The completion of Mitsui Shopping Park LaLaport (above) and Malaysia Grand Bazaar in Bukit Bintang in 1H2022 offered a combined one million sq ft of net lettable area of retail space (Photo by Knight Frank)

This article first appeared in City & Country, The Edge Malaysia Weekly on October 31, 2022 - November 6, 2022

As Malaysia transitions to the endemic phase of Covid-19, signs of economic recovery and growth have been apparent. According to the Knight Frank 1H2022 Real Estate Highlights report, the economy grew 5%, primarily supported by improved domestic and external demand, as well as continued policy support. Malaysia began moving to the endemic phase on April 1 this year, leading to the normalisation of economic activities.

Klang Valley retail to see overall improvement

In the Klang Valley, the retail market rebounded in 2021, following the gradual easing of strict containment measures in the four-phase National Recovery Plan (NRP). In 1Q2022, higher footfall at shopping malls plus the Chinese New Year festival created a positive outlook for the retail market, with a promising growth rate of 18.3%.

“For the entirety of 2022, the country’s retail sales growth has been revised upwards from 6.3% to 13.1% following the transition to the endemic phase earlier this year,” the report said.

The completion of Mitsui Shopping Park LaLaport and Malaysia Grand Bazaar in Bukit Bintang in 1H2022 offered a combined one million sq ft of net lettable area (NLA) of retail space. Both retail spaces are part of an integrated development comprising serviced residences, hotels, offices, retail and entertainment outlets, and transit hubs.

The report also indicated that as at 1H2022, the retail space supply was 18.38 million sq ft in KL fringe, 13.6 million sq ft in KL City and 34.11 million sq ft in Selangor.

The next half of the year (2H2022) will see the scheduled completion of four new shopping centres and retail components with a combined retail space of about 2.15 million sq ft; namely, KSL Esplanade Mall in Klang, IOI City Mall (phase two) in Putrajaya, Datum Jelatek’s retail component in Taman Keramat and EcoHill Walk in Semenyih, the report said.

Besides that, rising consumer demand for convenience and accessibility has hastened retailers’ initiatives to increase footfall at malls and retail outlets.

“Shifting consumer behaviour coupled with the acceleration in digital transformation amid the Covid-19 pandemic have led retailers and mall operators to increasingly adopt omnichannel strategies to improve sales and engagement,” the report said.

AEON Co (M) Bhd has accelerated its digital transformation by merging offline and online channels via various platforms including myAEON2go, AEON loyalty programme, iAEON app and AEON Living Zone. IPC and MyTOWN have created mobile apps with integrated mobile reward programmes and adapted to social commerce by introducing shoppable live streams, personal shopping services and campaigns with food delivery services, GrabFood and foodpanda. Atlas, one of Malaysia’s largest vending machine operators, has implemented Braille-enabled vending machines and Atlas TryBot for automated sampling.

As for sales transactions and rental rates, the report noted that occupancy rates have held steady while the revenue of shopping mall owners is improving. This is due to the lower rental rebates and discounts to tenants amid the rising foot traffic.

The rental rates of many retail spaces have gone down in 2021 compared to 2020. According to Knight Frank, the estimated rental rates were derived from the gross revenue of respective annual reports.

“Shopping icons in the Kuala Lumpur city centre, namely Suria KLCC and Pavilion Kuala Lumpur, command average monthly gross rentals of RM29 and RM25 psf (2020: RM33 and RM26 psf) respectively. The malls enjoyed commendable occupancy rates of 93% and 90.2% respectively.

“In KL fringe, Mid Valley Megamall and The Gardens Mall command average monthly gross rental of about RM13 and RM12 psf (2020: RM15 and RM14 psf) respectively. The occupancies of these malls remain high at around 97.8% and 90.7% respectively,” the report said.

Knight Frank highlighted that the resumption of economic activities in the endemic phase will bring overall improvement. However, rising inflation and the ongoing Russia-Ukraine war have caused a supply chain bottleneck, which may impede consumer spending.

Due to the change in consumer purchasing habits, omnichannel strategies — which integrate online and offline sales — are still essential for companies to continue in business. E-commerce is moving into a new phase in which on-demand services are assuming a significant role. Trends brought on by the pandemic will continue to exist as long as customers’ need for speed, convenience and safety exists.

