This article first appeared in The Edge Malaysia Weekly on November 28, 2022 - December 4, 2022

THE dire situation in the local last-mile delivery market, thanks to oversupply and cut-throat competition, is unlikely to go away anytime soon, with analysts expecting the two main players — Pos Malaysia Bhd and GDEX Bhd — to remain in the red for the next two years.

Analysts are lowering their earnings estimates for both Pos Malaysia and GDEX in the financial years ending Dec 31, 2022 and 2023 (FY2022 and FY2023) to reflect the latest quarterly results. They now expect the two last-mile delivery players to post a net loss.

Earlier, several analysts had estimated that Pos Malaysia could see a turnaround in its operations in the second half of this year. But that changed after it posted its 15th consecutive quarterly loss in the third quarter ended Sept 30, 2022 (3QFY2022).

According to RHB Research, Pos Malaysia is only expected to return to profitability in FY2024. “Our previous expectation of a turnaround in 2HFY2022 proved too optimistic, and we now expect the narrowing of losses to be more gradual — deepening our FY2022 forecast loss to RM108 million from RM48 million as we expect parcel volume loadings to further soften,” the research firm said in a report last Tuesday.

“We expect FY2023 to still be loss-making at RM51 million, while a full-year turnaround is only expected in FY2024,” it added.

For 3QFY2022, Pos Malaysia narrowed its net loss to RM33.63 million from RM43.9 million a year ago, on the back of an 8.3% decline in revenue to RM492 million from RM536.26 million previously.

The group attributed the drop in its top line to lower overall parcel volume, especially from contract customers, major e-commerce players who leveraged their insourced delivery capabilities, and international players who pursued penetration strategies to capture higher market shares in the courier business.

For the cumulative nine-month period (9MFY2022), Pos Malaysia posted a smaller net loss of RM69.25 million compared with RM212.52 million in 9MFY2021, while revenue fell 10.3% to RM1.49 billion from RM1.67 billion during that period.

Pos Malaysia group CEO Charles Brewer expects the outlook of the group’s financial performance to continue to remain challenging due to macro-economic headwinds that will impact consumer sentiment.

“Additionally, accelerated in-sourcing by e-commerce marketplaces, aggressive pricing practices and ‘masking’ (where merchants can’t choose their courier providers) continue to put pressure on parcel volumes, not just for Pos Malaysia but for all courier and logistics players in the country,” he said in a statement last week.

Kenanga Research said Pos Malaysia has missed the consensus estimate of RM63.9 million losses for FY2022 after it posted RM57.2 million core net loss for 9MFY2022.

As such, the research house is expecting Pos Malaysia to post higher losses this year and in FY2023, by 19% and 59% respectively.

“It (Pos Malaysia) registered another quarterly loss as its conventional mail business struggled to stay relevant, dragged further by declining courier volume on aggressive pricing practices and accelerated in-sourcing by e-commerce players,” Kenanga Research said in a report to clients.

It also raised its concerns on Pos Malaysia’s declining courier volume due to intense competition from new players such as J&T Express and Ninja Van that “undercut aggressively on rates” to grow their market share.

“Also, Pos Malaysia’s cost-cutting measures are insufficient to counter its weakening core business revenue,” Kenanga Research added.

According to Bloomberg data, of four analysts who covered the stock, three had a “hold” call and one rates it a “sell”, with an average target price of 55 sen a share. Shares of Pos Malaysia had fallen 12.5% year to date to close at 60 sen apiece last Thursday, giving it a market capitalisation of RM461.81 million.

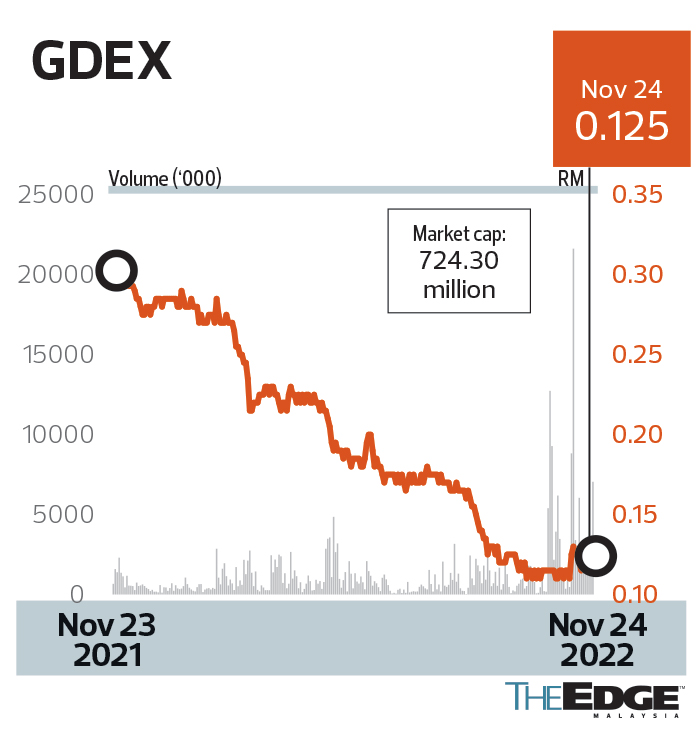

The industry oversupply and intense competition is also impacting GDEX. Last week, the logistics and express carrier slipped into the red, positing a net loss of RM6.57 million for 3QFY2022 — its third consecutive quarter of losses — compared to a net profit of RM9.47 million a year ago, on weaker earnings contributions from the courier and logistics services segments. Revenue for the quarter dropped 7.4% to RM95.28 million from RM102.86 million in 3QFY2021.

