This article first appeared in The Edge Financial Daily on January 13, 2020 - January 19, 2020

The start of 2020 was not an encouraging one for the local stock market. Though it closed above the psychological 1,600 level on the first day of trading at 1,602.5, it saw a sharp dip last Wednesday amid growing US-Iran tensions, and ended last Friday at 1,591.46. The general sentiment is definitely cautious, what more after the Malaysian stock exchange ended the previous year being one of the worst-performing bourses in Asia. That, too, was after a near 11% contraction in the local stock market in 2018. Still, there are opportunities to be found — whether they be battered-down stocks that are now at attractive valuations, steady dividend stocks, or potentially strong growth stocks. Here, The Edge Financial Daily has picked 10 stocks — categorised by theme based on one’s investment appetite — that it believes could provide good returns for the first half of the year (1H20).

Undervalued counters

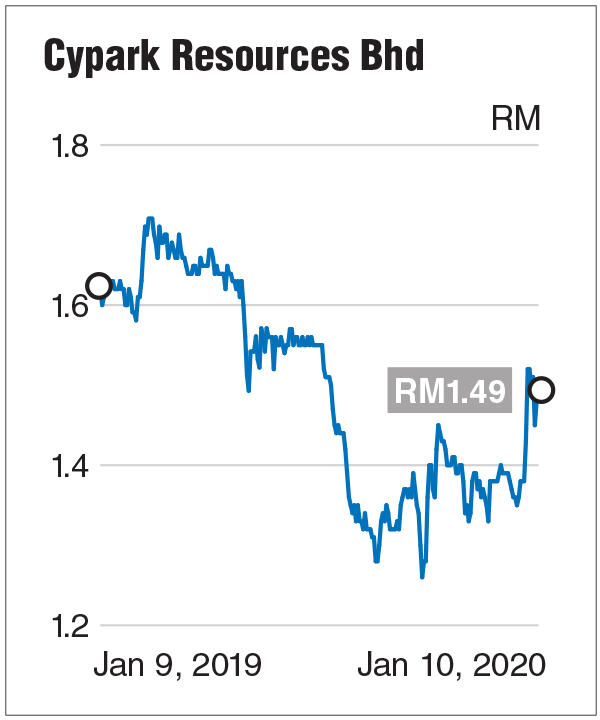

Cypark Resources Bhd

Renewable energy (RE) player Cypark Resources Bhd is among our top picks, given the industry’s bright prospects, led by Putrajaya’s target of having RE make up 25% of the country’s energy mix by 2025, from 2% currently.

Valuation-wise, Cypark has a price-earnings ratio (PER) of 7.2 times. In contrast, newly-listed Solarvest Holdings Bhd’s PER stands at 20.2 times. “We are not happy about this (valuation) because if you have a better track record in terms of earnings growth... that should be reflected,” Cypark group chief executive officer Datuk Daud Ahmad said last December, adding that the valuation “does not do justice” to the group’s earnings record.

Cypark’s share price performance has also not reflected the annual double-digit net profit growth it has recorded since the financial year ended Oct 31, 2012 (FY12) — except for FY15 — with steady revenue growth. The stock, which saw some uptrend in February last year to as high as RM1.71, declined about 12.87% to RM1.49 last Friday.

Phillip Capital Management Sdn Bhd chief investment officer Ang Kok Heng said Cypark’s share price has been affected by the delay in completing its Ladang Tanah Merah waste-to-energy plant, as well as its high gearing. As at end-October 2019, the group’s total borrowings stood at RM1.17 billion, of which RM184.87 million were short-term borrowings. Cash and bank balances were at RM523.65 million.

Daud, meanwhile, indicated that Cypark intends to restructure its loans in the next 12 months. It is also looking to potentially spin off its solar unit to unlock value and fund the group’s future growth.

Prospects-wise, besides the third phase of the Large Scale Solar (LSS) scheme, Ang said Cypark may get the job to install solar panels on government buildings in Negeri Sembilan and Kedah. Cypark, together with its consortium partner Impian Bumiria Sdn Bhd, announced in December that it had won a competitive bid to develop a 100mw LSS photovoltaic plant of alternating current in Marang, Terengganu.

