This article first appeared in Capital, The Edge Malaysia Weekly on December 19, 2022 - December 25, 2022

AFTER more than two years of exceptionally high freight rates in a tight capacity market, shippers are finally getting some relief. In the latter half of the year, shipping rates for both dry bulk carriers and container ships have come off the highest levels triggered when the Covid-19 pandemic disrupted the supply chain, causing port congestion, shortage of shipping containers and increased blank sailings by carriers.

Heading into 2023, shipping players and analysts are expecting global freight rates to fall further due to the greater availability of freight capacity globally and weaker freight volumes as the global economy deteriorates.

According to Tasco Bhd deputy group CEO Tan Kim Yong, container rates for certain routes have come down by more than 80% from their pandemic peak. For example, rates to ship a 40ft container from Asia to the US West Coast were as high as US$40,000 (RM176,000), but now they are closer to US$6,000.

“The rates are still 50% higher than the 2019 level of about US$4,000 per FEU (40-foot equivalent unit),” he tells The Edge. “People say rates are normalising. However, it depends on the trade lanes. For example, freight costs from here to Australia are now more expensive than to the US West Coast.

“There is a reason for this. Big US retailers like Target and Walmart that overstocked during the pandemic due to the uncertainty in shipping, are working through an unexpected glut of inventory. The surge in inventories has resulted in the current excess supply of goods. With a recession on the horizon, consumers in the US are also more cautious and spending less.”

While container freight rates are expected to continue to normalise in 2023, Tan is of the view that the drop will not be as big as this year given that they have fallen to near their 2019 levels.

“The rates might drop a little bit more or they might stabilise. But I don’t expect the rates to go up in the foreseeable future, especially next year when people are worried about a recession coming,” he points out.

The Drewry World Container Index, which measures the cost of shipping an FEU container in eight major routes to/from the US, Europe and Asia, had dropped 79% from the peak of US$10,377 reached in September 2021 to US$2,139 on Dec 8. The composite index is 77% down from a year ago.

On the local front, the Bursa Malaysia transportation and logistics index has fallen about 3.5% year to date (YTD), while the benchmark FBM KLCI has lost about 5% over the same period.

The air cargo market, which has been a bright spot in a pandemic-battered airline industry, has also seen rates out of Asia fall as air cargo volumes decrease. The Freightos Air Index showed that rates from China to North America and Europe had dropped more than 40% as at Dec 8 compared with the end of November a year ago.

Tan says with about half of the world’s air cargo carried in the belly of passenger aircraft, the sharp reduction in flights due to grounded passenger aircraft during the pandemic led to air cargo prices rising at a historic pace. “Since then, the situation has reversed on the back of increased capacity as passenger airlines restored more flights since the pandemic, although it remains below that of pre-pandemic level. Also, as ocean carrier capacity increases and rates fall, shippers are switching modes back to the cheaper sea freight,” he adds.

In a Nov 29 statement, Association of Asia Pacific Airlines director-general Subhas Menon said declining business confidence, against a backdrop of rising risks to the global economy, led to a slowing in orders for manufactured goods, which in turn led to a 5.5% year-on-year (y-o-y) decline in air cargo demand for the first 10 months of the year.

Mark Jason Thomas, the newly appointed CEO of MAB Kargo Sdn Bhd (MASkargo), says the company has been seeing a shift in popular trade lanes. “In terms of demand, there is a sharp decline in emerging markets, which ultimately is putting pressure on our yield. In a nutshell, there are higher capacity, lower load and softer yield,” he says in an email response to questions from The Edge.

Notwithstanding a bearish air cargo market, Thomas says MASkargo’s volumes remain strong due to the agility in its network planning, as its focus has always been on capitalising on high demand sectors.

MASkargo saw net profit grow 29.6% to RM454.98 million in the financial year ended Dec 31, 2021 (FY2021), from RM351.12 million in FY2020, while revenue increased 52.1% to RM3.01 billion from RM1.98 billion in that period.

“Capacity has increased by 20% y-o-y with the main driver being the resumption of passenger flights, with the average load factor standing at about 70%. As we see gradual recovery in air passenger traffic, belly cargo capacity is expected to further improve, which will result in a decline in yields for the overall freighter business as more capacity is put back online,” Thomas notes.

He sees challenges ahead for the air cargo industry in 2023. “The demand for charter has been low, translating into lesser demand for urgent consignments by air. Another factor contributing to the subdued operating climate is the steadiness in the maritime sector, which is taking the demand off of airfreight.

“We are also looking at overcapacity where passenger flights have resumed to almost pre-pandemic levels, coupled with new entrants emerging out of the pandemic.

“Thus, our outlook remains passive. As the world recovers from the effects of the pandemic, the sector will also have to be mindful to mitigate the onset of challenges ahead, including resource constraints led by labour supply issues and further demand uncertainty driven by lower production by major factories,” says Thomas.

