This article first appeared in The Edge Malaysia Weekly on July 25, 2022 - July 31, 2022

A country’s ability to borrow cannot be determined solely by the headline debt to gross domestic product (GDP) figure; it also needs to take into account more pertinent factors like debt affordability as well as debt sustainability, Finance Minister Tengku Datuk Seri Zafrul Abdul Aziz rightly said in parliament last week, in reply to a question by the Member of Parliament for Pontian, Datuk Seri Ahmad Maslan.

The former deputy finance minister had asked two questions that have gone viral on social media of late — whether Malaysia is at risk of going bankrupt like Sri Lanka, and why Malaysia doesn’t just continue to borrow more money to help the people if the country’s debt is indeed at manageable levels and it still has headroom to borrow.

Citing prevailing economic indicators, Zafrul told parliament that the chances of Malaysia going bankrupt are very slim. Not only has the International Monetary Fund (IMF) never raised bankruptcy issues, Zafrul said the fund also expects Malaysia’s economy to grow 5.75% in 2022. That is above the IMF’s 3.6% forecast for the global economy and 5.4% forecast for emerging and developing Asia in April (which IMF says may soon be revised lower).

Still, Zafrul rightly added that Malaysia needs to be prudent on finances and rein in debt according to what the country can realistically afford.

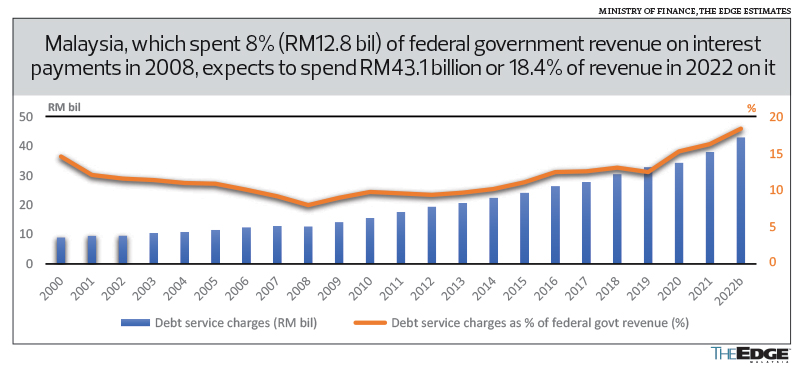

While Malaysia’s gross debt to GDP level of 63% may seem low relative to Japan’s 263% and Singapore’s 133%, Zafrul noted that Malaysia’s debt service ratio to revenue had reached 16.3% in 2021 and was already expected to breach 18% when Budget 2022 was tabled (with only 40% or RM31 billion of this year’s outsized RM77.7 billion subsidy bill budgeted for).

Put another way, close to 20 sen of every ringgit that Malaysia earns is going to cover only interest payments on direct federal government debt, which had reached RM1.02 trillion as at end-April. The debt service ratio is expected to remain near one-fifth of revenue in Budget 2023, The Edge’s back-of-the-envelope calculations show, barring a substantial rise in revenue or sizeable reduction in debt and/or cost of debt — which is possibly why Zafrul had added that Malaysia’s tax revenue to GDP of about 11% is low relative to the Philippines’ 18%, Thailand’s 17.2%, Singapore’s 13.3% as well as the 33% average for members of the Organisation for Economic Co-operation and Development (OECD), which are mostly developed high-income nations.

Why it’s different for Singapore and Japan

Japan may have the world’s highest headline gross debt to GDP of 263.1% in 2021, but net debt to GDP is much lower at 169% of GDP, according to IMF data. Japan — whose net external assets were at a record ¥411 trillion (US$3.24 trillion) in 2021 — has also been the world’s top creditor nation for 31 straight years.

While there are debates on whether the yen is still a safe-haven asset as the gap in monetary policy widens with quantitative tightening, and as the currency tumbled to a 20-year low versus the greenback, the chances of a sovereign default are still deemed low because Japan borrows entirely in yen and mostly (87%) from residents — the Bank of Japan holds close to half of debt paper issued by the Japanese government.

And even though proponents of Modern Monetary Theory may cite Japan as an example of how debt levels can be higher than traditionally thought, most experts would not advocate others going down the same path of having the central bank plug sizeable fiscal gaps. This is true even for the US, whose dollar is a reserve currency for the world. Debt, after all, needs to be repaid one way or another at some point — there is a cost to the people and the economy even if the central bank were to allow the government to not pay its dues.

Moreover, the ringgit — and Malaysia — are not in the same league.

Singapore — one of only 11 countries in the world with the coveted AAA sovereign rating — is also in a league of its own. For starters, it does not have any net government debt. This is because there are laws that prevent its government from spending more than what it earns annually unless there are extraordinary circumstances, such as the Covid-19 pandemic. The prudence in financial management has allowed the accumulation of sizeable reserves, on top of what is reported by its central bank, which uses currency strength to hedge against inflation.

The little debt service charges (less than 0.5% of revenue in 2020) Singapore incurs are more than made up for by its investment returns, which make up around one-fifth of its government’s annual income, giving the city state flexibility to remain a low-tax regime.