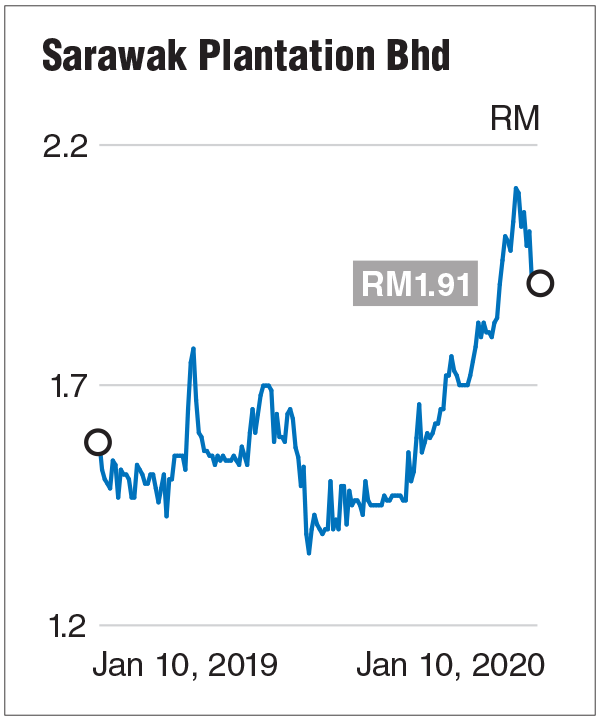

Sarawak Plantation Bhd

It can be difficult to pick the next big oil palm stock with a sector-wide recovery expected this year. But Sarawak Plantation Bhd, a pure upstream plantation firm trading mainly in spot prices, stands out as a potential big winner that will benefit from the current crude palm oil (CPO) price uptrend, amid a timely production growth.

The group, with a total harvestable area of 17,240ha, is set to enjoy a bumper harvest in the coming months, according to PublicInvest Research analyst Chong Hoe Leong. Chong said the Sarawak-based company’s stronger fresh fruit bunch growth will mainly come from the central region, which saw a 39% growth last year while the northern region posted a smaller growth of 11%.

“Sarawak Plantation mainly trades in spot price. As such, it will benefit from the capture on spot prices as they will manage to enjoy the stronger CPO prices at current levels compared to those companies which are locked in at forward sales based on the lower CPO prices previously.

“Based on the sensitivity analysis, for every RM100/ tonne increase in CPO price, the company’s bottom line is expected to expand by about RM7 million or a massive growth of 40%, given the low-base effect,” Chong said when contacted.

Chong has an “outperform” call on the stock with a target price of RM2.80 based on a 20 times financial year ending Dec 31, 2020 price-earnings ratio. The stock, which has gained 41.5% from its 10-year low of RM1.35 last July to now trades at RM1.91, currently fetching a forward PER of 39.7 times.

Besides a strong projected earnings growth, Chong said Sarawak Plantation has a solid balance sheet and an experienced management team under the leadership of Ta Ann Holdings Bhd, its largest shareholder since January 2018.

