This article first appeared in The Edge Malaysia Weekly on October 24, 2022 - October 30, 2022

LOANS to small and medium enterprises (SMEs) are continuing to grow at a healthy rate, thanks in part to government support. In view of rising inflation and interest rates, however, as well as growing risks of a global recession next year, how SMEs hold up bears watching, say analysts.

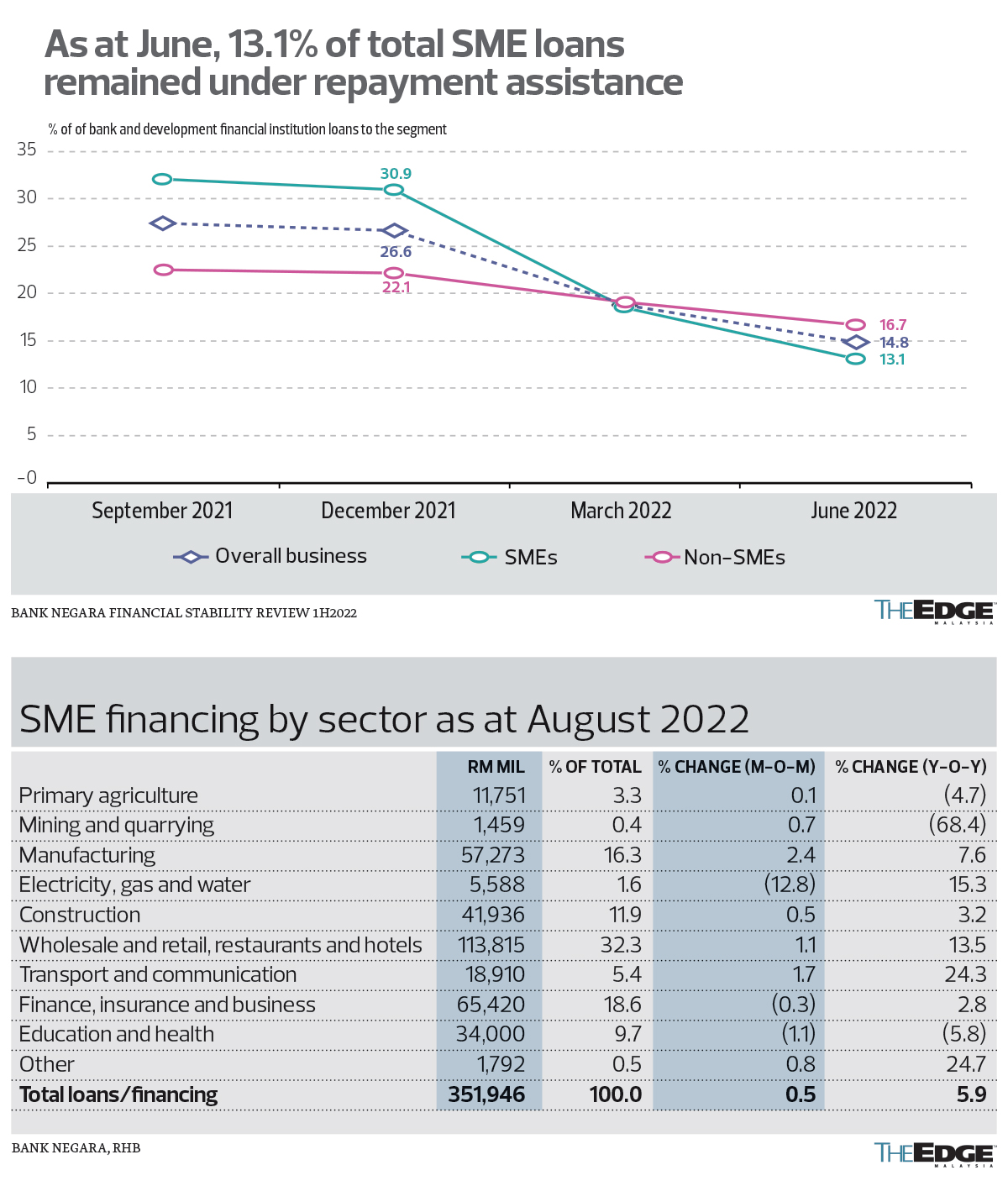

As it is, SMEs are just starting to emerge from the Covid-19 pandemic.

Bank Negara Malaysia’s latest data on the banking system shows that SME loans’ gross impaired loan (GIL) ratio — an indicator of asset quality — deteriorated to 2.97% in August, from 2.92% in the previous month and 2.73% a year earlier.

In contrast, the GIL ratio for overall loans in the system improved marginally to 1.84% in August from 1.83% in the previous month, although it deteriorated from 1.68% in December 2021.

“Pressure on SME asset quality seems to be rising,” says RHB Research analyst Fiona Leong, noting the 24-basis-point rise in the GIL ratio over the one-year period. “We believe, however, that this is within expectations, given the expiry of certain loan repayment assistance programmes [earlier this year]. Banks will continue to provide support for SMEs — especially those that are still recovering from the negative effects of the pandemic.”

SME loans in August grew 5.9% year on year and 0.5% month on month, driven mainly by loans to the manufacturing sector as well as the wholesale and retail trade sectors.

Banking sources say the SME business is growing faster than they can hire relationship managers to handle their customers. The problem is compounded by a shortage of talent in the industry, even as an increasing number of people move to Singapore, attracted by its strong currency.

“There is such hot demand for relationship managers in the SME segment, in particular,” one banker tells The Edge.

