KUALA LUMPUR (Jan 4): The year 2022 could be akin to a perfect storm that gathered to punish equities performance last year. Stocks momentum in Bursa Malaysia was impacted by higher-than-ever inflation driven by slew of interest rate hikes by both the US Federal Reserve and Bank Negara Malaysia.

The FBM KLCI ended on Dec 30, 2022 with a decline of 3.46% from Jan 3, 2022. Several indices beat the benchmark’s performance in the same period including the Bursa Malaysia Finance Index (5.68%), the Energy Index (10.27%) and the Plantation Index (6.37%).

In Malaysia, several industries were also affected by labour shortage, higher minimum wage, as well as higher raw material costs and taxes.

Although the eventual termination of Covid-19 disruptions boosted consumer spending, rising inflation continued to spoil investor sentiments because of expected macro-economic tightening to curb inflationary pressures, said Fortress Capital Asset Management Sdn Bhd chief executive officer Thomas Yong.

As the curtain raised to 2023, will the old monsters rear their heads into this year?

According to CGS-CIMB Securities Sdn Bhd, 2023 is predicted to remain challenging as corporates adapt to the new policy and political landscape post-15th general election (GE15) and adjust to slower global growth, tighter monetary policy, and ongoing geopolitical tensions.

It may be inevitable that a challenging year looms ahead, but investors still can look forward to a pocket of opportunities, said analysts. The Edge CEO Morning Brief has compiled a list of potential stocks that may do fairly well in 2023 based on leading financial and research firms.

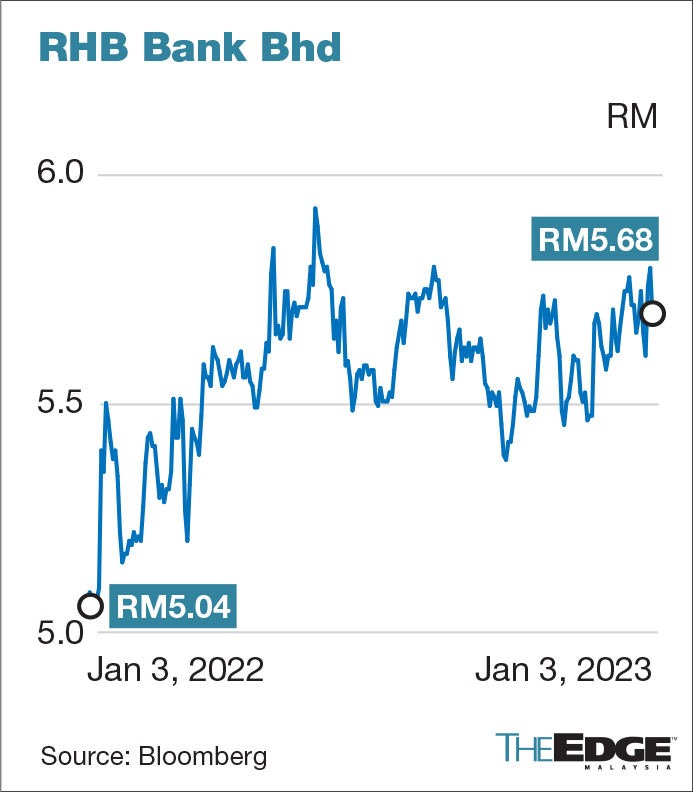

RHB Bank Bhd

Three research outfits, namely AmInvestment Bank Bhd, JP Morgan Asia Pacific Equity Research and CGS-CIMB Securities Sdn Bhd, have listed RHB Bank Bhd to leverage interest rate uptrend that will benefit the interest income of the bank with lower provision.

AmInvestment Bank noted that RHB Bank is one if its top picks for banks due to its valuation, which remains undemanding, trading at an attractive financial year 2023 (FY2023) price book-value (PB/V) of 0.8 times and strong capital position among peers with a Common Equity Tier 1 capital (CET1) ratio of 16.8%.