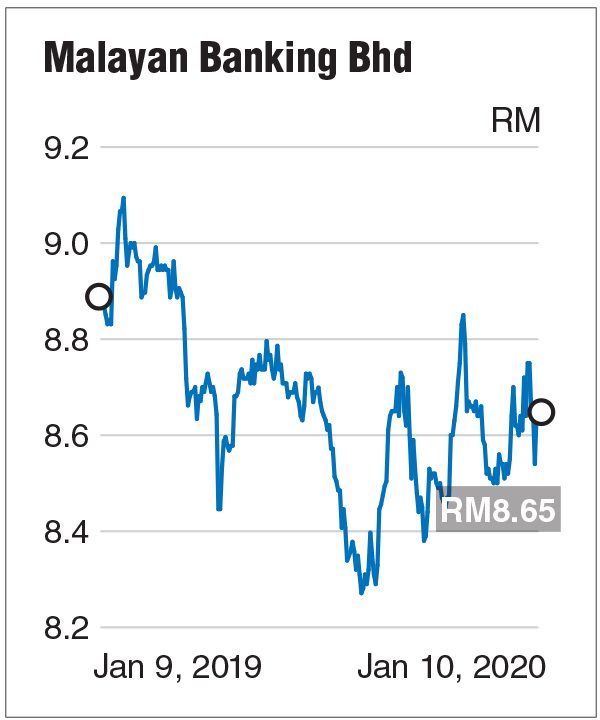

Malayan Banking Bhd

Malayan Banking Bhd (Maybank), the only FBM KLCI component stock in our top picks, is Malaysia’s largest bank in terms of market capitalisation. Notwithstanding this, its price-to-book value (P/BV) is at 1.23 times, significantly lower compared with Public Bank Bhd’s 1.78 times and Hong Leong Bank Bhd’s 1.38 times. The bank’s P/BV is also cheaper now compared against its five-year average P/BV of 1.4 times.

Over the past one year, Maybank’s stock has declined 2.48% to close at RM8.65 last Friday. Most banks’ share prices have been on a declining trend amid the lacklustre earnings growth following a cut in the overnight policy rate (OPR) in May 2019. At its current share price, the bank has a market capitalisation of RM97.24 billion. The once RM100 billion market cap counter was hovering below RM9 throughout 2019.

Notably, some 74.59% of its shares are held by institutional funds, while its 6.59% dividend yield is the highest among its peers. Of the 21 research houses covering Maybank, it has 10 “buy” calls, 10 “hold”, and one “sell”, with a consensus target price of RM9.27. This indicates a potential 7.17% headroom for the stock.

MIDF Research, in a recent thematic report, kept its positive stance on the banking sector despite expecting another OPR cut in the first quarter of 2020. It sees the key rate cut having a muted impact on the banks’ overall earnings this year, due to a possible demand-boost to loan growth.

“Based on the ability of banks in general to navigate the headwinds they faced last year, we opine that banking stocks are undeservedly undervalued currently... our top picks for this sector will be banks with scale and size or the potential to maintain its earnings momentum,” said MIDF, naming Maybank as one of its top picks.

MIDF also expects the net interest margin compression to be manageable in 2020, as it believes banks will fight less aggressively for deposits as their net stable funding ratio requirement has been met.

Growth stocks

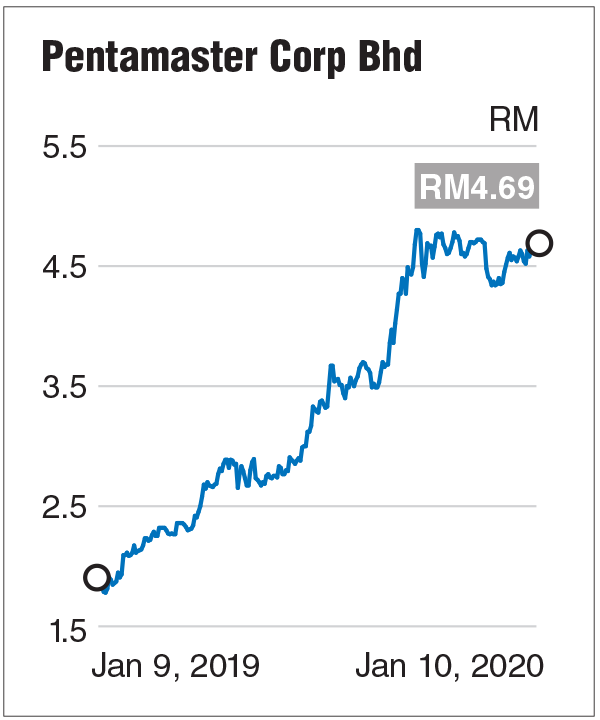

Pentamaster Corp Bhd

Pentamaster Corp Bhd, one of the best performing technology counters last year in terms of share price performance and earnings, continues to be our top pick for the first half of 2020, as its prospects remain optimistic.

Besides 5G network deployment being a key catalyst for its industry this year, the automated test equipment manufacturer is expected to see more business from China’s semiconductor players due to trade diversion amid the protracted China-US trade war.

Although Pentamaster did not pay any dividend, its share price has jumped 151% in the past 12 months to close at RM4.69 last Friday. Notably, the company is one of CGS-CIMB Research’s top three picks, according to the research house’s latest strategy note titled “Navigating Malaysia”.

