This article first appeared in The Edge Malaysia Weekly on May 30, 2022 - June 5, 2022

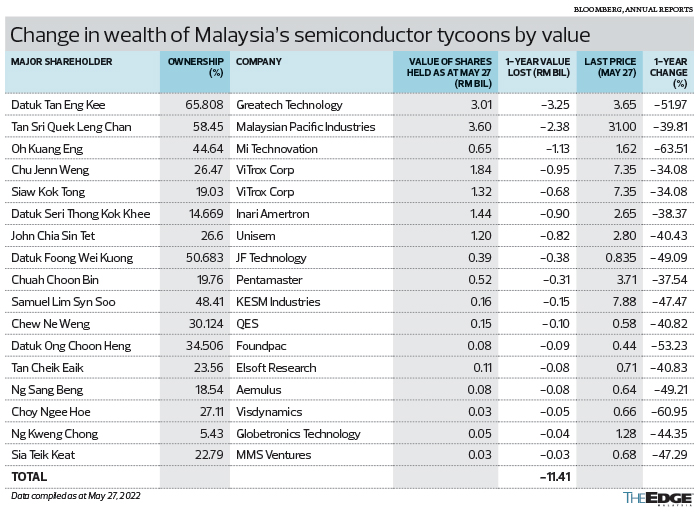

MALAYSIA’s semiconductor tycoons have collectively lost RM11.41 billion of their net wealth after share prices tumbled from 52-week peaks during the recent tech stock rout. While some were billions of ringgit poorer, others experienced losses that ran into the tens of millions.

Perhaps more concerning to these moguls and other investors are projections that there could still be further downside given the global inflation and supply chain disruptions.

Greatech Technology Bhd CEO Datuk Tan Eng Kee suffered the greatest paper loss — a whopping RM3.25 billion, when the company’s share price plunged 51.97% after climbing to a 52-week high of RM7.60. He owns 65.81% of the designer, manufacturer and integrator of factory automation solutions.

He is followed by Tan Sri Quek Leng Chan, who saw RM2.38 billion of his net wealth dissipate when the share price of Malaysian Pacific Industries Bhd, which he controls, tumbled 39.81% from a 52-week high of RM51.50.

Vitrox Corp Bhd president and CEO Chu Jenn Weng and group executive vice-president Siaw Kok Tong, who collectively own 45.5% of the company, saw a paper loss of RM1.63 billion when the stock fell 34.08% from a 52-week high. Chu and Siaw co-founded the homegrown automated test equipment (ATE) maker that was named The Edge Billion Ringgit Club (BRC) Company of the Year in 2021.

Mi Technovation Bhd group CEO Oh Kuang Eng suffered a paper loss of RM1.13 billion when his company’s share price tumbled 63.51%. He holds a 44.64% stake in the semiconductor equipment and semiconductor material specialist.

The 38.37% decline in Inari Amertron Bhd’s share price has cost Datuk Seri Thong Kok Khee an estimated RM900 million. He is a non-independent, non-executive director and 14.67% shareholder of the tailored electronics manufacturing services (EMS) contract manufacturing service provider.

Unisem Bhd chairman John Chia Sin Tet took an RM820 million hit when the company’s share price fell 40.43% from a one-year high. He owns 26.6% of the global provider of semiconductor assembly and test services.

The tech selldown also shaved RM380 million from the net worth of Datuk Foong Wei Kuong when JF Technology Bhd’s share price tumbled 49.09% from a 52-week high of RM1.64. He is managing director of the homegrown high-performance test contacting solution provider, which he co-founded with his wife Datin Wang Mei Ling.

At No 8 on the list is Chuah Choon Bin, chairman and 19.76% shareholder of automation solutions and services provider Pentamaster Corp Bhd. He had an estimated paper loss of RM310 million when the stock fell 37.54% from a 52-week high.

