Artist’s impression of Penang South Islands. (Photo by SRS Consortium)

This article first appeared in The Edge Malaysia Weekly on August 23, 2021 - August 29, 2021

ON Aug 13, Gamuda Bhd’s share price hit a 17-month low of RM2.62, on the back of foreign shareholders selling out of the company.

Foreign shareholding in the construction giant stood at 13% at end-July — down from 19% in May. The last time the foreign shareholding was at such lows was 23 years ago, during the 1997/98 Asian financial crisis.

The fall in Gamuda’s share price seems to have been brought about by delays in the rollout of large infrastructure projects — the Mass Rapid Transit 3 (MRT3) and its land reclamation project in Penang, dubbed Penang South Islands (PSI).

To make things worse, the company did not win a couple of jobs in Australia that it was expected to bag. Also in the mix was the stock’s removal from the MSCI Malaysia Index in May.

In a brief response to emailed questions from The Edge on the company’s outlook, Gamuda deputy managing director Mohammed Rashdan Mohd Yusof says, “We remain optimistic about our growth prospects, with opportunities coming from both domestic and overseas markets.

“We are expecting our performance to pick up, with a healthy order book that is poised to increase by RM5 billion with the commencement of PSI — Island A project. A transformative economic project, we see a considerable multiplier effect that the project will bring about for Penang, especially in the electronic and electrical sector. This adds on to our prospects on the domestic front as we await a decision by the incoming government on the MRT3 project.

“We are also confident of clinching some upcoming tunnelling jobs in Australia. We are actively bidding for a strong multibillion-ringgit pipeline of projects there and will submit a number of bids in the next few months and expect the outcomes of the earlier tender awards by 4Q2021 or 1Q2022.”

Is the selldown overdone?

A source familiar with Gamuda says the selldown of its shares has been extreme. “In two or three months, the foreign shareholding is down six percentage points … that is huge, we have never seen such a reduction,” he says.

Then again, the Bursa Malaysia Construction Index has not been doing well either, falling 15.06% from 188.73 points in mid-April to 160.53 points last Thursday.

Gamuda has diverse business interests. It has a large construction business, a property development arm and toll road operations, which include a 44% stake in publicly traded Lingkaran Trans Kota Holdings Bhd (Litrak), 52% shareholding in Sistem Penyuraian Trafik KL Barat Holdings Sdn Bhd (Sprint), 70% equity interest in Kesas Sdn Bhd and 50% in Projek Smart Holdings Sdn Bhd. The group also undertakes the operations and maintenance of the Sungai Selangor Water Treatment Plant Phase 3, among other businesses.

Despite the prevailing sentiment, several analysts view the company’s prospects positively.

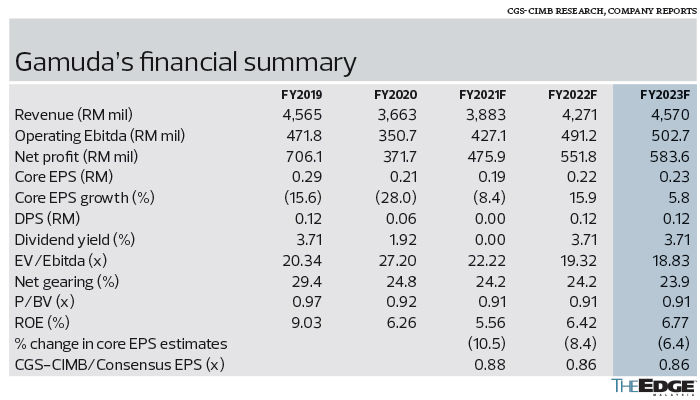

In a June 22 report on Gamuda, CGS-CIMB Securities Sdn Bhd says, “We feel that the 18% year-to-date fall in its share price is unjustified and largely reflects the potential delays to MRT3 and disruptions from the FMCO (Full Movement Control Order).

“Against the backdrop of a potential construction sector recovery in 4QCY2021F, Gamuda is a laggard among the big caps under our coverage. Risk-reward has turned attractive, in our view, on the back of easing political uncertainties, for the rollout of mega contracts.”

CGS-CIMB has a “buy” call on the stock, with a target price of RM4.18, which is close to a 60% premium to the current share price.

In an Aug 13 report that analysed Gamuda from an environmental, social and governance (ESG) perspective, CLSA Securities Malaysia Sdn Bhd pegged a 12-month target price of RM3.80 on the stock, with a “buy” recommendation. “We value Gamuda’s construction division based on 13.5 times sustainable earnings while applying 12 times sustainable earnings for its local property project, with a 40% discount,” it says.

“We used discounted cash flow to value the expressway and water supply operations and maintenance concessions. Our target price for Gamuda is based on an estimated fully diluted revalued net asset value (RNAV) per share.”

However, CLSA was also cautious. “Given its job concentration in large projects, Gamuda is exposed to policy risk. The ability to replenish jobs before the MRT2 civil works are completed is also a concern. A prolonged Covid-19 outbreak could slacken work efficiency,” it adds.

The Edge understands that until the end of last year, the RM30 billion MRT2 project made up the lion’s share of Gamuda’s order book. It is understood that the project is progressing as planned and is on schedule. The first phase of MRT2, which is slated to run from Kwasa Damansara to Kampung Batu Station, is almost completed while the second phase, from Kampung Batu station to Putrajaya Sentral station, will commence operations by January 2023.