Singapore’s seemingly high headline (gross) debt to GDP ratio is also not debt taken to fund general government operations but to facilitate investment needs. Much of its gross external debt reflects foreign capital inflows and deposits into its banking sector.

Also, despite using up a substantial amount of reserves to defend its currency strength year to date, the Monetary Authority of Singapore’s official reserve assets stood at US$345.3 billion as at May 2022, down from US$417.9 billion as at end-2021 and US$362.3 billion as at end-2020 but above US$279.45 billion as at end-2019, according to Bloomberg data.

Sri Lanka’s debt service ratio

Data on Malaysia’s net debt to GDP is not available on the IMF or World Bank’s public databases.

We know that Bank Negara Malaysia’s foreign reserves stood at US$107 billion as at July 15 this year — down about US$9.9 billion from end-2021 and down US$5.8 billion from end-May 2022 — but are still 1.1 times short-term external debt and sufficient to finance 5.7 months of imports of goods and services.

That’s not to say that Malaysia can continue to borrow as much as it wants as there are already warning bells that it needs to be more prudent about borrowings.

Malaysia’s ratio of debt service charges to revenue of 15.3% in 2020 places it among the top 25 countries in the world ranked in terms of high interest charges to revenue, according to data from the World Bank.

Topping the list is Sri Lanka, which saw 71.4% of its revenue going to interest payments on debt in 2020. In April this year, Sri Lanka said it would stop repaying international debt to conserve dwindling foreign currency reserves and, for the first time in its history, defaulted on its debt on May 19 after the expiry of a 30-day grace period for missed interest payments totalling US$78 million to foreign creditors of its sovereign bonds. The country only had US$25 million in usable foreign reserves when it suspended repayment of about US$7 billion in international loans due this year out of US$51 billion in foreign debt.

Others on the top 25 list of countries ranked by the percentage of revenue going to servicing interest payments alone in 2020 are Ghana (44.6%), Zambia (38.8%), Kenya (24.1%), Jamaica (22.4%), Brazil (21.7%), Dominican Republic (21.6%), Bangladesh (21.1%), Lebanon (21%), Malawi (20.7%), Indonesia (19.1%), Costa Rica (19.1%), Papua New Guinea (17.9%), Jordan (17.7%), Ecuador (17%), the Bahamas (16.5%), Fiji (16.3%), Mexico (15.4%), Guatemala (15.4%), Uganda (15.3%), Malaysia (15.3%), South Africa (15.2%), US (14.4%), the Philippines (13.3%), Namibia (13.1%) and Iceland (12.3%). (See table.)

Apart from Canada’s 5.6% and Australia’s 3.5%, it is perhaps no surprise that other countries with AAA sovereign ratings like Singapore spend less than 2% of government revenue on interest payment to service debt.

Improving debt affordability

With Malaysia’s debt service charges currently projected at 18% of revenue, there is a risk that the country could move higher on this list if revenue does not grow faster than its debt service charges, to bring down interest payments on its debt as a percentage of revenue.

The country’s past introduction of the goods and services tax showed that there could be at least a RM10 billion rise in revenue a year versus the current expanded sales and services tax — substantial given that debt service charges were RM34.5 billion in 2020 (15.3% of government revenue) and RM38.1 billion in 2021 (16.3% of government revenue).

Debt service charges were pencilled in at RM43.1 billion in 2022 and could reach RM46 billion in 2023, our back-of-the-envelope calculations show.

That level of interest payments means that the government needs revenue to be RM306 billion for the debt service ratio to fall back to 15%, a threshold breached in 2020. This would be a tall order even with the reintroduction of a broader consumption tax, given that federal government revenue reached an all-time high of RM264.4 billion in 2019, bolstered by a RM30 billion special dividend from Petroliam Nasional Bhd (Petronas) to pay owed taxes.

Revenue was pencilled in at RM234 billion in Budget 2022, an improvement from RM233.75 billion in 2021, but likely needs to be higher due to the outsized subsidies bill that Zafrul said could reach RM80 billion this year.

To be sure, Malaysia has never defaulted on its loan obligations, Zafrul reminded in his July 14 statement to correct misleading comments on the country’s debt and financial position that were appearing on social media. He also noted that Malaysia’s offshore borrowings were capped at RM35 billion and stood at only RM29.4 billion as at end-June.

Malaysia’s statutory debt, capped at 65% of GDP, stood at 60.4% of GDP as at end-June 2022, he said in the July 14 statement without disclosing the absolute amount. This is an increase from 58.5% of GDP (RM958.5 billion) as at end-April when direct federal government debt stood at RM1.078 trillion or 62% of GDP, according to the pre-budget statement.

While Malaysia is not in danger of defaulting on its loans like Sri Lanka, there is clearly a need to improve its debt affordability and reduce the proportion of revenue spent on debt servicing so that more money can go to more productive use, including supporting economic and human development. As debt needs to be repaid, Malaysia must learn to spend within its means and save for a rainy day. No amount of revenue would be enough to satisfy unbridled spending.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.