KUALA LUMPUR (June 23): The audit-turned-legal tussle between Serba Dinamik Holdings Bhd and KPMG has raised questions of whether a company can sue its auditor if the latter reports possible discrepancies to regulators.

Depending on the severity of the audit issues flagged by KPMG, the auditor’s action is guided by the Capital Markets and Services Act.

Under Section 320 of the Act, auditors are required to report to the Securities Commission Malaysia (SC) and the exchange any cases that adversely affect to a material extent the financial position of the public listed company (PLC), or any breach of securities laws and rules of the exchange.

And if they do so, they will enjoy legal protection in their employment and also be protected from being sued by the PLC.

The saga was made public when Serba Dinamik on May 25 notified Bursa Malaysia that KPMG had red-flagged certain bills and transactions in its 12-month period ended Dec 31, 2020 to the tune of over RM4 billion.

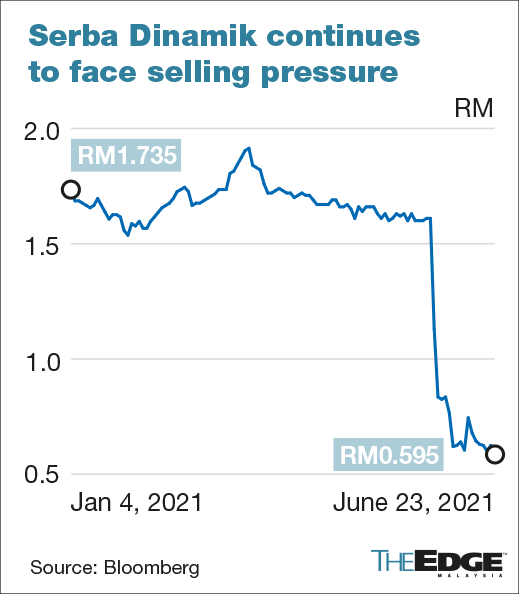

After making several board changes and expressing plans to undertake an independent review, Serba Dinamik pulled a surprise yesterday by filing a civil suit against KPMG for alleged negligence, breach of contract and breach of statutory duty.

Earlier today, KPMG said the audit was still being conducted in accordance with the relevant professional standards, and that it will vigorously contest any court proceedings.

At yesterday’s press conference, Serba Dinamik executives claimed that the issues could have been resolved if KPMG took steps to meet its clients and look at alternative procedures to determine the amount disputed.

Serba Dinamik’s legal counsel Tan Sri Muhammad Shafee Abdullah also expressed that the company's relationship with its auditor is no longer tenable, and that KPMG should resign.

According to Serba Dinamik, KPMG did not respond to the company for over eight weeks after informing that it will pause its audit until Serba Dinamik conducts an independent review of the findings.

“We found no infringement of law or non-compliance with provisions,” said Muhammad Shafee. “The key content is missing for KPMG to do whistle-blowing to the SC. As a result of unfavourable red-flagging of issues, the SC acted purely on what KPMG said and raided the premises of this company.”

Meanwhile, it is worth noting that Sections 430 and 120 of the Malaysian Institute of Accountants (MIA) by-laws states that a litigation between an auditor and a client will likely deter the accountant from acting objectively, and may only be addressed by ending the relationship.

This may be why Serba Dinamik decided to sue KPMG instead of trying to remove it via a shareholders' meeting as earlier planned.

But the MIA by-laws are said to be merely a code of conduct and it is not clear that given the gravity of the matter, the resignation of KPMG will resolve the core issues facing Serba Dinamik.

Read also:

Serba Dinamik to take legal action against external auditor KPMG for alleged negligence

No basis for legal action, says KPMG on Serba Dinamik suit

SC says Serba Dinamik probe ongoing and auditors must do their work without fear or favour

Serba Dinamik now says its board will meet on Friday to decide on independent review scope

Selling persists as Serba Dinamik sues KPMG for alleged negligence