This article first appeared in Forum, The Edge Malaysia Weekly on June 7, 2021 - June 13, 2021

When what is said in the headlines happens, what does it mean for the palm oil industry in Malaysia?

We need to start with the Paris Agreement, which is a landmark in the multilateral climate change process because, for the first time, there is a binding agreement that brings all nations into a common cause to undertake ambitious efforts to combat climate change and adapt to its effects.

It was adopted by 196 parties, including Malaysia, at the 21st Conference of the Parties (COP 21) of the United Nations Framework Convention on Climate Change Conference in Paris on Dec 12, 2015. Its goal is to limit global warming to well below 2°C, preferably to 1.5°C, compared with pre-industrial levels.

To achieve this long-term temperature goal, countries aim to reach global peaking of GHG (greenhouse gas) emissions as soon as possible to achieve a climate-neutral world by 2050. As we are already at 1.2°C, the situation is becoming urgent, with some calling climate change a climate emergency.

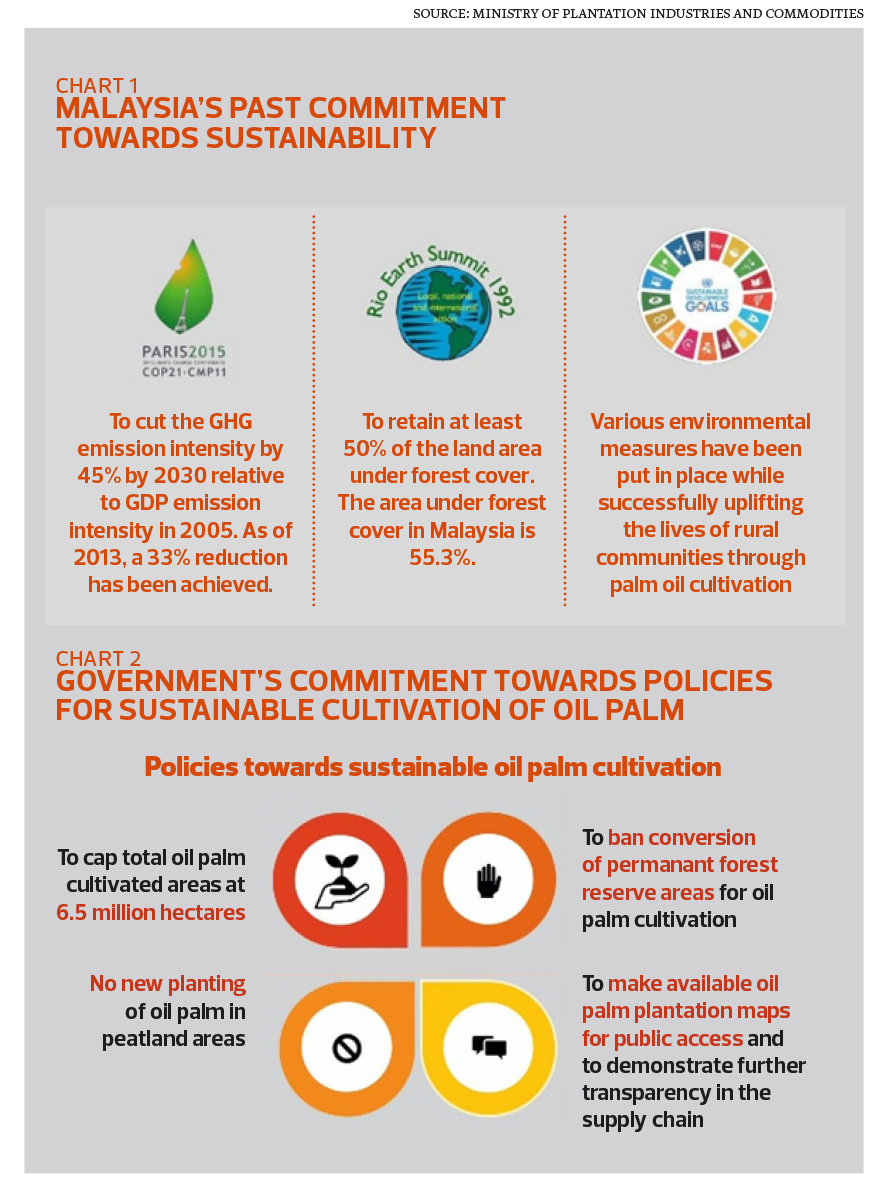

Malaysia’s commitment

At the Palm Oil Trade Fair and Seminar 2021 on Jan 5, Datuk Ravi Muthayah, secretary-general of the Ministry of Plantation Industries and Commodities, shared a presentation slide on what Malaysia has achieved (see graphic). You will note that Malaysia is committed to cutting the GHG emission intensity by 45% by 2030 relative to the GDP emission intensity in 2005. As of 2013, a 33% reduction has been achieved. To achieve the remaining 10%, we are waiting for climate finance, technology transfer and capacity building from developed countries.

Malaysia will cap palm oil cultivation at 6.5 million hectares (currently 5.9 million hectares or 18% of the total land area in the country). Some of these policies are being reflected in the working groups that are busy with the five yearly

systematic review of the Malaysian Sustainable Palm Oil (MSPO) Standards (MS2530:2013 series and Supply Chain Certification Standard). The revised Draft MS 2530:2013 Series Standards is now available for public comment from May 1 to July 4.

COP26 in Glasgow (Nov 1-12)

The Paris Agreement works on a five-year cycle of increasingly ambitious climate action carried out by countries. By 2020, countries had to submit their plans for climate action, known as nationally determined contributions (NDCs). This has been delayed by the coronavirus pandemic.

In the meantime, more than 126 governments around the world have made some sort of pledge on net-zero carbon emissions. It is already a law in some countries — for example, Sweden (by 2045) the UK (2050), France (2050), Denmark (2050), New Zealand (2050), Hungary (2050), China (2060) and Japan (2050). The US, the biggest CO-e emitter after China, has just rejoined the UNFCCC COP.

