KUALA LUMPUR (Sept 29): The impact on insurers’ and takaful operators’ earnings from premium deferrals as well as Covid-19 claims is expected to remain manageable, with insurers and takaful operators assessed to be resilient against stressed scenarios assuming higher claims than observed thus far, according to Bank Negara Malaysia (BNM).

Assumptions under stressed scenarios include Covid-19 related ex-gratia payments to policyholders and higher claims for policies without a pandemic clause, and a conservative increase in the general insurance claims ratio by up to 17%.

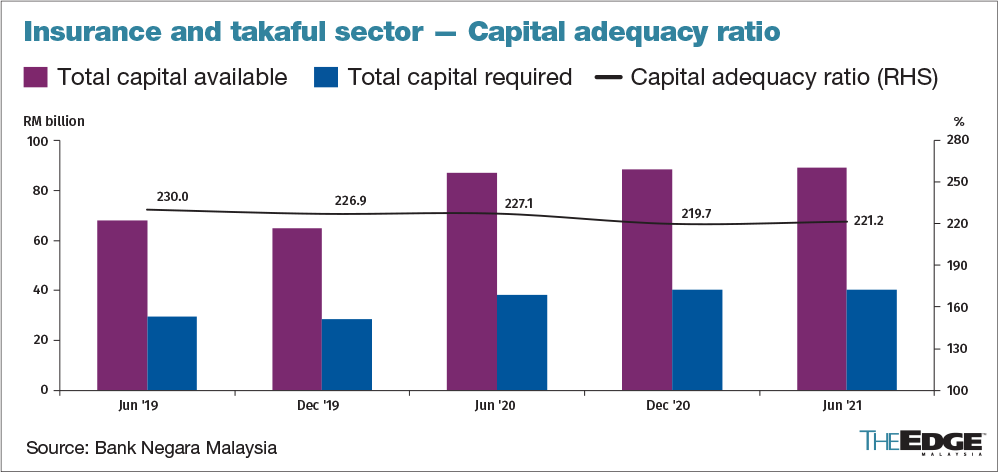

BNM noted that the aggregate industry capital adequacy ratio (CAR) of 221.2% remained well above the regulatory minimum of 130%. All insurers and takaful operators also continued to maintain capital ratios above their internal capital target levels that ranged between 150% and 250%.

As at end-June 2021, aggregate excess capital buffers above the regulatory minimum stood at RM36.8 billion.

“Going forward, financial market volatility and prospects of rising bond yields will continue to weigh on earnings of insurers and takaful operators given their sizeable financial investments. Nonetheless, the insurance and takaful sector is expected to remain resilient,” BNM said in its Financial Stability Review report for the first half of 2021 (1H21) released on Wednesday.

“A sensitivity analysis conducted on the balance sheet of insurers and takaful operators showed limited impact on their solvency positions in the event of a sharp rise in bond yields. This is underpinned by their strong capitalisation,” it added.

The central bank noted that some life and family insurers and takaful operators had introduced additional underwriting measures, including questionnaires to assess the Covid-19 medical history and risk exposure of prospective policyholders, as they take into consideration heightened risks arising from the pandemic.

It also observed that in selected cases, affected policyholders could be subjected to additional underwriting conditions, such as longer waiting periods. Higher premium loading could also be imposed on policyholders with indications of higher risk to develop serious health conditions, although this would be largely dependent on further medical assessments undertaken on a case-by-case basis.

Nevertheless, BNM said such practices had so far not been widely observed to suggest a broader tightening of underwriting conditions across insurers and takaful operators due to Covid-19.

“The impact on life and family insurers and takaful operators from temporary relief measures granted to policyholders remained limited. Affected policyholders have been afforded the option to defer premiums due under life insurance policies and family takaful certificates for three months without interruption in their coverage. This option, previously slated to expire by June 2021, has been extended until December 2021.”

Policyholders that availed the premium deferment option continued to increase, although the amount of premiums deferred and covered by premium holidays remained relatively small at 8.3% of premiums in force between March 27, 2020 and Sept 3, 2021.

A premium holiday refers to continued insurance/takaful coverage despite an absence of premium payments and applies to products with the premium holiday feature already in place, such as investment-linked products.