CGS-CIMB Research expects Pentamaster to deliver a 27% earnings per share compound annual growth rate for the financial year ended Dec 31, 2018 (FY18) to FY21, driven by expansion in the automotive and medical device segments as well as potential new customer wins in North Asia.

Higher sales contributions from the automotive and medical segments will provide better earnings stability due to long-term demand visibility and higher margin portfolio, said its analyst Mohd Shanaz Noor Azam. “Rising penetration of 3D sensing in smartphones, new customer wins in China, potential re-inclusion in the Securities Commission Malaysia’s (SC) syariah-compliant list and a weaker ringgit versus the US dollar are potential rerating catalysts for the stock,” Mohd Shanaz said. He also noted that the recent pullback in Pentamaster’s share price due to its exclusion from the SC’s syariah-complaint list provides as a good opportunity for investors to accumulate the stock, as the exclusion does not alter the company’s fundamentals and growth prospects.

“The long-term uptrend for Pentamaster is likely to continue in 2020 as its higher high and higher low sequence since the 2013 low is intact,” said Mohd Shanaz, adding that the stock is likely to work its way to new highs in the months to come. “As long as prices stay above the RM3.50 (uptrend channel support), look for a test of the RM6.00-6.20 levels next,” he noted.

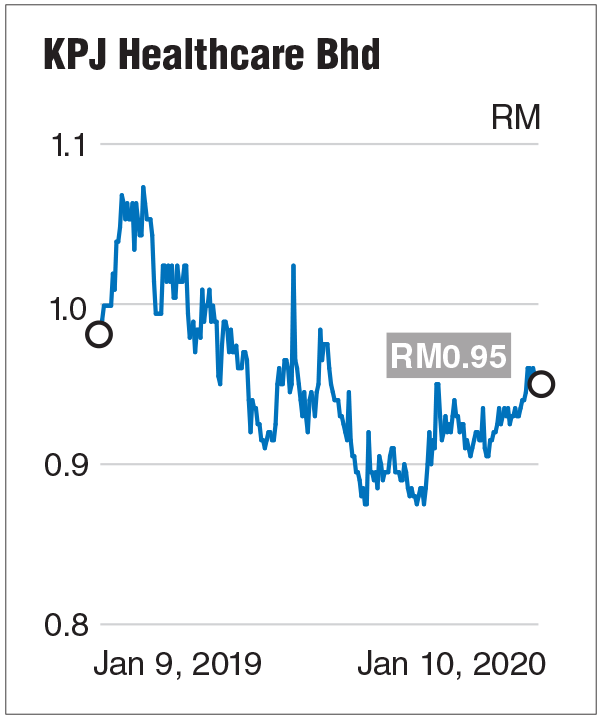

KPJ Healthcare Bhd

This year is not just Visit Malaysia Year, but also Malaysia’s Year of Healthcare Travel. More than RM2 billion worth of receipts could be generated from Malaysian hospitals this year — up 33% from 2018’s RM1.5 billion — as the country promotes itself as a regional healthcare destination, according to the Malaysia Healthcare Travel Council.

Malaysia’s ageing population and rising household income have also led to increased domestic demand for healthcare, which will make it more difficult for the country’s public healthcare system to cope, noted Cheah King Yoong of AllianceDBS Research. This, he said, will continue to drive more affluent patients to private hospitals. KPJ Healthcare Bhd, which operates 26 specialist hospitals, has seen uninterrupted growth in its annual inpatient admissions in Malaysia. MIDF Research estimates the number to hit 320.5 million in 2020, from 299.8 million in 2018.

Together with a prudent cost management, the private hospital operator, whose market capitalisation stood at RM4.06 billion, is expected to continue to deliver healthy earnings and improved margins this year.

CGS-CIMB Research said the private healthcare player’s cumulative nine-month earnings — its net profit for the period ended Sept 30, 2019 stood at RM127.37 million, with a revenue of RM2.62 billion — benefitted from strong patient visitations and higher revenue intensity for its Malaysian operations.

“We expect KPJ Healthcare to continue to benefit from stronger patient traffic on the back of the ramp-up of its hospitals, which are currently in the growth phase (less than 10 years old), as well as from an improvement in healthcare demand.