RHB Research said GDEX has missed the consensus estimates again, leading to the research firm revising downward its outlook for FY2022 and FY2023. It now expects the company to post about RM15 million and RM2 million in losses for FY2022 and FY2023 respectively, compared to profits of RM8 million and RM17 million.

“We believe the softening of online activities as a result of the resumption of physical retail businesses should entail a further drop in volumes handled by GDEX in the coming quarters.

“Meanwhile, the stiff price competition among players within the courier landscape (resulting from new alternatives in the market) are likely to continue — adding pressure to volume loadings,” it said.

On GDEX’s automated sorting hub, RHB Research said while it would increase the company’s parcels volume handled, the competitive business environment will result in lower average selling prices for last-mile delivery services.

“GDEX’s balance sheet is robust, as it is in a net cash position, which should allow it to comfortably embark on any merger and acquisition in the event of a consolidation of courier players,” it pointed out.

As at Sept 30, GDEX had a net cash position of RM268 million.

Call for help

GDEX managing director Teong Teck Lean says there is an urgent need for government intervention to ensure the sustainability of the last-mile delivery industry.

“By doing so, the competitiveness of the last-mile players can be enhanced to enable expansion to the region and globally,” he tells The Edge.

“This will give rise to opportunities for some domestic players to grow their business and, at the same time, become an essential infrastructure of the country. If the government does not intervene soon, we believe there will be many local casualties in this space.”

It is worth noting that the local last-mile delivery industry has been operating in a very competitive environment that led to razor-thin margins for industry players, with many dependent on volume to stay afloat.

For perspective, Malaysia, with a population of 33 million, has granted 122 courier licences. In comparison, Thailand, with a population of 70 million, has granted only half as many, while Indonesia has 42 for a nation of 273 million.

Many players are exiting the industry, with the latest being Nationwide Express Holdings Bhd, which will cease operations on Dec 15. Founded in 1985 by the late businessman Tan Sri Basir Ismail, it was a leading courier service provider in Malaysia.

Other companies such as KTM Distribution Sdn Bhd, which had a 38-year presence in the courier and logistics business, terminated its operations on Nov 1. CJ Century Logistics Holdings Bhd sold its loss-making courier arm last year for about RM7.5 million.

Teong, who is also the president of the Association of Malaysian Express Carrier, which represents 25 major courier companies in the country, sees more shutdowns ahead. “Definitely. There will be more roadkill ahead. This is an urgent matter that needs immediate attention from the government and regulators because the industry employs 150,000 local employees.”

He notes that the last-mile delivery market is overcrowded, with many start-ups dumping prices to gain market share.

Teong says some e-commerce platforms have also removed choices of delivery partners. “As a result, GDEX and other players have lost a lot of opportunities to deliver items for merchants who sell on e-commerce platforms, even though these merchants are willing to pay for the delivery service on their own.”

Teong points out that the industry’s volume has dropped 20% since last year. However, the number of complaints received by the Postal Forum has increased by 30%.

Looking ahead, Teong says GDEX will be focusing on optimising its processes and resources to help cushion the increased costs, without impacting the quality of service. “GDEX’s strategy is to differentiate our services by launching new products to enhance the customer experience in the first half of next year. The fully automated sorting hub is expected to be up and running then as well, which will double the sorting capacity to 350,000 packages a day, which will result in enhanced productivity and turnaround time,” he adds.

GDEX shares have fallen 56.14% year to date to close at 12.5 sen last Thursday, valuing the company at RM724.3 million.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- BNM to pay record RM5.25b dividend to govt as profits hit 27-year high in 2024

- MMAG's share price plunges more than 15%, intraday short selling suspended

- Penang Turf Club to be sold in parcels — sources

- Malaysia's Macrovalue to acquire Cold Storage and Giant supermarkets in Singapore for RM414 mil

- Borneo Oil chosen as Petronas’ Sabah vendor, teams up with Chinese firm to bid for drilling projects

- Opec+ likely to proceed with planned May oil output hike, Reuters reports

- Trump to impose 25% tariff on countries that buy oil, gas from Venezuela

- Over 51,000 shops affected by tobacco display ban starting April 1 — MOH

- Oil climbs 1% as Trump plans tariff on countries that buy Venezuelan oil, gas

- India to seek tariff reprieve in meeting with US officials, Bloomberg reports