This article first appeared in The Edge Malaysia Weekly on December 12, 2022 - December 18, 2022

LOW-cost carrier Capital A Bhd (CapA) and its medium-haul affiliate AirAsia X Bhd (AAX) have confirmed a report by The Edge that the former will sell its aviation business to the latter in exchange for AAX shares. This exercise will help lift the companies out of their Practice Note 17 (PN17) status.

Post-restructuring, CapA will be a pure digital group with maintenance, repair and overhaul (Asia Digital Engineering), logistics (Teleport), digital (airasia Super App) and fintech (BigPay Malaysia Sdn Bhd) businesses. AAX, which will be rebranded as AirAsia Group, will comprise six airlines — AirAsia Bhd, Thai AirAsia, AirAsia Indonesia, AirAsia Philippines, AAX Malaysia and Thai AAX.

The group also envisioned a separate spin-off listing in the future for the digital businesses of CapA once the PN17 status is resolved, according to CapA CEO Tan Sri Tony Fernandes. This is not surprising given that he had said over the past year that the group was weighing a US listing for its digital businesses.

But valuing a technology company is tricky in a year when financial markets have been so volatile and tech valuations have dropped sharply.

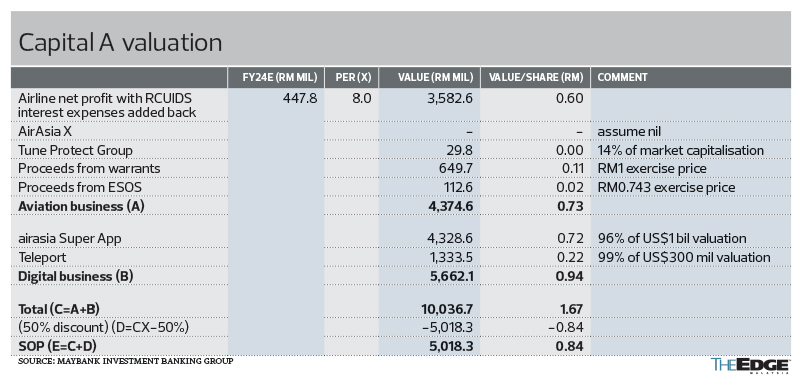

In fixing a target price of 84 sen for CapA in a Dec 1 report, Maybank Investment Bank analyst Samuel Yin Shao Yang valued the group’s digital assets at RM5.66 billion or 94 sen per share — more than the group’s market value of RM2.37 billion as at last Wednesday, on which the stock closed at 57.5 sen.

This has raised questions about the basis for Maybank IB’s valuation of a business that is still burning cash. At RM5.66 billion, its valuation is higher than that of profitable companies such as Bursa Malaysia Bhd, Chin Hin Group Bhd and Frontken Corp Bhd.

In arriving at this valuation, Yin says the RM5.66 billion only takes into account the airasia Super App and Teleport. “In July 2021, when CapA acquired Gojek’s operations in Thailand in return for a 4.76% stake in airasia Super App, the deal valued airasia Super App at US$1 billion. Similarly, Teleport’s acquisition of Delivereat for US$9.8 million in August 2021 valued the logistics unit at US$300 million,” he explains to The Edge.

“Bear in mind that these valuations were made during the easy money era — a time when it was easier to raise cash and [valuations] were high even though the units were loss-making. If anyone were to raise money today, the valuations would quite likely be lower than last year. If you look at tech companies like Grab Holdings Ltd and Sea Ltd, they are postponing their funding rounds because the implied valuation will probably be lower than last year.”

He adds that he had applied a 50% discount to the valuation of airasia Super App and Teleport in 2021 to calculate their present value.

Yin points out that unlike Grab and Sea, which currently command market capitalisations of US$11.32 billion and US$26.45 billion respectively, and do not yet have earnings before interest, taxes, depreciation and amortisation (Ebitda), airasia Super App reported positive Ebitda in the third quarter ended Sept 30 (3QFY2022). Teleport was also Ebitda positive, supported by increased bellyhold capacity.

“airasia Super App went from break even in 2QFY2022 to generating an Ebitda of RM15.8 million in 3QFY2022, as gross booking value surged 49% quarter on quarter. At a recent analysts’ briefing, CapA said 4QFY2022 looks even better,” he adds.

Yin notes that in the last few years, a lot of emphasis had been put on sales growth to calculate the valuation of a tech company, rather than looking at the losses. “[The end of the big tech boom and as the share prices of many de-special purpose acquisition companies (SPACs) crashed,] investors are now looking at the bottom line too and airasia Super App is at least showing Ebitda. If it can maintain this growth trajectory and continue to generate positive Ebitda, it will be easy to justify CapA’s digital assets valuation compared with Grab and Sea.”

Forget insane valuations

An investment banker who spoke on condition of anonymity concurs, noting that Southeast Asian tech companies have seen their valuations fall since going public.

For example, Indonesia-based PT GoTo Gojek Tokopedia Tbk has lost more than 70% of its initial valuation of US$28 billion since its Jakarta debut in April. Rival Grab has lost 72% of its initial valuation of about US$40 billion since its US listing in December 2021 via a SPAC, while e-commerce company PT Bukalapak.com Tbk is down about 71% from an initial valuation of US$6 billion since its Jakarta initial public offering in August 2021.

“Globally, investors are now actually asking these tech start-ups to show a clear path to profitability and when they will start making money. Those days, when investors such as private equity firms and venture capital firms just threw money at tech companies to take market share and worry about the profit later, are over. That is because a lot of these guys have already invested for a number of years and their investment horizon of five to seven years is coming up, and yet the companies they have invested in have no returns to show,” he tells The Edge.