JP Morgan said RHB Bank has seen sharp shifts in strategies over the last decade which include some combination of credit risk revamp, divestiture of subscale or non-core businesses and varying degrees of digitisation of offerings. “As a result, return on equity (ROE) visibility for RHB has improved meaningfully for 2023-24,” said JP Morgan.

AmInvestment Bank has a target price (TP) of RM7.40 on the bank, while JP Morgan set it at RM6.50 per share and CGS-CIMB's TP for RHB is RM7.62.

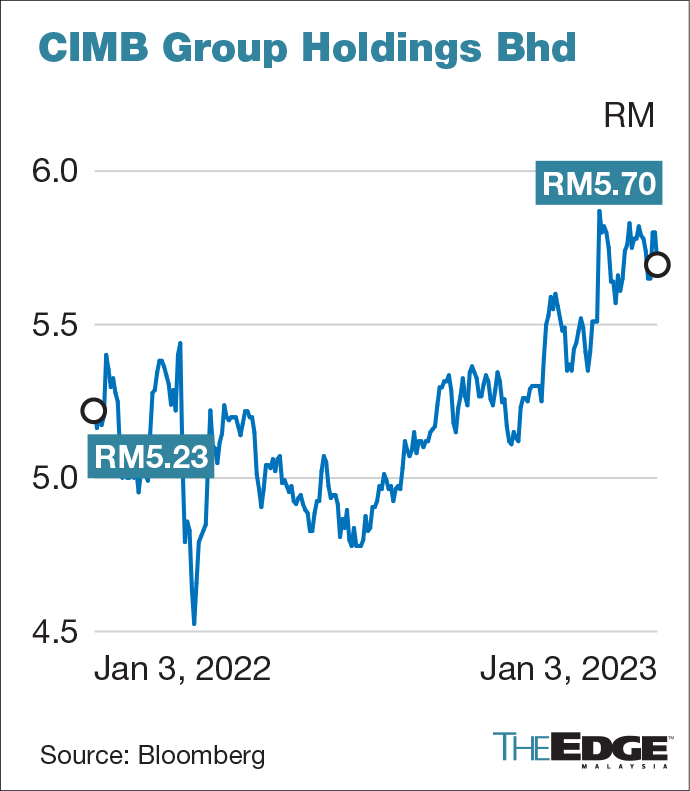

CIMB Group Holdings Bhd

The current positive market sentiment following GE15 is expected to spill over into the first quarter of 2023 (1Q2023) and continue to boost the banking sector, said UOB Kay Hian in a report.

“We opine that investors should take this opportunity to sell into strength by milking the last leg of a potential sector outperformance and taking positions in higher-beta large-cap banking stocks like CIMB Group which should outperform in a broad-based market in risk-on mode going into 1Q2023,” the research outfit noted.

Likewise JP Morgan said CIMB delivered a good turnaround on cost base as well as asset quality with return of equity visibility that has improved meaningfully.

Yong of Fortress added that banks had also made pre-emptive provisions and there is a possibility of provision write-backs if the economy slows down less than expected.

“Furthermore, the attractive dividend yield of the sector makes the sector a safe pick for institutional investors,” he added.

UOB Kay Hian ascribed a target price of RM6.50 per CIMB share, and JP Morgan set it at RM6.

Malaysia Airports Holdings Bhd

Malaysia Airports Holdings Bhd (MAHB) is expected to benefit from the strong recovery of passenger traffic volume that will drive earnings momentum of the airport operator.

“For 2023, we assume that domestic and international traffic volume would recover to 91% and 84% of 2019’s volume,” said UOB Kay Hian.

The research outfit added that the growth of MAHB is premised on rising optimism about the short-lived impact of the Omicron variant and locals’ mobility behaviour graduating to the endemic stage.

The pent-up travel demand amid consumers’ accumulated savings, and harmonising of entry coordination and border-crossing requirements within the Asean region are also expected to boost this counter.

CGS-CIMB added MAHB will also greatly benefit from the potential reopening of China’s borders sometime during 2023.

UOB Kay Hian maintained "buy" with a TP of RM7.52, while CGS-CIMB set it at RM7.48 per MAHB share.