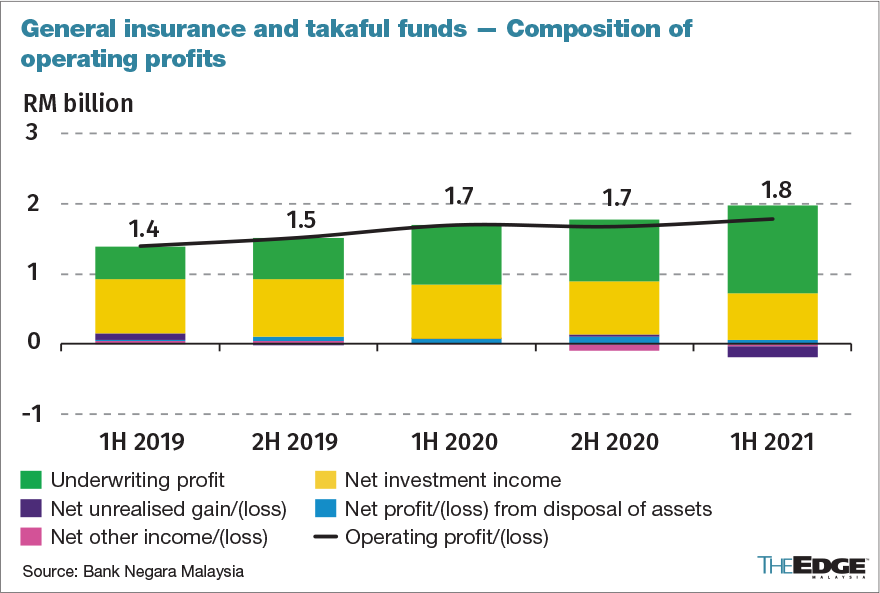

Profits for general and takaful insurers improved slightly in 1H

General insurance and takaful funds recorded a slight increase in operating profits to RM1.8 billion for 1H21 from RM1.7 billion for 1H20, driven by a better underwriting performance.

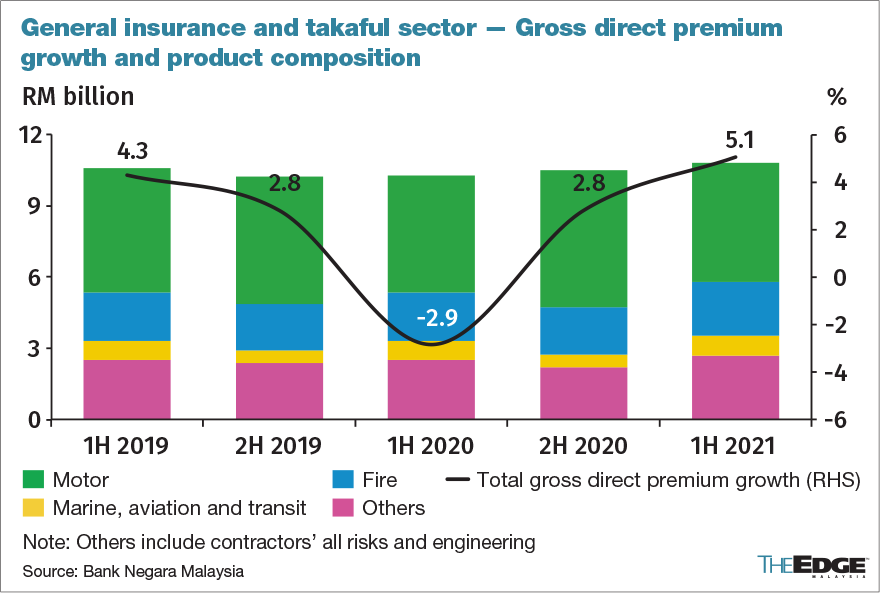

Gross direct premiums were bolstered by revised premium rates for the fire, contractors’ all risks and engineering segments following higher claims from several large fire and explosion incidents in the last two years, according to BNM.

Higher premiums were also supported, to a lesser extent, by a recovery in the motor segment amid a rebound in car sales following the extension of the vehicle sales tax exemption, which is in place until December 2021, and the easing of containment measures prior to the full movement control order (FMCO).

However, BNM noted that some smaller insurers and takaful operators continued to experience considerable earnings volatility in 1H21 due to higher reliance on investment income to support overall profitability.

“Risk of heightened volatility in the financial markets therefore remains significant for these insurers and takaful operators,” it said.

- Trump open to tariff cuts in return for ‘phenomenal’ offers

- China hits back at Trump with tariffs, limits on key exports

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- Karpal Singh Drive residents urge state government to halt land reclamation for Jelutong Landfill project

- 25 Putra Heights fire victims lent first batch of Chery Malaysia SUVs for a month on Friday

- Baffled Lesotho seeks to engage with US on jeans tariffs

- Strategic partnerships with global companies need to be enhanced, says Anwar

- Trump hits China tariff retaliation, says policy will remain

- Coffee declines on threat of demand blow from Trump tariffs

- Nasdaq heads towards bear market as trade war worries grow