“KPJ Healthcare is also exploring capex (capital expenditure)-light opportunities, including shifting its focus to brownfield expansion, after the existing greenfield developments are rolled out. We believe this shift in strategy is positive as it will reduce the need to fund heavy development expenditure, which should help KPJ manage its borrowings,” it added.

CGS-CIMB is among 13 research houses which rated KPJ Healthcare a “buy”, with a consensus target price of RM1.13, Bloomberg data shows. Based on the stock’s last closing price of 95 sen on Jan 10, this means a potential 19% upside.

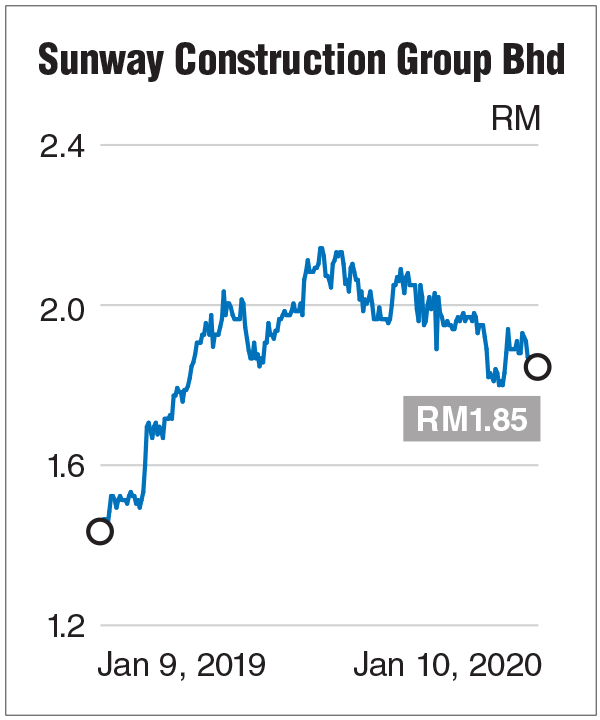

Sunway Construction Group Bhd

Sunway Construction Group Bhd (SunCon) is among our top picks given the anticipated pickup in construction activities this year, driven by the continuation of mega infrastructure projects.

The stock, which has a relatively attractive dividend yield of 3.78%, climbed 27.95% over the past 12 months to close at RM1.85 last Friday, bringing its market capitalisation to RM2.39 billion. Of the 13 research houses covering the stock, four have it on “buy”, four “hold”, and three “sell”.

SunCon is also among Hong Leong Investment Bank (HLIB) Research’s top picks for 2020, as the research house continues to like the stock due to its ample balance sheet capacity, positive earnings trajectory and strong support from parent company.

“We expect contract awards to pick up going forward due to recovery in development expenditure as the government rolls out major infrastructure projects,” said HLIB.

Into 2020, HLIB said the first of the year should be dominated by tender news flow on the East Coast Rail Link project (RM44 billion), Pan Borneo Highway Sabah project (RM12.3 billion) as well as packages three and five of the Central Spine Road.

Notably, development expenditure for 2020 is expected to increase 4.3% year-on-year to RM56 billion versus 2019’s 4.3% decline, as the government rolls out previously-delayed infrastructure projects, HLIB added.

High risk, high rewards?