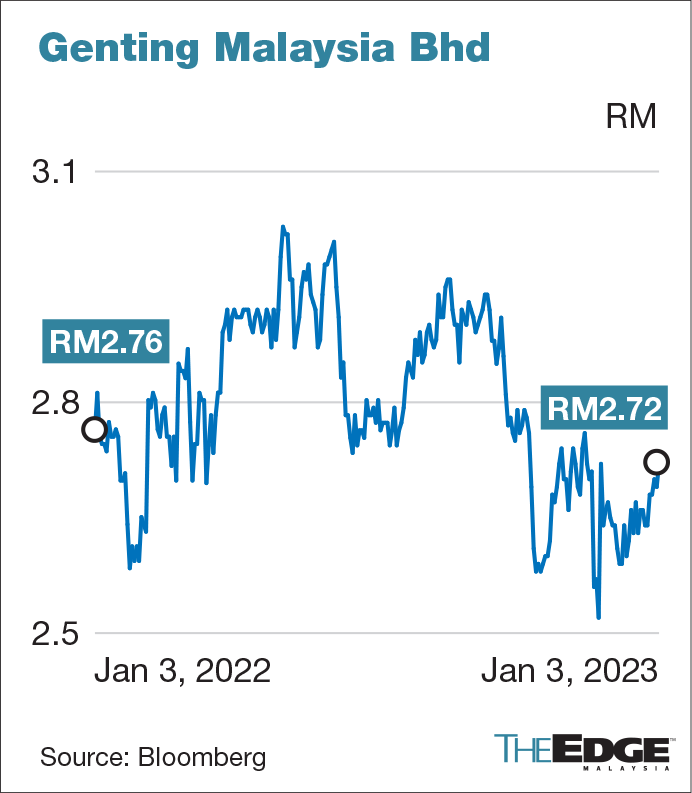

Genting Malaysia Bhd

Genting Malaysia Bhd has achieved 80-90% of pre-Covid earnings before interest, taxes, depreciation and amortisation (Ebitda) as of 3Q2022, signalling reopening recovery is on track, noted JP Morgan.

“Investors should focus on Genting Group’s balance sheet strength in 2023 as Genting's standalone net gearing stands at 177%. Malaysia's gaming market is 80% local driven; demand has been strong as visitation is almost back to pre-Covid,” the research outfit noted.

JP Morgan, however, said Genting Malaysia still needs to resolve its labour shortage issue as it is operating at 60-70% hotel capacity.

Public Investment Bank Bhd threw caution to the wind on tourism spending, noting the rate of recovery may be slower as consumer confidence remains weak due to inflationary pressures with a rising interest rate environment.

“Nonetheless, we believe that gaming stocks will continue to chalk higher earnings in 1H2023 (first half of 2023), driven by improvement in business volume. Genting remains our top pick. It should see stronger contribution from its subsidiary Genting Singapore, due to a gradual relaxation of Covid-19 measures in China that should lead to higher visitation of Chinese tourists,” the research outfit added.

UOB Kay Hian has a TP of RM3.50 on Genting Malaysia while Public Investment set it at RM3.28 per share.

