This article first appeared in Capital, The Edge Malaysia Weekly on March 14, 2022 - March 20, 2022

THE ongoing Russia-Ukraine conflict is building a war premium into the price of gold, and this premium will persist for as long as the conflict continues, say market experts. The yellow metal has risen by 9% year to date, closing at US$1,997 per ounce last Wednesday as investors parked their cash in gold, as it is considered a safe haven in times of uncertainty as well as a hedge against rising inflation.

Gold surpassed US$2,000 an ounce to hit a high of US$2,069 per ounce last Tuesday (March 8) after the US announced an import ban on Russian oil. Prior to Russia’s invasion of Ukraine two weeks ago, gold was trading at about US$1,900 per ounce.

In a March 9 report, UOB Global Economics and Markets Research head of markets strategy Heng Koon How notes that Tuesday’s jump in gold spot prices was very close to the all-time high of US$2,072 registered in August 2020. “The move (on Tuesday) was triggered by the announcement by the White House on the start of the US embargo on Russian energy exports. US President Joe Biden announced that the US will now stop new purchases of Russian crude oil, liquefied natural gas and coal immediately, after allowing for a 45-day window to wind down previous contracted deals.

“Concurrently, the UK has also announced that it will phase out imports of Russian oil as well by the end of 2022, with a move to extend the ban to Russian natural gas. Both Brent and WTI crude oil rallied hard on the news, pushing above US$130 per barrel and US$125 per barrel respectively,” he says.

In addition, Heng notes that the US two-year real yield (as measured by the US two-year Treasury nominal yield net of US two-year inflation breakeven) started to fall again after “stabilising” at -2% in early February. “Since then, with the onset of Russia’s invasion of Ukraine, the US two-year real yield has dropped further back to a new low of -2.9%. A further rise in inflation amid soaring energy and commodities prices is likely to result in US real yield falling deeper into negative [territory]. This is supportive of further strength in gold price,” he adds.

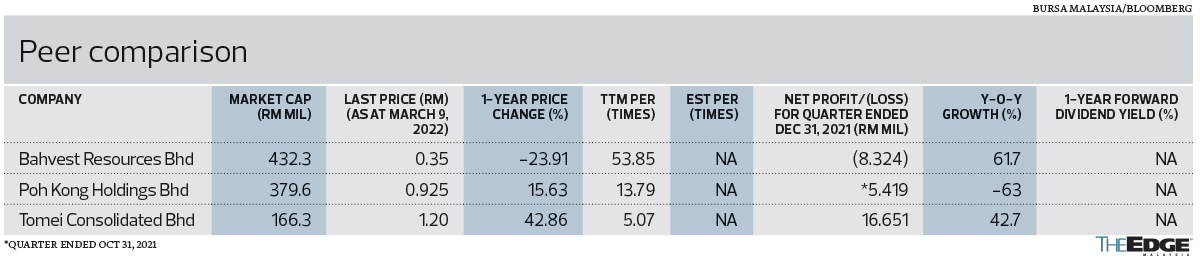

Rakuten Trade head of research Kenny Yee says the Russia-Ukraine conflict is the key factor to determine gold price trends going forward. He sees upstream players such as Bahvest Resources Bhd as direct beneficiaries of higher gold prices.

Bahvest, whose business operation is in gold mining production in a total mining area of 317.7ha in Tawau, Sabah, turned a net profit of RM3.88 million for the cumulative nine months ended Dec 31, 2021 (9MFY2022), compared with a net loss of RM18.42 million a year ago, while revenue rose 53.1% year on year to RM97.29 million from RM63.55 million.

The company said total gold production increased to 400.02kg in 9MFY2022, surpassing the 375.62kg recorded for the whole of FY2021.

However, Yee says the upside will be somewhat limited for downstream players such as Poh Kong Holdings Bhd and Tomei Consolidated Bhd, which are manufacturers cum retailers of jewellery in gold and gemstones.

“Poh Kong and Tomei may benefit slightly from the strong gold price if they have a lot of inventory acquired at lower prices. But if they buy gold at current prices, that could have an impact on their margins,” he tells The Edge. This could be seen in their past quarterly results, which have shown a volatile earnings pattern subject to fluctuations in gold prices.

But it is not just the price of gold that is leaping. Yee points out that commodity prices are also soaring at an accelerated pace in the wake of Russia’s invasion of Ukraine.

The worsening situation in Ukraine also continues to weigh on investors’ sentiment, which is evident from the extension of the recent sell-off in the global equity markets. On Bursa Malaysia, after closing lower at 1,546.87 points on Tuesday, the benchmark FBM KLCI settled at 1,562.33 points on Wednesday — down 0.33% year to date (YTD).