Penang’s overall retail occupancy expected to improve

In Penang, the retail supply is seeing rapid expansion with upcoming malls underway. There were more than 108 operating shopping centres with a combined retail space of over 19.6 million sq ft as at 1Q2022.

Penang’s overall occupancy rate increased from 70.9% in 4Q2021 to 71% in 1Q2022. Simultaneously, George Town’s overall occupancy rate also increased to 74.4%.

Gurney Walk along Gurney Drive, which was officially opened in March 2022, offers 100,000 sq ft of retail space. Having secured major new retailers, the Sunway Carnival Mall extension in Seberang Jaya, which was completed in June 2022, brings its latest NLA to one million sq ft.

The report noted that ongoing and upcoming retail developments include Sunshine Mall, Klippa Batu Kawan, The Light City Mall and Penang Mitsui Outlet.

“Being part of Sunshine Central, the 9-storey Sunshine Mall will have a total of 142,000 sq ft to accommodate 412 retail stores and 3,500 parking bays. It is expected to be completed by 1Q2023.

“Ikano Centres Malaysia has officially unveiled its mixed-use development in Batu Kawan. Klippa Batu Kawan, spanning over 1.6 million sq ft of GLA (gross lettable area), will house more than 300 brands, including a petrol station with a Starbucks drive-thru,” the report said.

With the rising footfall and entry of new businesses like food and beverage (F&B), grocery, home décor, furnishing and accessories, the state’s retail sector is slowly getting back on its feet. More operators and retailers are implementing e-commerce and cashless platforms.

Positive retail growth expected in Johor

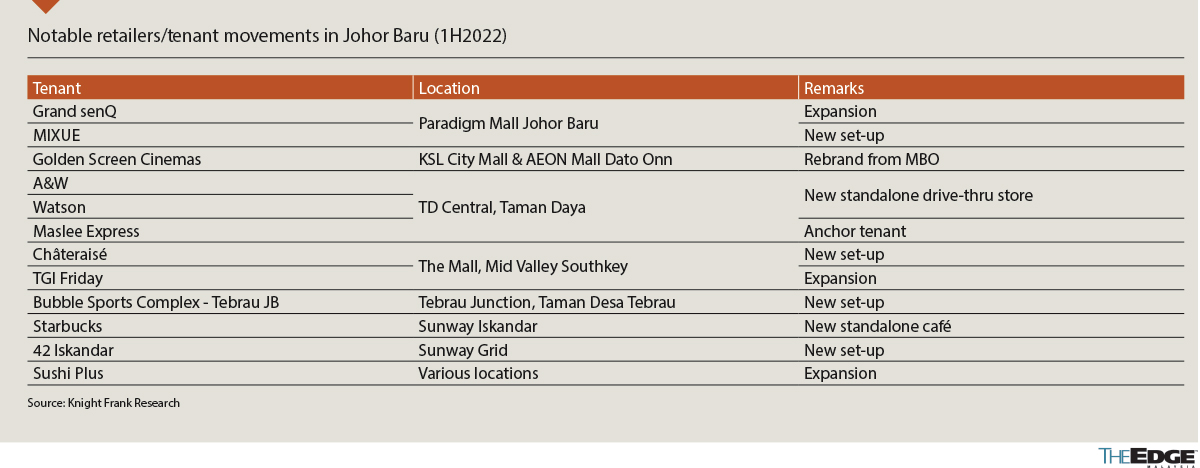

The retail market in Johor is anticipating positive growth. As at 1Q2022, Johor Baru’s total retail space supply was estimated at 20.4 million sq ft, with an overall occupancy rate of 71.6%.

TD Central in Taman Daya is a new retail project that was completed in 2021 and is anchored by Maslee Express. Watsons TD Central is the health and beauty retailer’s first outlet to offer a drugstore drive-thru service.

“A Chinese chain of fresh ice cream and tea stores, Mixue Bingcheng, debuted its first outlet in Malaysia at Paradigm Mall Johor Baru early this year while Châteraisé, a patisserie with 460 outlets in Japan, is opening a new outlet in The Mall, Mid Valley Southkey,” the report said.

A large number of travellers enter Johor every day via the Causeway, therefore the country’s border reopening on April 1 this year has encouraged steady recovery in the retail market. The state’s retail market has also benefited from the increased foot traffic in malls.

Kota Kinabalu to witness stable footfall

In Kota Kinabalu, occupancy and rental rates in the retail market remain stable with tenant entries on a steadier pace. According to data from the National Property Information Centre (Napic), Kota Kinabalu’s shopping centres have 5.78 million sq ft of total retail space, with an average occupancy of 76.7% as at 4Q2021.