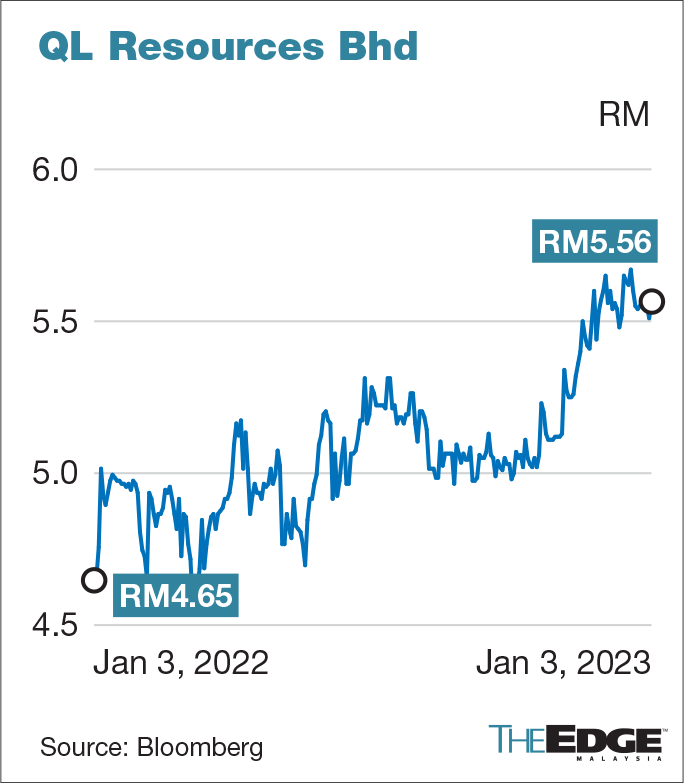

QL Resources Bhd

CGS-CIMB and MIDF put QL Resources Bhd as their top pick in the consumer sector, which they believed would be driven by strong demand for staple products in 2023.

CGS-CIMB said QL Resources will benefit from the government’s move to lower cost of living and raise household disposable incomes, especially for the lower- to middle-income earners.

CGS-CIMB added that QL Resources is a potential beneficiary of China’s relaxation of its zero-Covid policy that may be more evident in 2H2023, as it believes QL Resources has exposure to Chinese consumers.

Likewise, MIDF said it believes QL Resources will benefit from the rising demand for marine products as well as global shortage of chicken and eggs.

MIDF said its economists anticipate that private consumption growth will continue to increase in 2023 at a rate of 6.6%.

CGS-CIMB has a TP of RM6.50 for QL Resources while MIDF set it at RM6.30.

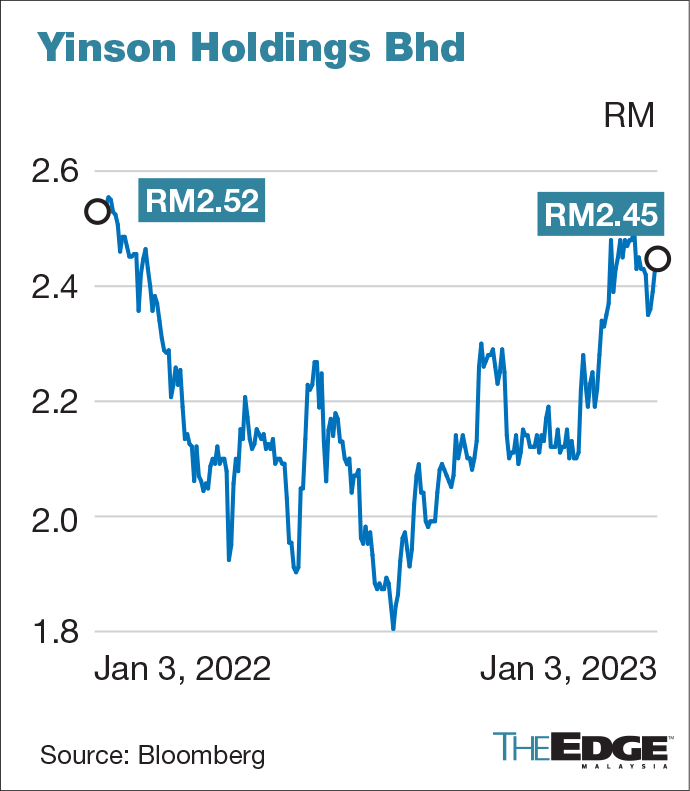

Yinson Holdings Bhd

UOB Kay Hian chose Yinson Holdings Bhd as the top stock for the company’s delivery of existing floating, production, storage and offloading (FPSO) contracts and potential new FPSO contract wins.

UOB Kay Hian added that Yinson is expected to have the highest future earnings growth among the oil and gas (O&G) stocks under its coverage.