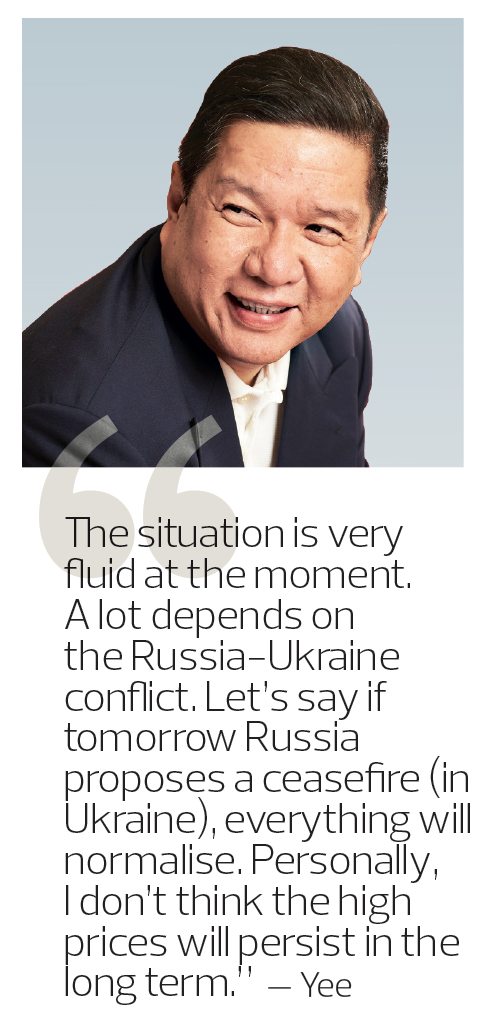

The upward trend in gold prices, however, is unsustainable, says Yee. “The situation is very fluid at the moment. A lot depends on the Russia-Ukraine conflict. Let’s say if tomorrow Russia proposes a ceasefire (in Ukraine), everything will normalise. Personally, I don’t think the high prices will persist in the long term. Maybe gold prices will stay elevated in the short term,” he says.

So, should investors invest in gold-related stocks as a portfolio diversifier and a hedge against inflation? Yee says those looking for exposure to the gold segment may consider gold-backed exchange-traded funds (ETFs).

UOB’s Heng concurs. “It’s important to note that at this stage of the rally, there is elevated uncertainty. While unlikely, a sudden ceasefire between Russia and Ukraine could improve sentiment dramatically and trigger a retreat in gold prices.

“Similarly, a very hawkish outcome at the upcoming US Federal Open Market Committee on March 15 and 16 may trigger a larger-than-expected rise in rates that will weigh on gold as well. Currently, futures have priced in a lower 25 basis points (bps) rate hike from the FOMC, from the 50 bps rate hike expectation prior to the onset of war,” he says.

Heng also says, in line with this latest round of strength in gold price, there has been a clear return of inflows to gold ETFs and funds since early February. “The total global tonnage in gold ETFs rose back above 100 million ounces on Feb 18 and has now added another three million ounces in the interim to 102.8 million ounces. These renewed inflows to gold ETFs are likely the return of safe-haven buying into gold.”

In a February ETF performance report, Bursa Digital Research notes that Affin Hwang Asset Management’s ETF, the Bursa-listed TradePlus Shariah Gold Tracker (GoldETF), continued to lead in terms of traded value during the month, with RM2.4 million traded. It accounted for 28% of total traded value of ETF of RM8.6 million.

On a YTD February 2022 basis, GoldETF was the most actively traded ETF, reversing the lead of fixed income ETF in 2021. GoldETF contributed 35.8% of total traded value and 30.7% of total traded volume YTD, says Bursa Digital Research.

Meanwhile, Bahvest’s share price declined 22.2% YTD and 23.9% over the past one year to close at 35 sen last Wednesday, giving the company a market capitalisation of RM432.3 million. The stock is currently trading at a trailing 12-month price-earnings ratio (PER) of 53.85 times.

Shares in Poh Kong have risen 15.6% YTD and over the past 12 months to settle at 92.5 sen last Wednesday, giving the company a market capitalisation of RM379.6 million. The stock is currently trading at a trailing 12-month PER of 13.79 times.

Poh Kong closed out its financial year ended July 31, 2021 (FY2021) on a positive note, with net profit rising 50.5% to RM36.76 million from RM24.43 million in the previous year, while revenue rose 20.6% y-o-y to RM903.1 million.

However, net profit for the first financial quarter ended Oct 31, 2021 (1QFY2022) fell 63% to RM5.42 million from RM14.64 million a year ago, mainly owing to the lower revenue in the current quarter in review. Revenue for the quarter declined 21% to RM175.29 million from RM221.91 million in 1QFY2021, as its business was only allowed to reopen in stages from Aug 16, 2021.