The investment banker points to Malaysia-based unicorn Carsome, which was valued at US$1.7 billion in its last funding round, and its recent move to shelve plans for a dual listing, which had been set for this year in Singapore and the US, given the current volatile market conditions and economic headwinds.

Why tech firms should prepare for lower valuations

At the other end of the spectrum to Maybank IB’s Yin’s estimate is Kenanga Research analyst Raymond Choo Ping Khoon, who gave a valuation of only RM996.8 million for CapA’s digital assets. “We value AirAsia’s digital assets at a 30% discount to e-wallet operator Boost’s US$320 million, given their similarity in terms of being digital platforms targeting the same geographical areas, although we acknowledge that AirAsia’s digital assets are not strictly comparable to Boost,” he wrote in a Dec 1 report.

According to Choo, Boost — the fintech arm of Axiata Group Bhd and Payments Network Malaysia Sdn Bhd — boasted 7.5 million users and 170,000 merchant touchpoints at the point of the funding round that fetched a US$320 million valuation in 2020. This compares with the 11 million users and 32,000 merchant touchpoints of AirAsia’s digital assets currently.

“We also take into consideration the sharp fall in the valuations of tech start-ups in the private markets over the last six months, reportedly to the tune of as much as a third on the back of the regulatory crackdowns in China as well as the Nasdaq’s sell-off,” he added.

Choo notes that looking at 2023, CapA’s digital segment is expected to remain loss-making. “airasia Super App is expected to grow, underpinned by the continued resurgence of travel demand from borders reopening and tactical campaigns, alongside expected growth from airasia Food, Ride and Xpress. Additionally, Teleport is expected to continue expanding throughout 2022 as it increases new international lanes and delivery hubs. BigPay has also launched its digital lending platform to provide new loan products.”

However, he is mindful of its digital assets’ persistent cash burn. “BigPay remains in the red due to ongoing investment costs.”

Filings with the Companies Commission of Malaysia show that BigPay had a net worth of RM23.05 million as at Dec 31, 2021. Its net loss widened 12.9% to RM66.66 million in the financial year ended Dec 31, 2021 (FY2021) from RM59.06 million in FY2020, while revenue rose 20% to RM20.28 million from RM16.9 million during that period.

Meanwhile, Choo values CapA’s airline assets at RM1.5 billion, based on FY2023 price-earnings ratio (PER) of 10 times, a discount to its peers’ average due to its smaller market capitalisation. “We continue to like CapA as it is a beneficiary to the recovery in air travel as the pandemic comes to an end; its growing digital business, which leverages its strong AirAsia brand and AirAsia’s existing client base; and its dynamic and visionary leadership that should help to steer it out of the current financial difficulty.”

Maybank IB’s Yin values CapA’s airline operations at RM3.58 billion, with a PER of eight times based on estimated FY2024 earnings of RM447.8 million. Including the contributions from AAX and Tune Protect Group, as well as the proceeds from warrants and employee share option scheme, the sum-of-parts valuation for the aviation business works out to RM4.37 billion or 73 sen per share (see table).

“For the digital assets, there is a lot of room to grow. On the airline side, what they can hope for is for it to recover to pre-Covid-19 pandemic levels. But whether it will go beyond that, I am not so sure yet,” he says.

CapA has until January 2023 to submit its PN17 regularisation plan to the regulator and six months from then to complete its regularisation. However, the company is seeking an extension until July 2023 to submit a holistic PN17 regularisation plan and is awaiting the reply of Bursa Malaysia. The group plans to announce the details of its regularisation plan by end-January 2023, with completion expected by July.

“It is hoped that the sale of its aviation business will result in a gain on disposal that will be enough to offset its negative shareholders’ equity position of RM7.07 billion as at end-3QFY2022. However, the number of AAX shares swappable for CapA’s aviation business has not been set yet,” says Yin.

CapA’s net loss widened to RM2.74 billion for the cumulative nine months ended Sept 30 (9MFY2022) from RM2.23 billion a year earlier, while revenue came in at RM4.24 billion, up 317% year on year. Its cash balance fell to RM415 million at end-3QFY2022 from RM632 million at end-2QFY2022.

“Around RM944 million of debt was also raised during 9MFY2022, and management is targeting to close an additional RM1 billion debt by 1Q2023. We understand that the borrowing rates for these were relatively high, considering the risk profile of the airline business,” said Nomura Global Markets Research analysts Ahmad Maghfur Usman and Divya Thomas in a Dec 1 report.

Meanwhile, AAX reported a net profit of RM32.83 billion on revenue of RM538.88 million for the cumulative 15 months ended Sept 30, 2022, after writing back RM33 billion to profit as the group completed its debt restructuring in March. In August, it changed its financial year end to Dec 31 from June 30. Its cash balance stood at RM79.5 million at end-September, from RM25.4 million at end-June.

“With its track record of its ability to gain investor confidence, there should be a bright spot for CapA to raise sufficient funding. Looking at the past digital IPOs, many of them managed to gain good valuations. However, uncertain market conditions and rising interest rates in recent years have limited the amount of venture capital funding and caused their share prices to be volatile,” says the investment banker.

According to data compiled by SPAC Research, 83 new blank-cheque companies have raised only US$13.2 billion in the US so far this year, paling in comparison to the record US$162.5 billion collected by 613 SPACs for the whole of 2021.

Having said that, following a record year for SPAC IPOs, the sky-high valuations and massive influx of liquidity that private tech companies experienced in recent times are over. “The tech financing market over the next three to five years will look like a rollback to more reasonable valuations,” says the investment banker.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- China hits back at Trump with tariffs, limits on key exports

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Trump hits China tariff retaliation, says policy will remain

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market