“In detail, its financial year 2023 earnings base may triple to more than RM1.3 billion by financial year 2026 (with FPSO Agogo becoming operational), and at our TP this implies a 12 times price-earnings ratio after the Agogo deal.

UOB Kay Hian set a TP of RM4.45 for Yinson.

AmInvestment Bank said O&G is an overweight sector expected for robust earnings growth from elevated oil prices supported by prolonged supply disruptions and past underinvestment.

“Companies with direct exposure to the upstream production and the FPSO subsector would be the biggest beneficiaries,” AmInvestment said.

AmInvestment set a fair value of RM3.89 for Yinson.

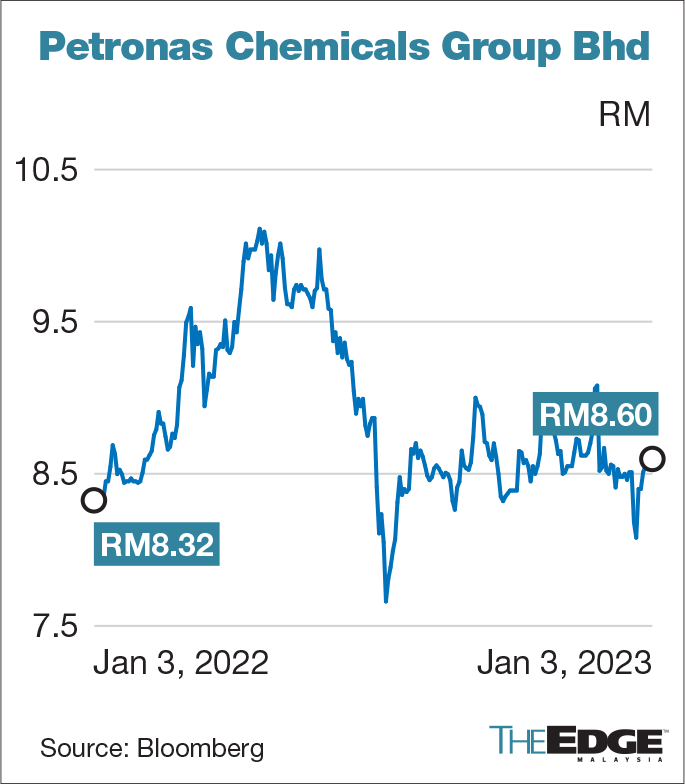

Petronas Chemicals Group Bhd

JP Morgan said the firm is constructive on Petronas Chemicals Group Bhd (PetChem) based on its exposure to nitrogen-based fertilisers in Asean.

The firm expects a higher overall fertiliser and methanol (F&M) utilisation for the financial year 2023, as well as elevated nitrogen fertiliser prices and demand during the summer planting season in January to February 2023, to remain a key catalyst for PetChem.

“We are overweight on PetChem thanks to its fertilisers earnings, cheap gas feedstock, and positive ringgit-depreciation impact,” JP Morgan said.

It also sees the bullish oil price to benefit chemical prices.

MIDF chose PetChem as its top pick for downstream stocks in the O&G sector, stating that it believes retail and commercial fuels to be in high demand in 2023.

“The petrochemical sub industry is also anticipated to remain robust in our local front, as Pengerang Integrated Complex — the primary hub for petrochemicals in the region — is expected to be in full operating capacity by mid-2023,” MIDF said.

JP Morgan has a TP of RM11 while MIDF set it at RM11.77 for PetChem.