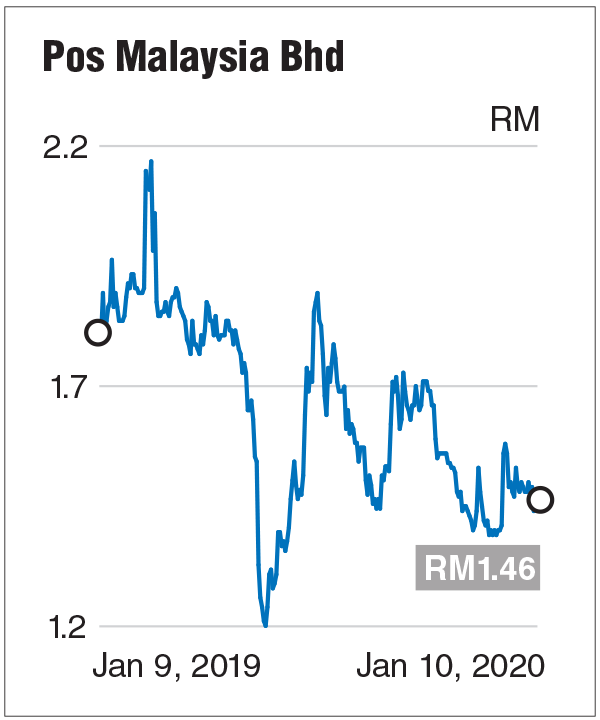

Pos Malaysia Bhd

Pos Malaysia Bhd is a stock worth watching as the national postal service provider has reportedly received a letter confirming the government’s approval for a tariff hike — the first in nearly a decade — which could offer a lending hand that pulls the company out of the doldrums. Citing two unidentified ministers, news portals have reported that the government has approved a proposal from the company to raise rates, its first revision in nearly a decade.

Pos Malaysia said it has yet to obtain from the government official details of the new postal tariff rates and the implementation date, although a source within the company was reported as saying that the letter has reached its hands.

The change in pricing would reportedly not impact postage rates for domestic non-commercial users.

While more needs to be done in the face of structural issues such as declining mail volume and high universal service obligation (USO) costs, the rumoured tariff hike could play a role in attempting to reverse Pos Malaysia’s fortunes, which posted a negative total return of 19.17% in the past year. The stock finished at RM1.46 last Friday, with a market capitalisation of RM1.14 billion.

Pos Malaysia recently reported its fifth consecutive quarterly net loss of RM29.34 million — higher than the RM16.58 million net loss posted a year earlier — bringing the company an accumulated loss of RM215.16 million since July 2018.

The latest loss incurred for the three months ended Sept 30, 2019, was due to the continued decline in its mail volume, besides increasing costs in serving the USO to accommodate the increasing growth of addresses nationwide.

Group CEO Syed Md Najib Syed Md Noor, who assumed the post in October 2018, told The Edge Malaysia weekly in an interview that Pos Malaysia’s turnaround plan will take three years before the company returns as a profitable and sustainable business by financial year 2022.

He added that dividends may continue to flow in the next three years to retain investor interest, depending on operating cash flow.

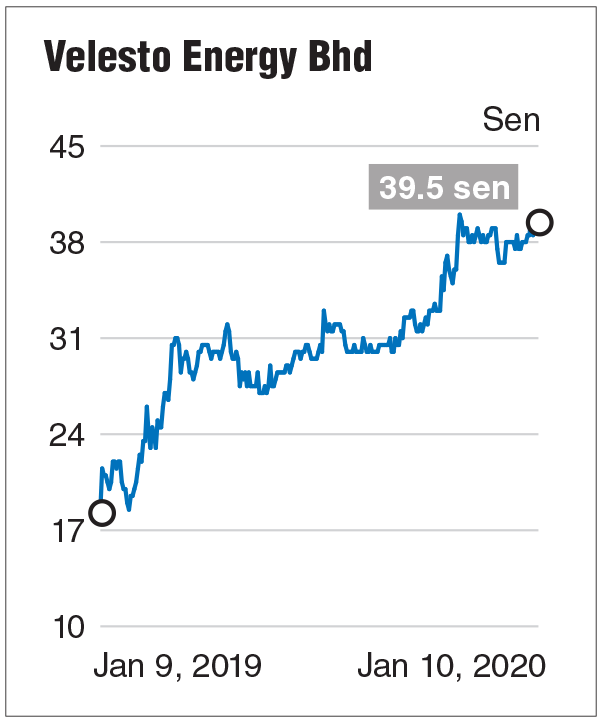

Velesto Energy Bhd

The oil and gas industry has enjoyed a stable year with the benchmark Brent crude oil price averaging at US$64.12 a barrel in 2019 — lower than US$71 in 2018 but higher than US$54 in 2017 and US$44 in 2016. Brent is expected to trade above the US$60 (RM244.60) level this year with further activity across the value chain.

