to money supply that results in high inflation will lead to capital flight (foreign and domestic) — and rapid depreciation of the ringgit. This would diminish the purchasing power of the ringgit and effectively destroy the savings of the people.

The nation has made great progress in raising the people’s standard of living in the 65 years since achieving independence. But the actions of past governments — the years of profligate spending and wastages — have led us to this critical crossroad. Instead of always going for short-term fixes, is it not time for Malaysia to finally acknowledge — and reform — the underlying structural issues?

Quite honestly, we see no good (painless) options. Short-term fixes will only exacerbate the challenges. And not acting will mean watching the country descend into a debt spiral — that will certainly bring even more pain as well as risking the well-being of future generations of Malaysians.

Over the past series of articles, we have spelt out some of the most critical structural issues that must be urgently addressed. First and foremost, we must reinvigorate investments by creating a business-friendly environment that promotes innovations. The education and training system must be able to provide the necessary talent pool to attract investors. The brain drain must be stopped and talents recruited from abroad. We can learn from the successes of others. Equality of opportunity and high social mobility — the quintessential American Dream — have proved to be great motivators in attracting and fostering talent, and removing rent-seeking activities. Singapore is the preferred hub for Asean because its public service is perceived as transparent, streamlined, efficient and absent of systemic corruption. The country is highly effective in planning and driving long-term industrial-investment strategies and has strong private property rights. Both the US and Singapore are among the top destinations in the world for investments. Investment is the answer to sustainable long-term growth — investments will spur innovations, boost productivity and corporate profits, create more and better-paying jobs, and lift per capita income for all Malaysians.

The Global Portfolio fell 2.5% for the week ended Sept 7, underperforming the MSCI World Net Return Index. The biggest losers were Yihai International Holding (-11.4%), Alibaba Group Holding (-7.3%) and Chinasoft International (-6.5%). There were only three gainers in the portfolio last week — Airbnb (+2.6%), Bank Rakyat Indonesia (+2.4%) and Guangzhou Automobile Group Co (+0.1%). Total portfolio returns since inception now stand at 20.3%, trailing the benchmark index’s 34.7% returns.

Total returns for the all-cash Malaysian Portfolio remained at 120.9% since inception. This portfolio is outperforming the benchmark FBM KLCI, which is down 18.5% over the same period, by a long, long way.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.