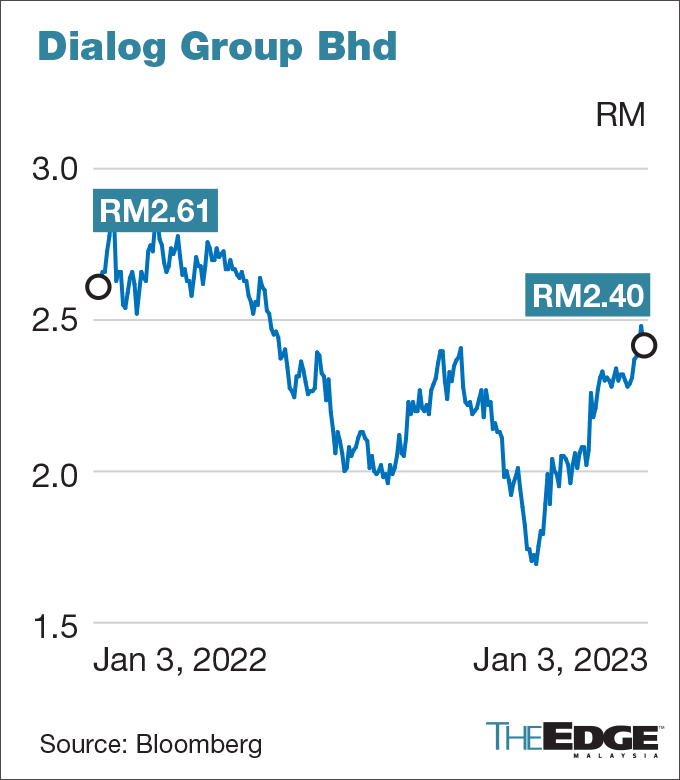

Dialog Group Bhd

AmInvestment Bank placed Dialog Group Bhd among the firm’s top "buy" calls as it perceived the improving sector recovery on bullish crude oil prices poised to spur recurring services growth with the group's strategic Pengerang development to likely bring in new investors.

The firm added that it likes Dialog on the back of its resilient non-cyclical tank terminal and maintenance-based operations.

MIDF also puts Dialog as its top buy according to its 2023 market outlook report.

In the firm’s Nov 16 note on the group, MIDF is confident that Dialog will continue to be resilient amid the challenging economic environment after posting a 2.4% year-on-year decline in earnings to RM125.8 million for the first quarter of the financial year ending June 20, 2023.

“Considering that a stable oil price trend is expected for 2023, we opined that the group’s financial performance is on the right track,” MIDF said.

“We are positive that Dialog will continue to strengthen its competitiveness via its storage tank farm business, international upstream operations, engineering and fabrication services, recycled PET (polyethylene terephthalate) production facility, and technology and digital transformation initiatives.”

AmInvestment Bank put a fair value at RM3.38 for Dialog. Meanwhile, MIDF set a higher TP of RM3.70 on Dialog.

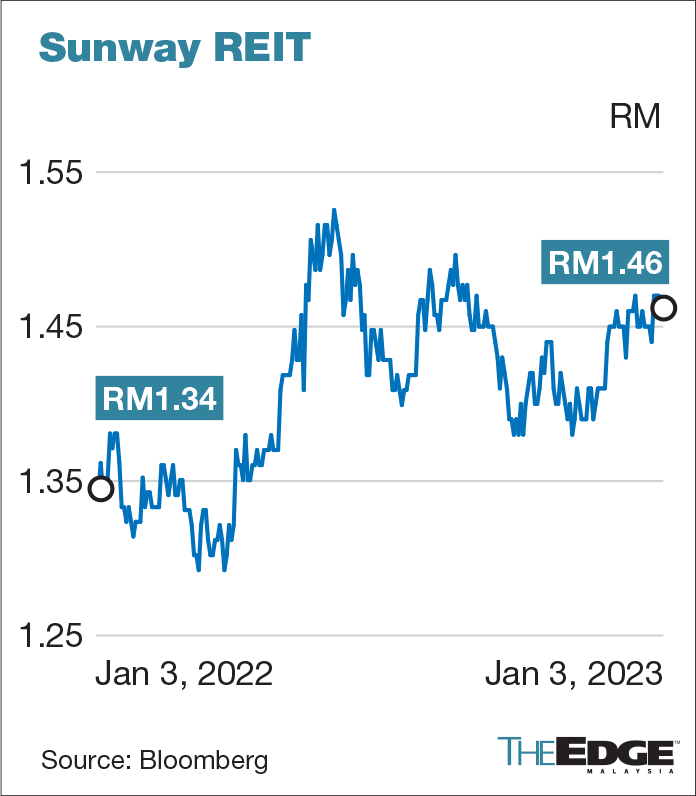

Sunway Real Estate Investment Trust

AmInvestment Bank said it had Sunway Real Estate Investment Trust (Sunway REIT) as its top pick for the perceived overweight REIT sector due to the group’s diversified investment portfolio, which encompasses retail malls, hotels, offices, a university and hospitals across Malaysia.