As for MASkargo, the biggest challenge faced by the cargo arm of Malaysia Aviation Group Bhd is the imbalance between supply and demand now that belly capacity has rebounded to almost pre-pandemic normalcy, he continues.

“Added to this are the economic uncertainties already touted by world experts. According to the International Monetary Fund, the global economic activity is experiencing a broad-based and sharper-than-expected slowdown, with inflation higher than seen in several decades. The cost-of-living crisis, tightening financial conditions in most regions and the lingering pandemic all weigh heavily on the outlook. This is on top of the volatile fuel prices and foreign exchange.

“Another challenge which looms heavily on us is the competition, especially within the Asean region as well as capacity offered by other modes of transport, namely road, rail and sea. Finally, the impact from customer behaviour where they are cost-driven instead of considering the cycle time,” Thomas explains.

Multimodal logistics providers to mitigate lower rates better than pure freight players

Still, analysts and freight forwarding companies believe that the latter’s multimodal logistics business model with operations across multiple geographies should continue to hold them in good stead in an environment of lower freight rates in 2023, compared to pure freight players.

For Tasco, volumes are still holding up despite the continuous drop in freight rates, thanks to new customers.

“If you look at our air freight and ocean freight forwarding segments, their revenue contribution [to the group] for 2QFY2023 has reduced on a quarter-on-quarter basis. However, we still managed to achieve better results in a broad-based manner, with both our contract logistics and cold supply chain divisions reporting significantly better results. The reopening of the economy has also generated more economic activities and enabled us to secure quite a number of major customers, which helped prop up our volume and mitigate the rate decline,” says Tan.

“Even if there is a recession next year, we feel we will be able to weather it because of our diverse client base, which encompasses various economic sectors. Some industries will continue to do well in a recession, such as food.”

Tasco’s net profit for its second financial quarter ended Sept 30, 2022 (2QFY2023) shot up 54% y-o-y to RM24.13 million, thanks to stronger contributions across its business segments. Revenue rose 57% y-o-y to RM493.95 million.

Net profit for the cumulative six months (1HFY2023) increased 54% to RM48.56 million from a year earlier, while revenue grew 56% y-o-y to RM947.51 million.

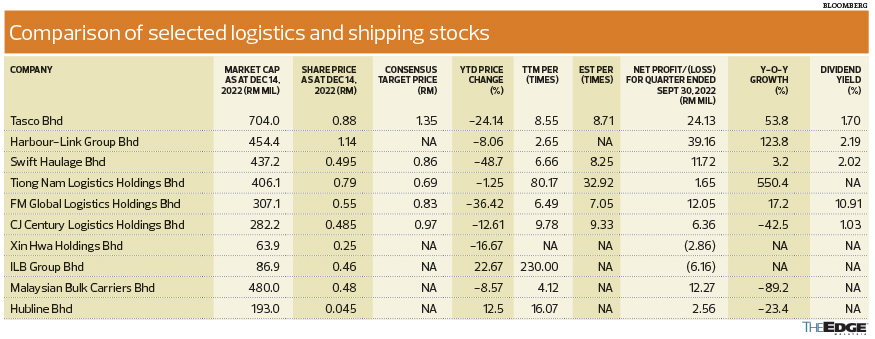

RHB Research analysts Lee Meng Horng and Raja Nur Aqilah Raja Ali point out that the sustainable outstanding performances in the past few quarters highlight the importance of operational excellence and Tasco management’s strategy in defying investors’ expectations of an earnings contraction due to the downward trend in freight rates, which has led to YTD share price underperformance. The counter has fallen 24% so far this year to close at 88 sen last Wednesday, giving the company a market capitalisation of RM704 million.

In a Nov 1 report, the analysts project Tasco’s near-term performance to be underpinned by robust trade flows — in spite of the slowing global economy — as well as new business wins across multiple industries, and the integrated logistics solutions tax incentive booster, which should support earnings.

CGS-CIMB Research analyst Walter Aw expects declining global freight rates to likely weigh on the profitability of FM Global Logistics Holdings Bhd in the financial year ending June 30, 2023 (FY2023) as premiums decline.

“Still, we expect FM Global Logistics to partially mitigate the impact of weaker freight charges via higher freight volumes given lower freight charges; increased focus on cross-selling; and higher cost efficiencies. Overall, we forecast 6.9% and 1.9% y-o-y declines in FY2023 and FY2024 net profits [respectively] before a return to profit growth in FY2025, as we assume a further erosion in margins as freight rates decline going forward,” he says in a Nov 29 note.

FM Global Logistics’ net profit for 1QFY2023 rose 17% y-o-y to RM12.05 million, owing to higher contributions from Malaysia and overseas. Revenue rose 42% y-o-y to RM303.23 million.