The Petronas Activity Outlook report for 2019-2021 indicated that the national oil major required 16 to 18 jack-up rigs in Malaysian waters in 2019, and 17 to 19 in 2020 and 2021, a stark contrast to the fourth quarter of 2018 (4Q18) when nine or 10 jack-up rigs were deployed.

Jack-up rig player Velesto Energy Bhd, formerly known as UMW Oil & Gas Bhd, appears to be a proxy to the robust upstream exploration and production activities, which may help the company stage a turnaround it has been working towards.

Velesto posted a core net profit of RM26 million for the cumulative nine months ended Sept 30, 2019 (9MFY19), a dramatic turnaround from a RM16.7 million core net loss for the same period of FY18, on the back of an increased jack-up rig utilisation rate of 92% in 3Q19.

Although Velesto’s share price has risen about 83% to 39.5 sen over the course of a year — with a price-to-book value ratio of 1.14 times — it is well below earlier levels. The stock hit a high of RM4.31 in February 2014 to become one of the most loved counters.

Its market dominance means there could be an uptick in its rigs’ utilisation and daily charter rates (DCR) this year, since the only other player with jack-up rigs is Perisai Petroleum Teknologi Bhd.

“Market dynamics for jack-up rights in Malaysia look favourable going into FY20, with limited supply in the region and higher capex spending by Petronas. We have an ‘add’ call on Velesto as all seven of its jack-up rigs are working and due for repricing in FY20,” said CGS-CIMB Research analyst Raymond Yap. Yap, who has a target price of 47 sen on the stock, also noted that Velesto is expected to have fewer special survey days next year, and that the full employment for Velesto’s fleet of seven jack-up rights means that its FY20 earnings will be strong.

“Velesto delivered an average DCR of US$70,870/day in FY19F, based on our forecast, but we expect the FY20F DCR to rise 4.7% year-on-year to US$74,210/day as all seven jack-up rigs will see their commercial terms repriced in FY20F,” he added.

Defensive play

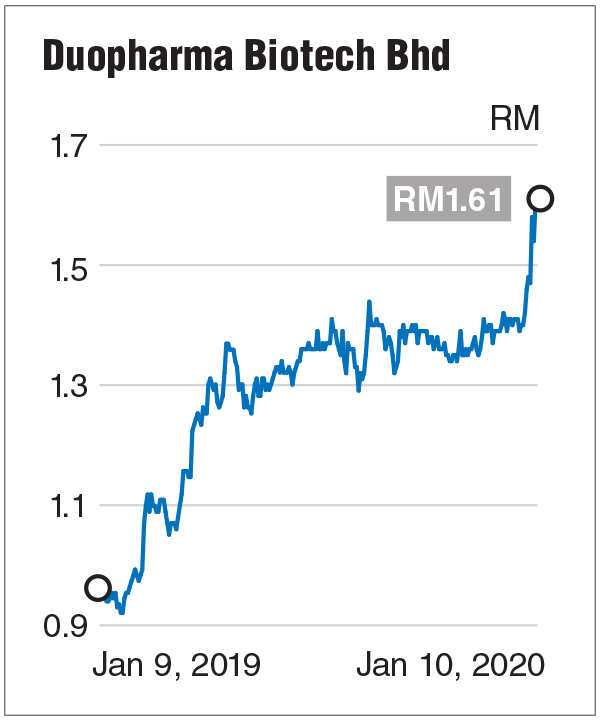

Duopharma Biotech Bhd

With Malaysians moving into an ageing population, healthcare is certainly one of the preferred defensive play sectors.

All five research houses covering pharmaceutical company Duopharma Biotech Bhd have “buy” calls with a consensus target price of RM1.80, representing a potential upside of 11.8%, from its closing price of RM1.61 last Friday. The counter has a one-year total return of some 67%.

Duopharma Biotech is expected to further solidify its market position given its ongoing expansion plans, new product launches and the 6.6% higher budget allocation of RM30.6 billion to the health ministry for 2020, TA Security Holdings Bhd analyst Tan Kong Jin said in the research house’s annual strategy report.

Tan said the company’s ability to win approximately RM170 million worth of contracts from the government recently attested to that.

The company also recently received extensions of its approved product purchase list (around RM80 million) and insulin contract (RM91.1 million), which means 30% of its 2020 sales would be recurring, said Tan.

