This article first appeared in The Edge Malaysia Weekly on September 26, 2022 - October 2, 2022

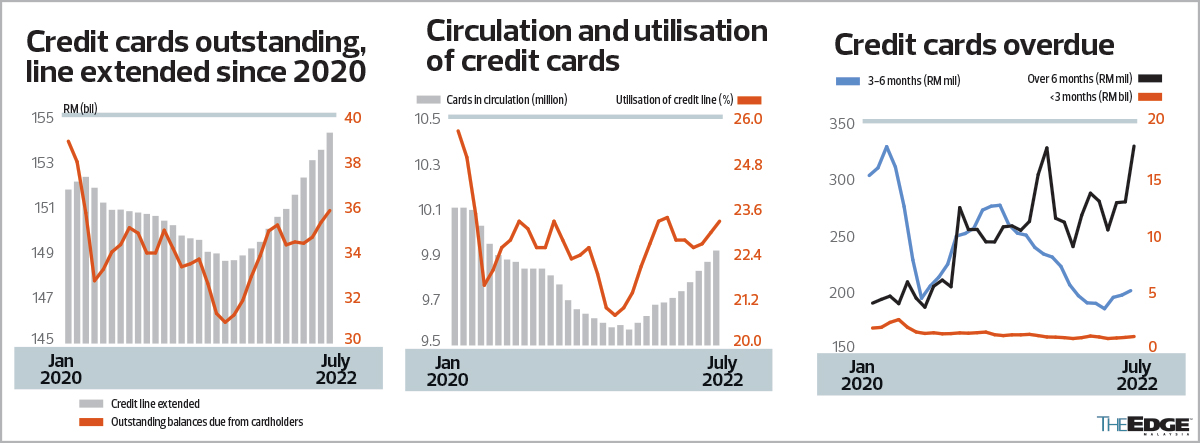

CREDIT card usage in Malaysia appears to have increased in recent months as consumers return to their pre-pandemic life. Bank Negara Malaysia data shows that outstanding balances of credit cards had increased for the third consecutive month to RM35.89 billion in July — the highest since February 2020 when the balance stood at RM38.05 billion.

This is an indication that consumers are loosening their purse strings to spend more. In addition, the inflationary pressure that has resulted in higher prices is also contributing to larger amounts being spent.

Total consumer credit line, commonly known as credit limit, offered by credit cards broke a new record of RM154.34 billion in July, according to the central bank, after having risen steadily over the past 12 months.

This coincides with an increase in the number of credit cards in circulation, including supplementary cards, from 9.57 million in September last year to 9.92 million in July, and getting closer to the 10.1 million mark reached in March 2020.

Banks are issuing more credit cards as more people are employed. The unemployment rate has been on a decline — to 3.7% in July, from 3.8% in June and 3.9% in both May and April.

Nonetheless, the utilisation of credit lines granted by credit cards (the ratio of outstanding balance to total credit line extended) is not that high — it has stayed below the pre-pandemic level of 24% for more than two years since the outbreak of Covid-19. The recent increase in the use of credit cards in the May-July period did not push the credit line usage higher either.

Apart from inflation, which has driven up prices, the increase in credit card usage could have been driven by improving labour market conditions, higher salaries and, hence, accessibility to credit, says Julia Goh, senior economist at UOB Global Economics and Markets Research.

“Coupled with [the economy] reopening, higher mobility and the release of pent-up demand [have led to an increase in] private consumption and credit card usage. There are also more interest-free instalment plans and financing options available that have spurred credit demand,” Goh tells The Edge.

Last Friday, the Department of Statistics Malaysia reported that food prices have driven August inflation to increase further at 4.7%, bringing the year-to-date Consumer Price Index (CPI) to 3.1%.

In a Sept 23 note, RHB Research economist Chin Yee Sian says the trajectory of inflation would very much depend on the timing and scale of the fuel and food subsidy adjustment going forward.

“Headline CPI inflation could peak in 3Q2022, with the balance of risks tilted towards delays. The sources of inflation are broadening to the services sector from food-related components.

“The demand side pressures on core CPI inflation are likely to remain elevated in 2H2022 as we see limited risks of deterioration in labour market conditions,” says the economist, who has raised the research house’s 2022 CPI forecast to 3.4% from 3.2%, after which it is expected to moderate to 2% next year.

Malaysia’s gross domestic product (GDP) grew 8.9% in the second quarter of this year following the reopening of the economy in April, and the Ministry of Finance foresees that growth may even surpass official estimates of between 5.3% and 6.3% in 2022.

However, UOB’s Goh cautions that there is risk of excessive build-up of consumer debt, especially for those with low financial literacy or poor financial management, coupled with unstable incomes.

Citing statistics and surveys by the Credit Counselling and Debt Management Agency (AKPK), she says this segment of cardholders is vulnerable to bankruptcy.

“Though at this point, the percentage of credit card debt is small at 2.5% of total household loans,” she says, adding that the banking system’s credit card delinquency rate is low.

“Nevertheless, debt-driven growth is considered unsustainable in the medium term. Sustainable consumption trends must be supported by higher incomes, lower unemployment and increased productivity,” she says.

Bank Negara data shows that the overdue amount for credit cards, with outstanding balance of less than three months and three to six months, has seen a slight increase since April.

Overdue of less than three months rose to RM1.17 billion in July, from RM987.88 million in April, while overdue of three to six months increased to RM202.33 million from RM186.34 million over the same period. Credit card overdue outstanding balances that are longer than six months have been increasing since April as well. It is worth noting that there was a sudden jump in July, to RM18.04 million — the highest level since March 2014 — from RM13.1 million in June.

It would be interesting to see if the usage of credit cards would continue to rise in the coming months, with cardholders facing monetary normalisation on the one hand, and mounting inflationary pressure on the other.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Powerful quake in Southeast Asia kills several, Myanmar declares state of emergency

- Genting says Nevada authorities have signed off settlement terms for Las Vegas complaint

- Hi Mobility makes modest 9% gain on Main Market debut

- Businessman who assaulted bodyguards for fasting sentenced to six years and 10 months' jail

- Tesla’s US$14b rally eclipses rout in other auto stocks

- Tremors felt in Penang after earthquake hits Myanmar

- CK Hutchison will not sell strategic ports at Panama canal next week, SCMP reports

- Hi Mobility makes modest 9% gain on Main Market debut

- Kenanga lowers valuations for chip packaging, testing firms as semiconductor cycle softens

- Chemicals firm SumiSaujana closes IPO applications with 1.85 times oversubscription