Smaller listed peer Tomei’s shares have risen 30.4% YTD and 42.9% over the past year to close at RM1.20 last Wednesday, valuing the company at RM166.3 million. The stock is currently trading at a trailing 12-month PER of 5.07 times.

Tomei’s net profit grew 5.1% to RM32.77 million for the financial year ended Dec 31, 2021 (FY2021), from RM31.17 million in FY2020, contributed positively by both its manufacturing and wholesale and retail operating segments. Revenue grew 33.2% to RM736.07 million from RM552.4 million during that period.

Tomei attributed its improved performance to the gradual reopening of the economy since August 2021, which has facilitated the recovery of the group’s business, coupled with the year-end festivities.

All eyes are now on the listing of its manufacturing and wholesale subsidiary YX Precious Metals Bhd (YXPM) on the ACE Market of Bursa. Both Bursa Securities and the Securities Commission Malaysia have approved the listing, subject to certain conditions being met by YXPM.

Renewed risk aversion

Gold demand in 2021 recouped much of the Covid-19-related losses sustained during 2020 except for holdings of gold ETFs, which fell in 2021 in sharp contrast to 2020’s record increase, according to UOB in its Feb 24 report titled “Gold in 2022: Caught Between Rising Rates and Renewed Safe Haven Demand”.

“Gold ETFs had net outflows of 173 tonnes in 2021, mainly concentrated in 1Q, coinciding with risk-on investor appetite as vaccines were rolled out,” it says.

“However, the gradual reopening of the global economy across 2021, coupled with the lower price, lifted jewellery demand to pre-pandemic levels. After a brief rally that saw gold rise above US$1,900 per ounce in 2Q2021, gold pulled back to consolidate around US$1,800 per ounce throughout most of 2H2021.”

UOB observes that gains were fuelled primarily by India and China but decent recovery was also seen across all other regions. Pent-up demand in India from weddings deferred during 2Q2021 and rescheduled for 4Q2021 provided a boost, as did the higher number of auspicious wedding days in 4Q (15 in 4Q2021 versus seven in 4Q2020).

“Gold started 2022 on a strong note, amid escalating geopolitical risk in Ukraine and, at the moment of writing, rallied past the US$1,900 per ounce psychological resistance,” says UOB.

It also notes that since the start of 2022, there has been a strong jump in renewed allocation back into gold ETFs. A reversal in gold price despite the hawkish Fed statement and the manifestation of safe-haven demand amid rising tensions in Ukraine are likely the driving factors behind the strong inflows, it adds.

“Traditionally, gold moves in the opposite direction to interest rates, that is, gold does not like rising interest rates. That seemed to be the case previously. However, since the start of 2022, there has been a strong move higher in gold despite the corresponding rise in 10-year US Treasury yield,” says UOB.

In its latest report, UOB’s Heng says the ongoing rise in energy and commodity prices will be keenly felt in economies across the world in the months ahead as inflation rises further and growth slows down concurrently.

“It is worth noting that future expectations of US Fed rate hiking trajectory remained strong and continued to price in a 150 bps cumulative rise in Fed fund rates by end of this year. But this anticipated rise in rates is no longer the dominant driver against gold price. There is now an increasing fear of stagflation by global investors and safe-haven inflows to gold now take over as a key dominant driver.

“These safe haven inflows can take many forms across the investor spectrum, from individual consumers to institutional funds to global central banks. Specific to individual consumers, prior to Russia’s invasion of Ukraine, there was a clear recovery in physical gold jewellery demand, particularly from India, as economies gradually recovered from the Covid-19 restrictions,” he says.

Taking into consideration the mounting stagflation risk and evidence of more safe-haven inflows to gold across various investor classes, ranging from individual consumers to institutional funds to global central banks, UOB has upgraded its neutral outlook for gold to positive and raised its forecasts from the US$1,900 to US$2,000 per ounce range across this year previously, to US$2,100 per ounce for 2Q2022, US$2,150 per ounce for 3Q2022 and US$2,200 per ounce for 4Q2022 and 1Q2023.

Sean Markowicz, strategist at Schroders’ strategic research group, says gold is often seen as a safe-haven asset and it tends to appreciate in times of economic uncertainty. The risk of stagflation favours inflation hedges such as commodities and gold.

“Last year, the reflation environment favoured investing in risk assets such as equities and commodities, such as raw materials and oil, while gold has suffered. However, if we are on the cusp of a period of stagflation, then a shift in performance leadership may be on the way. In this scenario, equity returns may become more muted while gold and commodities may outperform. This is exactly what has manifested so far in 2022,” he writes in a March 1 Talking Point report.

Markowicz says central banks, however, are stuck between a rock and a hard place. “Hiking interest rates too quickly could send the global economy into recession. But keeping rates low for too long could send inflation spiralling out of control.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.