Aw is maintaining an “add” call on FM Global Logistics, with a lower target price of 65 sen from 82 sen previously. The stock is down 36% YTD, closing at 55 sen last Wednesday and valuing the group at RM307.1 million.

Larger dry bulk vessels face further pressure in 2023

Meanwhile, the Baltic Dry Index, a bellwether for global dry bulk shipping, closed at 1,357 points on Dec 13, down 38.8% since the beginning of 2022, amid significant uncertainty in economic activity, the Russia-Ukraine conflict and seasonal corrections.

In an Oct 3 report, Moody’s Investors Service says with global gross domestic product growth slowing, it expects dry bulk charter rates to be lower over the next 12 months after hitting multiyear highs in 2021.

“Chinese imports of iron ore, which tend to drive Capesize charter rates, have weakened. However, looking at 2023 and beyond, the low likely growth in vessel supply over the next two years will help keep charter rates relatively elevated,” it adds.

It notes that one-year time charter rates for Capesize ships, which often transport iron ore needed for steel production, are now trending at about US$20,000 per day — a level similar to the pre-pandemic 2018-2019 average, but much lower than the rates of well over US$30,000 per day that prevailed in October 2021.

Dennis Ling Li Kuang, CEO and managing director of Hubline Bhd, says the dry bulk rates for the company’s shipping segment in its fourth financial quarter ended Sept 30, 2022 (4QFY2022), were in line with its 3QFY2022 rates. “Since January 2022, freight rates have increased by about 20%,” he says.

Hubline’s net profit fell 23% y-o-y to RM12.93 million for the full financial year ended Sept 30, 2022 (FY2022), owing to losses suffered by the aviation segment. Revenue rose about 50% y-o-y to RM229.17 million.

“The performance of our dry bulk shipping business segment had actually improved between FY2021 and FY2022. For Hubline, this business segment achieved profit before tax (PBT) of RM5.1 million in FY2021, increasing to RM19.8 million in FY2022.

“When reviewing the latest quarterly report announcement, it would appear that the profit was lower in FY2022 when compared with FY2021. However, the PBT was in fact higher in FY2022 (RM20.61 million) compared with FY2021’s RM18.07 million. It is also worth noting that the PBT of RM18.07 million for FY2021 was mainly due to a RM10 million profit from the sale of a subsidiary whereas for FY2022, the profit was derived from operations,” stresses Ling.

While the global supply chain issues have not been fully resolved, he points out that the cargo that Hubline carries are not directly linked to such commodities.

“We do foresee some downward pressure on dry bulk shipping freight rates, but bunker costs have also come down quite significantly. Our shipment orders continue to be promising for 2023 and the group’s expectations for this business segment remain encouraging.

“Our advantage is that we are operating in a niche market as our vessels can call on smaller ports where larger vessels cannot call on due to draft problems. Our challenge is the possibility of large capacities coming into our market. This is not likely to happen soon,” says Ling.

Though there is a general slowdown in world economies and a weak growth in China at the moment, Hubline can look forward to China gradually opening up, which will be a boost to Asean countries including Malaysia, he continues. “We are still positive on our outlook.”

The Sarawak-based shipping firm, which owns 23 sets of tugs and barges, recently took delivery of another set.

“For the aviation segment, the general aviation business will continue to perform well as it has been successful in procuring and implementing aviation contracts. The flying academy, however, continues to face challenges as student intake remains slow. Nevertheless, we remain cautiously optimistic that this situation will improve in 2023, although the shipping segment will continue to be the main contributor,” Ling says, adding that Hubline’s diversification from shipping into aviation has worked well. The company’s fleet currently stands at 23 aircraft.

“We are now looking at other areas to diversify [into]. It is oil-and-gas-related services, but we will make an announcement when things are firm.”

In announcing its third-quarter results on Nov 23, dry bulk shipping company Malaysian Bulk Carriers Bhd (Maybulk) said the dry bulk market has softened since the beginning of 3Q2022. It saw a slight reduction in charter rates to US$19,269 per day in its third quarter ended September 2022 (3QFY2022) from US$19,318 per day in 2QFY2022.

As a result, its revenue and operating profit in 3QFY2022 were RM29.34 million and RM11.43 million, down 13% and 21% from RM33.73 million and RM14.47 million in 2QFY2022 respectively.

“We expect to see dry bulk freight levels for 2023 to be at levels lower than 2022. The group does not foresee a reversal of this trend in the immediate term and will continue to deploy short- to medium-term charters to mitigate against volatile market conditions,” Maybulk says in its filing with Bursa Malaysia.

Hubline’s share price is up 13% YTD, while Maybulk’s has fallen about 9%.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.