The US president hosted a virtual Leaders’ Summit on Climate (April 22 and 23) as a prelude to COP 26. Malaysia was not invited, probably because it is not demonstrating strong climate leadership or charting innovative pathways to a net-zero economy. Nevertheless, the country is not only vulnerable to climate change but can impact it as well.

COP26 is considered significant as it will be the first COP to take place after the Paris Agreement’s measures take effect. Nations will come together to review their commitments and strengthen their ambitions as the urgency increases.

Malaysia’s progress

In the last few months, the momentum towards addressing climate changes issues appears to have picked up. Tenaga Nasional Bhd declared that the Jimah electricity-generation facility, commissioned in 2019, is the last new coal-fired power plant in the country.

National oil corporation Petroliam Nasional Bhd (Petronas) has pledged net-zero aspirations by 2050. Renewal energy has gone from 2% in 2008 to 10% against the 20% target in 2025. The recent LSS4 (large-scale solar programme) award by the Energy Commission has increased this by 3%. Hopefully, there will be more news in the pipeline in the build up to COP26.

It is inevitable that Malaysia will embrace net-zero carbon emissions. It is better to do so earlier rather than later as remedial costs are very high. Jimah will retire in 2033. Retrofitting it for CCUS (carbon capture, utilisation and storage) is very expensive and carbon capture technology exacts an “energy penalty” of 25% to 40%.

The transition requires, besides political will, massive structural and legislative reforms. The process will involve all stakeholders and industry, not just the palm oil industry, which sometimes bears the brunt of uninformed accusations. Among other things, it should become clear how forests (if any) and land should be used for development.

The palm oil industry

The palm oil industry recognises the impact of climate change. With the rise in temperature, incidences related to water stress may become more prevalent. During times of drought, oil palm yield suffers significantly. Unusually long periods of flooding have also negatively impacted the supply because of harvesting difficulties.

The palm oil industry is quite well placed to meet the challenges of net-zero carbon emissions, having made an early start with the Roundtable on Sustainable Palm Oil (RSPO) in 2004. Many initiatives have been undertaken in the industry by the public as well as private sector.

