This article first appeared in The Edge Malaysia Weekly on December 27, 2021 - January 2, 2022

Mid Valley Megamall (MVM), one of the two core assets of IGB Real Estate Investment Trust (IGB REIT), was built during the Asian financial crisis. The group’s massive investment in building offices, a big shopping mall as well as a hotel was met with scepticism at the time.

But the group — co-founded by brothers, the late Datuk Tan Kim Yeow and late Datuk Tan Chin Nam — has proved the sceptics wrong. The developments on the plot of prime land have made the IGB group the largest landlord in town while going through several economic cycles.

The Covid-19 pandemic, however, seemed to have caught IGB REIT off guard, just as it did most retail malls around the world. The coronavirus outbreak resulted in the implementation of the Movement Control Order (MCO), and the usually bustling MVM and The Gardens Mall became quiet because footfall fell drastically as shops were ordered to close.

The group’s net property income (NPI) declined 20.6% to RM316.68 million in the financial year ended Dec 31, 2020 (FY2020), from RM398.79 million in FY2019. This is the first income contraction IGB REIT has seen since it was listed in 2012.

In The Edge Billion Ringgit Club’s (BRC) review period, from 2018 to 2020, the retail REIT’s NPI was on an upward trend before the Covid-19 outbreak. Its NPI increased to RM386.25 million in FY2018 from RM373.56 million in FY2017, climbing further to RM398.78 million in FY2019 — the highest level achieved so far.

The REIT rewarded its unitholders with a distribution per unit (DPU) of 9.19 sen in FY2018, and 9.16 sen in FY2019, compared with earnings per unit (EPU) of 9.45 sen and 8.91 sen respectively. In FY2020, as a result of the income fall, it declared a lower DPU of 6.75 sen versus EPU of 6.65 sen.

The group’s return on equity (ROE) remained at 9.1% in FY2018 and FY2019, but declined to 6.9% in FY2020.

With that, IGB REIT delivered a weighted ROE over FY2018-FY2020 of 8%, which still outperformed its peers with a market capitalisation above RM1 billion.

The group’s NPI remained under pressure in FY2021, owing to the resurgence of new Covid-19 cases and the emergence of new variants. Its NPI fell 18.8% to RM181.4 million for the nine months ended Sept 30, 2021 (9MFY2021), from RM223.6 million a year ago, while gross revenue dropped 11.8% to RM280.16 million from RM317.73 million.

Despite the current reopening of retail trades and some initial signs of a recovery in business and economic conditions, IGB REIT says its prospects remain cautiously optimistic.

“IGB REIT is determined to stay resilient throughout the Covid-19 pandemic and the subsequent endemic phase. It remains committed to bringing about long-term value for its stakeholders,” it says.

Among the 13 investment analysts who track the REIT, seven have a “buy” call while six are recommending a “hold”. There is no “sell” call on the stock.

CGS-CIMB Research says in an Oct 27 note that although 9MFY2021 was a challenging period for the retail sector, it gathered that both MVM and The Gardens Mall managed to sustain healthy occupancy rates of over 90%, while average weekend footfall since late September has improved to 80% to 85% of pre-Covid-19 levels.

The research house maintains its EPU forecast on IGB REIT for FY2021 to FY2023. It also projects robust core EPU/DPU growth of 21% year on year in FY2022, amid expectation of a recovery in the retail sector.

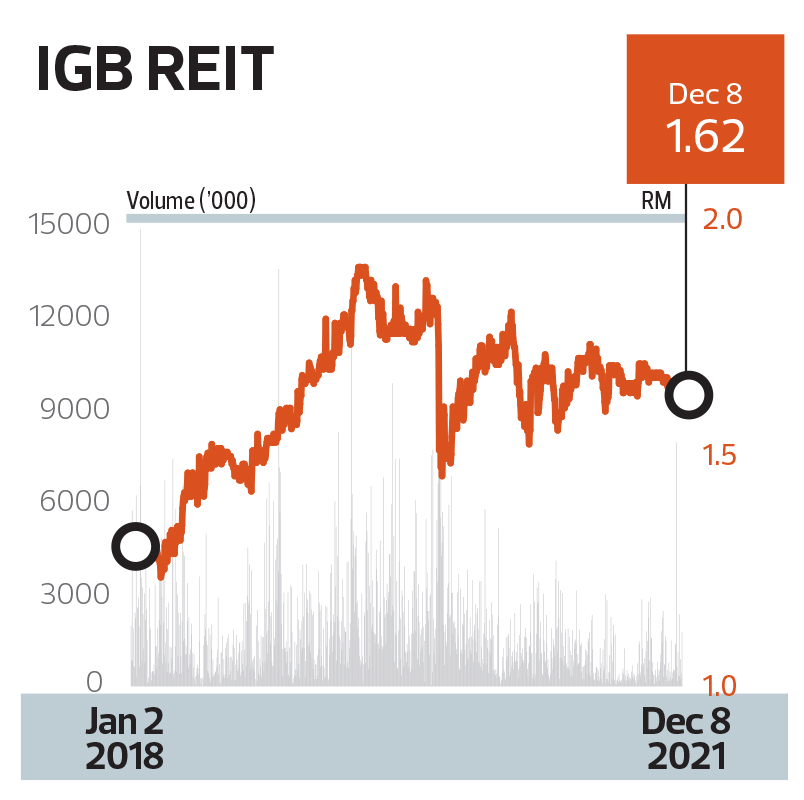

It retains an “add” rating on IGB REIT, with a target price of RM1.88. The rating is supported by the group’s FY2021 to FY2023 dividend yields of 3.7% to 5.3%.

“We believe IGB REIT’s flagship malls’ strong neighbourhood appeal is well-positioned to benefit from the turnaround in retail mall sentiment and a recovery in retail sales, which is its key medium-term potential share price catalyst,” it says.

The downside risks, however, are weak tenancy renewals, a prolonged negative rental reversion and resurgence of Covid-19 infections that result in movement restrictions.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.