KESM Industries Bhd executive chairman and CEO Samuel Lim Syn Soo and Foundpac Group Bhd boss Datuk Ong Choon Heng were not spared from the tech rout. Lim saw a paper loss of RM150 million when the stock fell 47.47%. He owns 48.41% of the country’s largest independent burn-in and test service provider.

Ong, who has 34.51% equity interest in Foundpac Group, was hit with a paper loss of RM90 million when the stock tumbled 53.23% from a 52-week peak.

Chew Ne Weng, who holds a 30.12% stake in ATE maker QES Group Bhd, was poorer by RM100 million when the counter slid 40.82%. He is the founder, managing director and president of the group.

Aemulus Holdings Bhd CEO Ng Sang Beng lost RM80 million of his net worth after the company’s share price nosedived 49.21%. Also RM80 million poorer was Elsoft Research Bhd CEO Tan Cheik Eaik. Visdynamics Holdings Bhd CEO Choy Ngee Hoe, who holds a 27.11% stake in the company, saw a paper loss of about RM50 million.

Globetronics Technology Bhd founder Ng Kweng Chong saw RM40 million dissipate from his net worth after the stock tumbled 44.35%. He has 5.43% equity interest in the outsourced semiconductor assembly and test (OSAT) company.

Meanwhile, MMS Ventures Bhd CEO Sia Teik Keat, who has a 22.79% stake in the company, is RM30 million poorer.

Worries about stretched valuations, interest rate hikes, soaring inflation and supply chain disruptions have taken a toll on tech stocks and battered Bursa Malaysia’s Technology Index, which had contracted by nearly a third, or 31.83%, year to date to 66.45 points on May 27, from 97.47 points.

Some experts argue that the semiconductor sector is now oversold. But the odds may be stacked against them. The weakness in the sector is primarily a derating in valuations as central banks around the world tighten monetary policy, on top of the temporary disruptions in supply.

Given the strong capital gains over the past few years, investors may have been conditioned to shorter time frames, AIMAN Asset Management portfolio manager Lee Pak Seng observes.

“It will be nearly impossible to call the bottom of the derating cycle. But in the short term, it looks like there could be more downside since headwinds like rising interest rates and inflation, which is leading to higher input costs, have not fully abated yet.

“We are staying defensive and have reduced our exposure while maintaining positions in some of our high-conviction stocks in the sector. We will look to capitalise on opportunities when the risk-reward environment becomes more favourable.”

TA Investment Management chief investment officer Choo Swee Kee says the research firm is currently neutral on the sector while waiting for the bad news in the market to run its course.

“In the short term, we believe it would be prudent to tone down the growth expectation of tech companies as the supply chain disruptions are more serious and may last longer than expected. Rising costs and prices would also affect consumer demand as affordability becomes an issue,” he adds.

Choo says the once high-flying semiconductor stocks are going through a cyclical correction due to high valuations, which suggests that the optimism may have been overdone.

“Average price-earnings (PE) valuations of tech stocks reach highs of 40 to 60 times versus the historical average of between 15 and 25 times. Liquidity from the various global quantitative easing programmes was a major factor in supporting such high PE valuations,” he notes.

Given the downside risks to the local semiconductor sector, Choo suggests that investors pace out their buying in a few tranches and only be more aggressive when valuations are back to more acceptable historical averages of about 20 times forward earnings.

While industry earnings normalisation could be in the interim in view of growth moderation and supply chain disruptions, UOB Kay Hian Securities (M) Sdn Bhd senior analyst and head of retail research Desmond Chong sees bright spots from bottom-up stock picking of battered technology counters as he is positive on the long-term growth prospects of the semiconductor sector, as well as the value emerging given the current share price weakness.

Chong believes there is still room for growth amid the twin supply-demand shock and supply chain reconfiguration resulting from the US-China trade diversion. “Mean reversions were seen in the SPE (semiconductor production equipment segment) and OSATs’ forward valuation, from +2SD (standard deviation) above five-year mean during the peak in 2020/21, to now -0.5SD below its five-year mean, which we think makes the risk-reward profile better,” he says.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.