The wealth gaps between the baby boomers, Generation X and the millennials have always been a source of contention. While the oldest cohort has been vaunted for being financially savvy, the younger groups are often reproached for their spending on luxuries such as avocado toast and speciality coffee and not enough on housing and retirement.

The baby boomers — the wealthiest generation in history — are referred to as such following the baby boom after World War II. Having grown up at a time when much of the world was recuperating from the aftermath of war, the baby boomers were motivated to accumulate wealth and strive for financial stability.

In many ways, witnessing the stress and trauma of the various upheavals around the world left them with a deep-seated conviction, to some, almost an obligation, to accrue assets such as property and stocks, upon coming into adulthood.

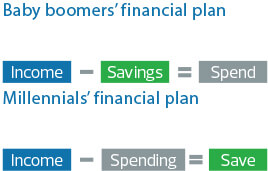

That translated into a disciplined savings behaviour where individuals would spend what was left of their incomes, after having saved a certain proportion for the proverbial rainy day.

The dynamics of the retail industry also influenced the saving and spending pattern of the baby boomers. The lack of choice or convenience available over the internet today meant that the baby boomers were less likely to spend impulsively and hence, they ended up saving a greater proportion of their income.

With baby boomers, the trend is also apparent in the kind of assets they invested in. They mostly viewed physical assets such as property as stable investments and the attractive rental yields and capital gains (back in the day) warranted that the savings were generally skewed towards property investments.

When it came to investing in financial assets such as stocks and mutual funds, access to information was limited, which explains why many chose to stay on the sidelines. When they did invest in financial assets, the baby boomers generally relied on their friends and family for advice, which, in most cases, lacked professional rigour.

The millennials were born and brought up in the age of comfort and convenience for the most part, where they have enjoyed a fairly cushioned upbringing. Save the recession of 2008-2009, they have not really endured the economic hardships that the previous generation had to endure and, hence, the urgency to save for a rainy day is not as strong.

They are also much more educated and have a strong desire for self-directed decision-making.

To add to this, the internet has taken over the retail industry and made spending a bit too convenient. Couple this with the age of instant gratification and absolute modern luxury and you see why millennials mostly struggle with their savings behaviour.

Where baby boomers spent what was left after saving, millennials find themselves saving what is left after spending (which is not much once they cave in to their impulses).

The advent of the internet and innumerable technological advancements has changed our lives so much, making a profound impact on our world view.

Fuelled by what has been described as the carpe diem (“seize the day” in Latin) instinct, their intentions are all about investing in experiences. To them, life is about creating memories and enjoying the journey, not working to save for retirement.

The downside of all of this is that they have much more difficulty when it comes to accumulating wealth. Balancing the urge to live in the moment and, at the same time, prepare for an indistinct future is a tough demand.

It is no surprise that millennials generally spend more than they save. Though still not spectacular, the financial track record of this generation is showing signs of promise.

A 2018 Standard Chartered report found that this generation of the emerging affluent are beginning to discover that proactively managing their money (save first, spend later) can help them save for their goals and a better future.

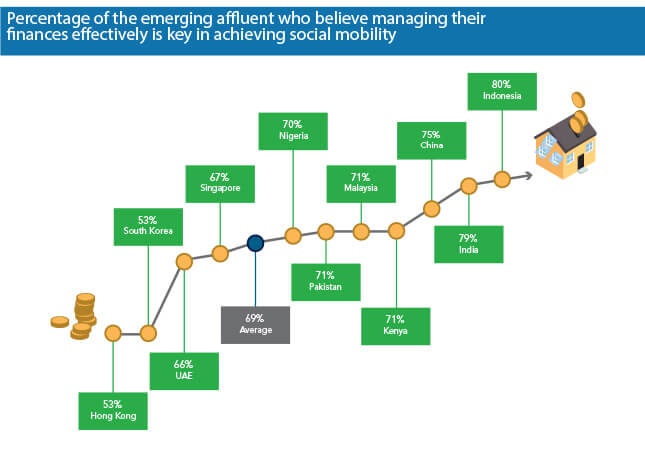

The Climbing the Prosperity Ladder: The Rise of the Socially Mobile in Asia, Africa and the Middle East survey states that emerging affluent know that smart financial choices will improve their social status, with more than two-thirds (69%) saying that managing their finances effectively holds the key to greater social mobility.