It highlighted that Sunway REIT has a strong occupancy rate which has exceeded 90% in retail assets, as well as stable rental income generated from the REIT’s services and industrial segments.

AmInvestment Bank added that Sunway REIT is among environmental, social and governance (ESG) champions which has incorporated sustainable financing consideration into capital management strategies via the issuance of sustainability-linked bonds.

MIDF said Sunway REIT's earnings in 2023 will be underpinned by positive rental reversion of Sunway Pyramid as well as higher shopper footfall. It added that Sunway REIT’s exposure to the hotel industry will also benefit from the recovery of the tourism industry in 2023.

Both AmInvestment Bank and MIDF set a TP of RM1.73 on Sunway REIT.

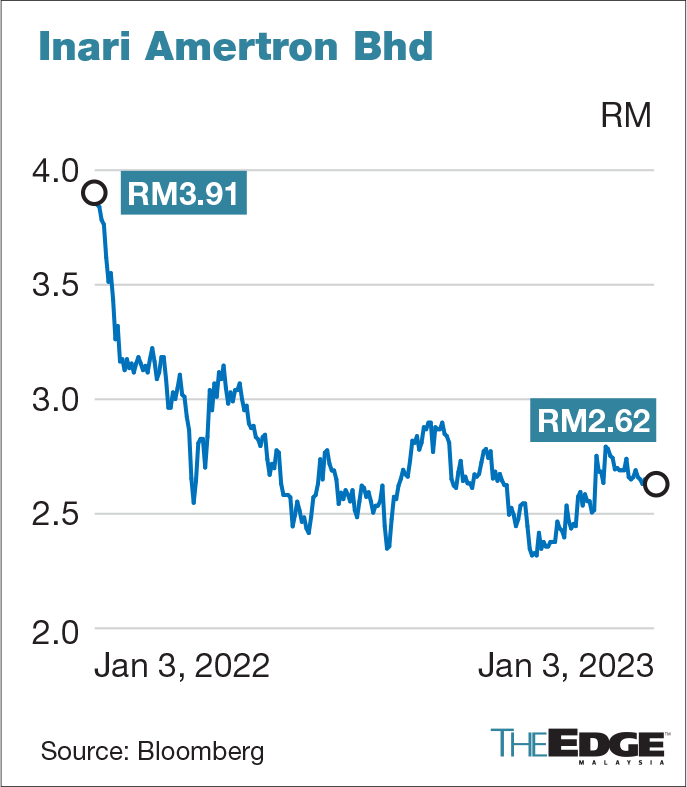

Inari Amertron Bhd

MIDF said its top pick for semiconductor players is Inari Amertron Bhd given the company’s exposure in the radio frequency (RF) segment.

Inari belonged in the technology sector, which MIDF has a positive view of in 2023.

MIDF said the growth prospects for the sector stay intact, supported by the emerging technologies like 5G, Internet-of-Things (IoT), artificial intelligence (AI), personal computers (PCs), Cloud, and electric vehicles (EVs).

“We opined that the selldown of the tech sector might be overdone and thereby provide opportunities to forward-looking investors to place their investment in a growth stock,” MIDF said.

Public Investment also retained Inari as a suggested pick for 2023 amongst the smaller-capitalised stocks. The bank said it expects Inari to likely see multi-year growth stories and earnings stability.

Similar to MIDF, Public Investment said the management is particularly upbeat on the RF component outlook with strong double-digit growth. The bank also believes Inari for higher earnings contributions from new product offerings in the assembly of next-generation phone cycles.

MIDF recommended a TP of RM3.20 for Inari, while Public Investment suggested RM3.74.