In comparison, the state had 5.84 million sq ft with an 82.1% occupancy rate for 2020. “The pandemic has had a pronounced impact on the Kota Kinabalu retail market as evidenced by the decline in overall occupancy rate,” the report stated.

However, the city’s established shopping centres, including Imago Mall, Suria Sabah Shopping Mall, Centre Point Sabah, Karamunsing Complex and City Mall, continue to record healthy occupancy rates of between 80% and 90%.

“In addition to promotional and advertising measures via digital marketing tools, mall operators ramped up efforts to conduct physical events and roadshows during the review period, particularly in conjunction with the Hari Raya Aidilfitri and Kaamatan (harvest) festivals,” the report said.

The state’s transition to the endemic phase has also improved consumer sentiment, which has resulted in a healthy return of shopper footfall to the malls, especially during weekends and public holidays, as mentioned in the report.

Industrial market set for growth

Malaysia’s Industrial Production Index (IPI) rose 4.5% year on year to hit 122.7 points in 1Q2022 compared with 117.4 points in 1Q2021. The manufacturing and electrical sectors performed well, which helped the IPI stay above the 100-point mark since June 2020.

“Year on year, the manufacturing and electricity indices grew 6.3% and 3.7% to record 133.2 and 120.2 points, respectively. In contrast, the mining index moderated 1.8% y-o-y to 94.7 points in 1Q2022,” the report said.

In May 2022, the S&P Global Malaysia Manufacturing Purchasing Managers’ Index (PMI) dropped to 50.1. Despite that, the PMI is expected to stay in the positive range following the country’s transition to the endemic phase.

The industrial property sector in the Klang Valley witnessed a resurgence of activity with 2,050 industrial properties worth RM9.21 billion transferred in 2021, reflecting annual increments of 20.2% and 23% in transacted volume and value respectively.

During 1Q2022, the Klang Valley registered 598 industrial property transactions with a collective value of RM2.61 billion compared with 518 transactions worth RM1.95 billion in 1Q2021.

“Year on year, the transacted volume and value were higher by 13.4% and 33.8%, although, on a quarterly comparison, there was moderation in market activity. Both the districts of Petaling and Klang were equally active in 1Q2022, garnering 22.1% and 21.2% of total industrial transactions in the Klang Valley. In terms of transacted value, Klang led with a 27.3% share, followed closely by Hulu Langat (23.6%),” the report said.

According to data collected by Napic and Knight Frank, the cumulative existing industrial property stock in the Klang Valley stood at 46,498 units. There are currently 1,522 units of ongoing industrial facility developments underway and 3,328 units under planned supply. Meanwhile, the boom in the logistics sector continues to be driven by the pent-up demand post-pandemic.

“Notable upcoming logistics hubs and distribution centres within the Klang Valley include the redevelopment of Axis REIT’s Bukit Raja Distribution Centre 2 and the redevelopment of two blocks of 4-storey warehouses in Shah Alam belonging to Symphony Warehouse Sdn Bhd.

“In addition, Atrium REIT’s ongoing major asset enhancement initiative (AEI) on its existing asset in Shah Alam into a 2-storey Grade A warehouse facility is targeted to be completed by 4Q2022,” the report said.

Meanwhile, prices and rental rates have seen a steady increase. Among them, Shah Alam appears to yield the highest rental rates, ranging from RM1.60 to RM2.20 psf per month.

The report also highlighted other localities like Kapar and Sepang, with monthly rental rates from RM1.40 to RM1.60 psf, and from RM0.90 to RM1.40 psf respectively.

“The asking prices of vacant industrial land in selected localities of the Klang Valley generally range from RM60 to RM180 psf, depending on the location, scheme, accessibility, land size, tenure, level of infrastructure and others,” the report further stated.

The surge in e-commerce usage, which increased the need for more storage space to accommodate the rise in last-mile deliveries, as well as the structural move towards omnichannel retailing, have all contributed to the industrial market’s steady expansion nationwide in recent years.

However, there are concerns regarding the rising transportation costs amid the shortage of labour and disruptions in supply chains. This has resulted in multinational corporations expanding their manufacturing facilities to the Asean region, a trend Malaysia may benefit from.

On the whole, the Klang Valley’s industrial market will continue to grow despite its challenges.