What the banks say

A check by The Edge with local banking groups such as AMMB Holdings Bhd (AmBank Group), CIMB Group Holdings Bhd and RHB Bank Bhd found that they have indeed been growing their SME loans at a strong pace, but not all foresee stress in their asset quality.

AmBank’s managing director for business banking, Christopher Yap, says the GIL ratio of its SME portfolio improved to 2.73% in June from 3.29% a year earlier.

“With the reopening of the economy, we are seeing [that] SMEs should be able to generate cash flow to meet repayment obligations. The most important thing for SMEs is their ability to generate cash flow. We don’t foresee stress in the asset quality,” he tells The Edge.

Nevertheless, he acknowledges that SMEs’ recovery from the pandemic will be challenging, given rising costs, labour challenges and an “unstable environment”. At the same time, SMEs will already need to start looking at ESG (environmental, social, and governance) adoption as Malaysia moves towards becoming a net-zero emission country.

“Those that have adopted Industrial Revolution 4.0 and digitalisation will have an upper hand in facing these challenges,” says Yap.

The bank has forecast Malaysia’s gross domestic product growth at more than 6% this year, double that of last year’s 3.1%.

“Most SMEs, especially the larger ones, will have sufficient margin for now to weather rising costs and inflation,” he says.

AmBank’s SME loans grew 9.2% to RM24.9 billion in the financial year ended March 31, 2022 (FY2022), reflecting an improved outlook. This was stronger than the bank’s overall loan growth rate of 6.5%. According to Yap, SME loans under repayment assistance or restructuring as at June stood at RM1.7 billion.

He expects SME loans to expand by RM2.1 billion in FY2023, the same as in FY2022. “We foresee a double-digit growth for the SME segment,” he remarks.

Of the country’s eight local banking groups, AmBank has the second-highest exposure to SME loans after Alliance Bank Malaysia Bhd. Its SME loans accounted for 21.3% of its overall loans as at end-June.

Meanwhile, RHB Bank’s head of SME banking Yip How Nang says its SME asset quality has remained resilient and “in line with expectations”, despite the tough operating environment, and the bank continues to intensify efforts to help its customers recover and build resilience.

“This has contributed to the steady improvement in our GIL ratio since May 2022,” he says, without providing details of where the ratio stands. “To assist them further, we continue to extend to our SME customers the necessary support, which includes providing access to new funding, championing Bank Negara Malaysia-initiated funding schemes to assist SME recovery, through R&R (rescheduling and restructuring) programmes, as well as provide repayment assistance especially to our most vulnerable borrowers.”

According to Yip, the recovery of some businesses, such as those in the construction industry, continues to be dampened by economic challenges. “On the other hand, we have seen rapid improvement in the services industry, where there has been a drastic rebound in business performance,” he notes.

As for repayment assistance, more than 90% of expired deferments for RHB Bank’s retail and SME segments had resumed payments as at July 31, he says.

Yip reckons that SME loan growth is likely to soften in 2023 and 2024, owing to continued challenges in the macroeconomic environment. He says the bank nevertheless strives to continue outpacing industry growth for SME loans and expects its SME loan book to grow by 8% in 2023.

RHB Bank’s SME portfolio stood at around RM26 billion as at end-June, accounting for about 13% of the bank’s overall loans.

CIMB tells The Edge that it has seen a slight uptick in delinquency in its SME portfolio, following the expiration of the government’s Pemerkasa and Pemulih relief packages this year.

“The GIL ratio has had a marginal increase since 2021, but it still remains at a healthy ratio,” it says, without disclosing the ratio.

It notes that rising inflation and interest rates have affected demand and cost, squeezing the margins of SMEs further. “However, we are currently seeing minimal impact on our SME customers, as we continue to provide financial assistance and debt relief programmes to those that are still recovering post-pandemic.”

CIMB says while the majority of its SME customers came out of the pandemic well, the recovery was not the same across all sectors. “Some, such as the tourism industry, are still experiencing the long-standing impact of Covid-19 and will require further assistance from us, as they may need a longer period for recovery,” it states.

The bank is expecting “positive” SME loan growth this year and next, particularly in terms of working capital financing, as it aims to empower “business revitalisation” post-pandemic.

“We have seen the demand for financing increasing, despite current challenges on cost of doing business due to supply chain disruptions, cost of financing (interest rates) and labour shortages. Guided by our lending and risk control mechanism under the Forward23+ strategic plan, we are confident [of meeting] our projections, barring any unforeseen interruptions to market and business,” it says.

CIMB’s SME loans stood at around RM52 billion as at end-June, making up 13.2% of the group’s overall loan book.

Solving talent shortage with digitalisation

RHB Bank’s Yip believes the talent shortage in the industry has no significant impact on the growth of its SME business, given the bank’s continuous focus on digitalising key processes.

“This has greatly enhanced our efficiency and service levels through our digital channels. Today, more than 60% of our SME loan applications are received through our digital channels. We also continue to invest in talent development, where young graduates are put through multiple structured programmes over a few years to develop them into relationship managers,” he says.

AmBank’s Yap, too, believes investing in digitalisation is important to manage the talent shortage.

“We aim to support relationship managers by providing digital tools and simplifying processes to elevate their throughput. Since [digitalisation], our turnaround time for the processing of loans has been reduced by more than half. Loans are processed within four to seven days now versus 20 days before digitalisation,” he says.

In addition, productivity has increased twofold. “So far, productivity is RM24 million loans (approved and accepted) per relationship manager per year, versus RM12 million previously,” Yap says.

He notes that recruitment drives are also an important mitigating factor for the talent shortage. AmBank hires fresh graduates and trains them to be SME relationship managers, especially in credit and lending expertise. It also has programmes in place to groom talent internally.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.