He also noted that the company is a market leader in terms of sales volume and second in terms of value.

In an interview with The Edge Malaysia weekly in October, Duopharma Biotech’s group managing director Leonard Ariff Abdul Shatar said the company could not expand production capacity fast enough to keep up with the market.

This could mean that there are tonnes of opportunities, especially in the healthcare market.

To date, the company has five new effervescent products ready to go since two years ago — on top of two already in the market — but not the manufacturing capacity to spare to actually make them, said Leonard.

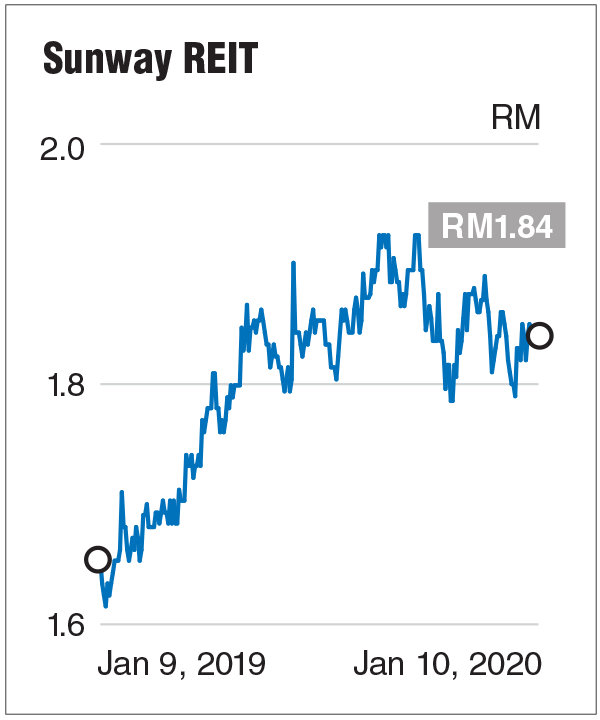

Sunway Real Estate Investment Trust

Real estate investment trusts (REITs) are often considered defensive stocks and Sunway REIT appears to be a good addition to one’s strategy portfolio in 2020. This is especially as Sunway REIT’s management is targeting to grow its property value to between RM13 billion and RM15 billion by the financial year ending June 30, 2025 (FY25), from RM8 billion at end-FY19, and diversify its asset base by increasing allocation for service and industrial assets.

“Broadly, we like the management’s plan so long as acquisitions are earnings-accretive. A diversified asset base should lower earnings risks, while a larger market capitalisation should increase the REIT’s liquidity [if acquisitions are partly funded by equity].

“While the management has yet to share its acquisition targets, we believe the asset pipelines of its sponsor (comprising retail, office, education and medical assets) are good candidates for future acquisitions,” wrote Affin Hwang Capital in a note.

The research house said despite lowering FY20 to FY22 earnings per unit forecasts due to soft property market conditions, it is still expecting Sunway REIT to report higher earnings for FY20, up by 3.4% y-o-y, driven by contributions from Sunway University, a strong performance of Sunway Pyramid, and a recovery in revenue from Sunway Resort Hotel & Spa coming from a low base.

MIDF Research too said it continues to prefer Sunway REIT among the REITs it covers for its stable income growth from Sunway Pyramid shopping mall and a balanced asset portfolio. The research firm’s “buy” call on Sunway REIT is assigned with a target price of RM2.02, versus the consensus RM1.98 across 15 brokers. The stock closed at RM1.84 last Friday, generating a total return of 12.61% over the past one year.

For FY19, Sunway REIT delivered a distribution per unit of 9.59 sen, versus 9.57 sen for FY18. Distribution yield compressed from 5.4% to 5.1% on the back of appreciation in unit price.

During the year, Sunway REIT posted a 4.7% growth in net property income (NPI) to RM439.7 million, while net realised income was up marginally by 0.1% to RM282.34 million. Revenue rose 3.5% to RM580.3 million.

For 1QFY20, the trust saw its NPI grow 7.7% to RM119.07 million, from RM110.51 million a year earlier, as revenue expanded 8.1% to RM155.35 million from RM143.74 million.