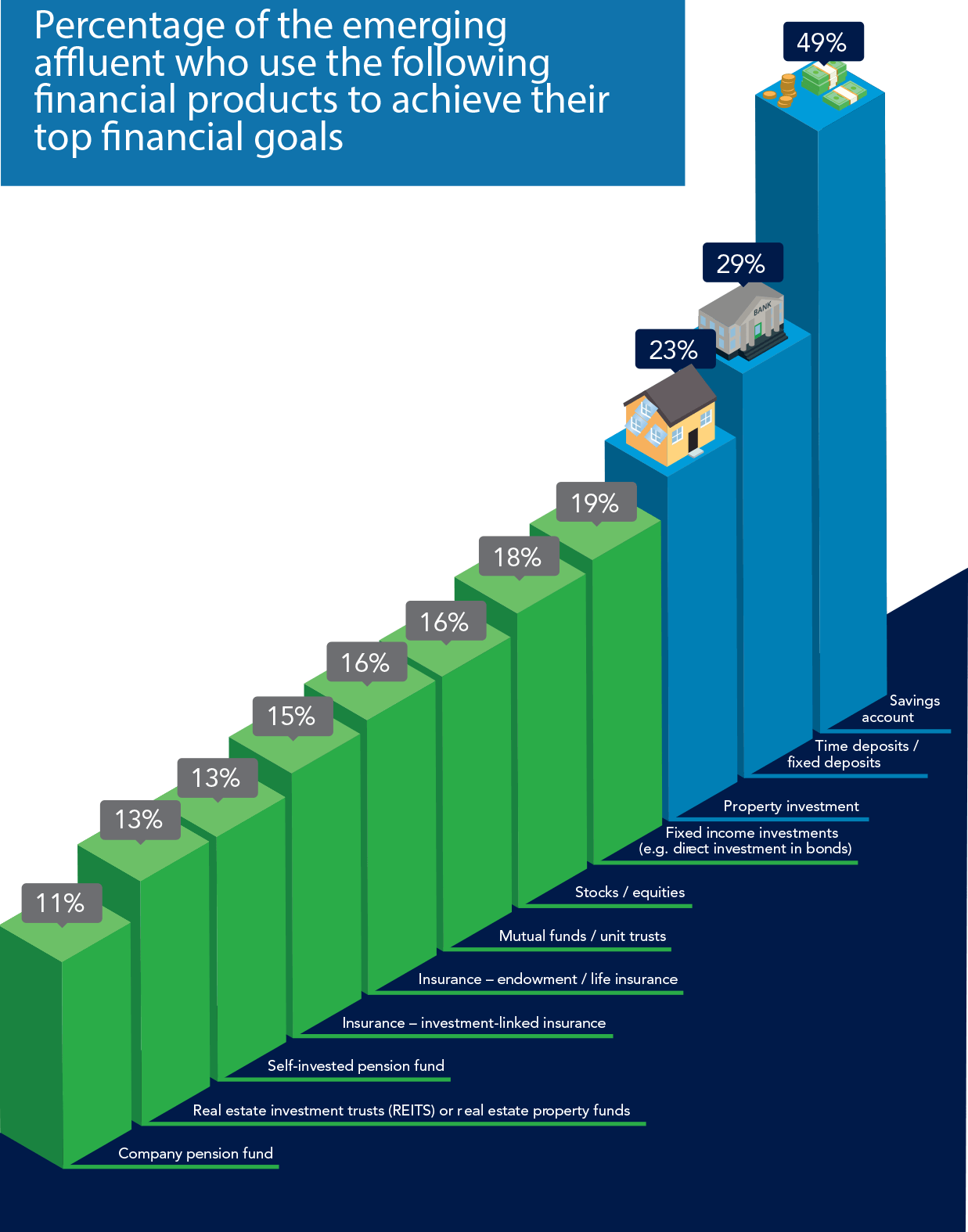

Interestingly, while the emerging affluent millennials increasingly acknowledge the need for discipline and sophistication in their financial plan, they continue to employ the most basic level of sophistication (basic savings account being the most prevailing financial product being used to achieve their goals).

A debilitating factor is information overload. With multiple wealth management outfits offering innumerable wealth products, it is increasingly difficult for self-directed investors to make decisions as an overdose of information feeds their paralysis.

This is where Standard Chartered SmartGoals comes in.

The millennial generation may not be prone to investing but they are pretty adept at setting and achieving their goals.

Click / Tap image to enlarge

Helping the emerging affluent to build their wealth

SmartGoals is designed to leverage on this attitude by making investing for life’s goals easy and effortless.

The platform intelligently understands the client’s risk tolerance and return preferences, offers a diversified portfolio of unit trust funds tailored to those preferences and is tied to client’s investment goals.

SmartGoals is embedded with the same advisory process that Standard Chartered employs to advise our high-net-worth clients. But it has been made extremely affordable for the mass affluent to take advantage of.

The platform is an amalgamation of Standard Chartered’s award-winning market insights and trusted advisory capabilities. It is now accessible to clients for as low as RM400 in initial investment (subsequent monthly investments are as low as RM200).

The first-of-its-kind platform is available through both the SC Mobile smartphone application and Standard Chartered online banking website.

To find out more about SmartGoals, visit sc.com/my/investments/smartgoals/. For more stories on investing for millennials, visit sc.com/my/stories/

Earn up to 6% p.a. on PrivilegeSaver with Standard Chartered Priority Banking.

Let’s chat. Leave your details here or call us at (03) 7718 9788 to learn more

- Sapura Energy bags multiple contracts worth nearly RM100 mil

- Anwar, Xi witness exchange of 31 MOUs and documents to advance Malaysia-China cooperation

- Bina Puri announces boardroom changes, founder director Tan Cheng Kiat retires

- King confident Malaysia, China will continue to empower cooperation

- Bank Rakyat flags challenging 2025, keeps 17% dividend for FY2024

- Putrajaya orders temporary closure of KL Tower, says past concessionaire's stay 'unlawful'

- Meta saw TikTok as ‘highly urgent’ threat, Zuckerberg says at antitrust trial

- Sapura Industrial, Gas Malaysia, CapitaLand, Hextar Technologies, Golden Land, Skyworld, Sapura Energy, Bina Puri, Paragon Globe, OCK Group, Nextgreen, Nexgram

- Ivory Properties aborts land disposal deal with Chin Hin following liquidation of subsidiary

- Tesla slumps below 50% share of California’s electric car market