1. Under the Malaysian Palm Oil Board (MPOB) licensing requirements effective Jan 1, 2014, new mills are required to trap/avoid methane gas emissions from palm oil mill effluent (POME). By 2019, 125 palm mills out of 452 had

biogas plants, with 30 connected to the national electricity grid. This is green electricity.

2. The current MSPO Standards review will bring it up another notch in the sustainability ladder. As Malaysia’s commitments are legislated, this will facilitate “shared responsibility”, not only across the palm oil sectors but all industries.

3. As palm biodiesel is a renewable source of energy, we can look forward to a marked increase in the use of palm biodiesel in Malaysia to meet its net-zero carbon emissions goal. Increasingly, low quality palm oil recovered from POME (about 2% to 3%) is being converted into value-added biodiesel while assuring the high quality of crude palm oil (CPO).

4. Oil palm biomass will be in demand as the second-generation biofuel. This will not only be for palm kernel shells (PKS) and palm mesocarp fibres (PMF) but also the less-easy-to-use empty fruit bunch (EFB). The palm mill is an excellent example of a self-sufficient production unit in terms of energy when it uses its own biomass and biogas. We can then consider such a mill to have net-zero carbon emissions.

We may see the revival of the production of bio oil using biomass-to-liquid technology as per Entry Point Project 7 (EPP 7) of the Palm Oil National Key Economic Area that was shelved in 2018.

5. The combined palm/palm kernel oil yields are nearly six times the next highest vegetable oil on a per hectare basis. Yet, palm oil yields have continued to increase from four tonnes per hectare to at least 10 tonnes based on the work of MPOB and the private sector. The carbon footprint per tonne of palm oil continues to go down.

Much work is also going on to reduce palm oil loss at the mill. The industry uses the term “oil extraction rate” (OER) and in Malaysia, this is between 19% and 21%. Based on the global production of palm oil in 2018, about three million tonnes of additional palm oil can be produced globally with a 1% increase in OER. Conversely, in both instances, less land will be required.

6. The industry has availed itself of digitalisation across all sectors. Currently, it is widely used for production management, improving efficiency, reducing cost and increasing productivity. A 3% to 4% increase in OER as a result has been claimed.

The potential for the use of data analytics in processing remains to be tapped, with the downstream sector most ready to do so and apply it, for example, in heat integration.

Climate change is now a climate emergency and it is good to see the two largest contributors — China and the US — come on board. Having said that, no country is spared from the effects of climate change, and the contribution from every country, no matter how small, is needed.

We can expect Malaysia to join the 126 or more countries in embracing net-zero carbon emissions. It will take strong political will in these difficult times, but it is better to do so earlier rather than later.

The palm oil industry is in a good position of having started its sustainability journey, which is inevitably tied to climate change, as far back as 2004. The MSPO is a key vehicle for this as it gains momentum and shortly crosses the 90% planted area certification milestone. The palm oil industry can seize this opportunity to rebrand

its sustainability story that net-zero carbon emissions present.

Ir Qua Kiat Seng is a senior lecturer at Monash University Malaysia and a fellow of Monash-Industry Palm Oil Education and Research (MIPO) Platform. He is also a member of the working group for the review of MSPO Standards (MS2530:2013).

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Li Ka-shing has little to lose as China threatens Panama deal

- HHRG’s largest shareholders dispose of entire stake at a steep 94% discount

- Petronas keeps mum on news of its possible exit from Argentina

- Pertama Digital acquires 80% stakes in two companies for RM106m as part of its regularisation plan

- BofA says US stocks rout is correction, not start of bear market

- Malaysia to fortify position as centre of competitive trade, finance and technology — Anwar

- Op Birth: Detained legal practitioner assisted syndicate in registering birth

- MACC opens two investigation papers involving Sapura Energy

- Schumer retreats on shutdown threat, enhancing bill’s prospects

- Wall St climbs after string of sharp losses as investors weigh tariff impact