In Penang, the industrial market managed to secure manufacturing investments worth RM6.3 billion, with foreign direct investment (FDI) accounting for an 86% share valued at about RM5.5 billion.

“The state’s manufacturing investment achieved a record high of RM76.2 billion (versus RM14.1 billion in 2020) last year. This total investment surpassed the past cumulative investments worth RM73.1 billion (from 2012 until 2020). FDI contributed RM74.4 billion or 97.6% of the total investment share,” said Knight Frank.

In terms of outlook, the state’s industrial market is set to witness growth. As Penang Development Corp (PDC) plans to build between 100 and 150 acres of industrial land in Batu Kawan each year for the next three years, the Batu Kawan Industrial Park will continue to be the primary attraction, as highlighted in the report.

“In order to attract more foreign investors, Penang is also planning a smart and high-tech industrial park with the best infrastructure for 5G internet access in Kepala Batas. There is also encouraging demand for logistics facilities to serve the expanding e-commerce and logistics sector,” the report said.

In Johor, with the Port of Tanjung Pelepas (PTP) reporting a 14% increase in its annual volume, from 9.8 million twenty-foot equivalent units (TEUs) to 11.2 million at the end of 2021, the logistics industry is still recording impressive achievements.

“PTP will invest RM750 million to expand its capacity in 2022. Meanwhile, its current expansion of the Free Zone at an 81-acre site in Tanjung Adang is scheduled for completion by 2023,” the report said.

Both local and international companies are set for upcoming industrial developments in Johor. The following are some of the notable transactions. With the purchase of a logistics warehouse facility in PTP for RM390 million in cash, Axis REIT reached a new milestone as this marks the company’s largest acquisition to date. The REIT also paid RM16.3 million for the purchase of another industrial property in Kulai, Johor. The freehold property in i-park@Indahpura, Bandar Indahpura, has 59,956 sq ft of lettable area on a 98,393 sq ft plot of land.

Lion Industries Corp Bhd (LICB) has offered to sell all of its shares in Eden Flame Sdn Bhd for RM135.88 million in cash. Eden Flame is the owner of a long steel mill in Pasir Gudang, Johor, that produces billets that are rolled into steel bars and light sections like angle bars, flat bars and U-channels.

The opening of Hershey’s new research and development facility in Johor was announced recently. The 10,400 sq ft facility will likely rank among Hershey’s largest R&D facilities outside of the US.

Insulet Corporation in i-Tech Valley, SiLC (a freehold industrial park in Iskandar Puteri) broke ground on June 2. The plant, which will have a floor area of about 400,000 sq ft, is scheduled to open in 2024. It will produce the Omnipod Insulin Management System from Insulet.

South Korea’s SPC Group is investing RM130 million to build its first Paris Baguette halal-certified bakery manufacturing and distribution centre in Nusajaya Tech Park. Construction is scheduled to start in 3Q2022, and operations are expected to begin by June 2023.

Yondr Group announced its entry into Malaysia in March 2022 with the proposal to build a 200MW hyperscale campus on 72.8 acres of land it had acquired from TPM Technopark Sdn Bhd. The development is located in Sedenak Tech Park, formally known as Kulai Iskandar Data Exchange (Kidex), with the first phase scheduled to be completed in 2024.

Local conglomerate YTL Corp is also venturing into the data centre market. YTL Power International Bhd announced that construction has begun on the first 72MW of its 500MW data centre project in Johor through subsidiary, YTL Data Center Holdings Pte Ltd.

With 275 acres set aside for data centre development, the future YTL Green Data Centre Park is anticipated to meet the region’s expanding demand for sustainable and cost-effective data centre solutions.

Another company entering the data centre market is GDS Holdings, with its new data centre campus at Nusajaya Tech Park launched in April 2022. The company will invest about RM1.38 billion in its hyperscale data centre campus.

Overall, the industrial property market of Johor is set for growth due to numerous notable acquisitions along with the expansion of logistics warehouses and data centres.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Maybank announces departure of CFO after internal inquiry; Khalijah plans legal action

- SUKE subcontractors file RM500 mil lawsuit against Prolintas subsidiary, alleging corruption and conspiracy

- EcoWorld Malaysia sells second plot of Johor land to Microsoft for RM694 mil

- Central banks of Malaysia, Indonesia, Thailand adopt local currency transaction guidelines

- 99 Speed Mart 20% down from peak ahead of result release