Strong balance sheet

Nevertheless, at RM2.62, Gamuda’s share price is less than 75% of its net asset per share of RM3.52 as at end-April. Its net gearing, meanwhile, was a commendable 0.24 times.

AmInvestment Bank, which has a “hold” call on Gamuda with a fair value of RM3.16, forecasts a net profit of RM499 million on the back of RM3.49 billion in revenue for FY2021 ended July 31. CLSA pegs Gamuda’s net profit and revenue at RM511 million and RM3.24 billion respectively, while CGS-CIMB has these at RM531.5 million and RM4.03 billion respectively.

AmInvestment Bank had cut its FY2021F net profit forecast by 12% and reduced its fair value for Gamuda from RM3.49 previously “to reflect the increased risk of its order book (which includes a sizeable self-funded reclamation project). The construction giant’s 9MFY2021 net profit came in below expectations at only 66% and 69% of its full-year forecast and full-year consensus estimate respectively”.

For the nine months ended April, Gamuda chalked up a net profit of RM374.23 million from RM2.63 billion in revenue. This compares with a net profit of RM389.02 million from RM2.74 billion in revenue in the previous corresponding period.

As at end-April, Gamuda had cash and bank balances of RM2.7 billion, long-term debt commitments of RM3.79 billion and short-term borrowings of RM1.8 billion. Shareholders’ funds stood at RM8.8 billion, including reserves of RM5.22 billion.

Good prospects

In the notes that accompany its financial results, Gamuda says, “Ongoing risks to the country’s economic and fiscal outlook posed by the progression of the Covid-19 pandemic and uncertainties surrounding the vaccine drive to counter it have dampened economic activity. Public spending and stimulus for infrastructure development could be constrained due to the rising government fiscal burden.

“It is anticipated that this year’s performance will be driven by overseas property sales, in Vietnam and Singapore, and the continued progress of the MRT Putrajaya Line (formerly called MRT Line 2). Moving forward, the resilience of the group is underpinned by its construction order book of RM4.9 billion and unbilled property sales totalling RM4 billion, which will see it through the next two years. On top of that, the group has a healthy balance sheet, with prudent gearing of below 0.3 times.”

Analysts point out that Gamuda stands a good chance of winning projects in Australia. The company lost out on the A$2.6 billion (RM7.8 billion) Sydney M6 Motorway bid, but it was one of three shortlisted bidders for two tunnelling jobs for the Sydney Metro West project — the 11km Central Tunnelling package from Bays Precinct to Sydney Olympic Park and the 9km Western Tunnelling package from Sydney Olympic Park to Westmead. For these contracts, it partnered with international engineering and construction firm Laing O’Rourke.

For the Central Tunnelling contract, Gamuda and Laing O’Rourke lost out to the joint venture of Acciona Construction Australia Pty Ltd and Ferrovial Construction (Australia) Pty Ltd. However, this means Gamuda and Laing O’Rourke, as well as the other losing bidders of the Central Tunnelling project — John Holland, CPB Contractors and Ghella Australia — will be left to vie for the Western Tunnelling package. These tunnelling packages — Central and Western — are valued at between A$2 billion and A$2.5 billion.

For another job, the Greater Western Sydney-Western Sydney International Airport metro line, Gamuda is partnering with Australian contractor John Holland. This bid is expected to be announced in the first quarter of 2022.

Gamuda managing director Datuk Lin Yun Ling said late last year that the Australian government had chosen to use fiscal stimulus to boost the country’s economic recovery and had earmarked A$100 billion for infrastructure projects, specifically rail-related ones, over the next 10 years. In other words, there is going to be RM30 billion worth of jobs up for grabs every year in Australia over the next decade.

On the MRT3, a construction industry source says, “It is more a question of when the MRT3 will be awarded than if. The HSR (high-speed rail) is on the back burner, and you can’t have another ECRL (East Coast Rail Link). The multiplier effect of construction projects is 2.5 times … so the MRT3 will give the government the best bang for its buck. So, it [MRT3] should be out soon once the Covid-19 situation subsides.”

Gamuda and its partner MMC Corp Bhd have played a key role as the project integrator for the two MRT projects and have undertaken a chunk of the construction work for the RM21 billion MRT1 and RM30 billion MRT2. Thus, it is understandable that the two companies are also the front runners to bag the multibillion-ringgit MRT3 construction project.

In Penang, Gamuda is understood to have obtained all the requisite approvals and looks likely to make good on the PSI reclamation project. The company has 70% equity interest in the turnkey contractor undertaking the reclamation job and 70% in the project developer, ensuring a dual income stream for the group.

PSI basically entails Gamuda reclaiming 1,820ha and constructing three man-made islands: Island A, B and C measuring 930ha, 566ha and 324ha respectively.

The reclamation contract of RM5 billion itself should more than double the group’s existing construction order book. The land sales, meanwhile, is understood to have generated significant interest among many large developers looking to buy parcels off Gamuda to develop them.

“It would be worrying if Gamuda were building houses or condominiums. But in this case, they are just selling large parcels of land, maybe 10 parcels to five buyers,” says the construction industry source.

Also on hold, pending the setting up of the new Cabinet under the incoming prime minister, is Gamuda’s plan for a highway trust, which is understood to have excited former works minister Datuk Seri Fadillah Yusof. The broad plan entails the elimination of compensation from the government for not allowing toll rate hikes and involves the tolled roads being run by a non-profit entity.

In April, Fadillah said the government was looking at a highway trust proposal by Gamuda, where the concession period is extended without any tariff hikes. He also said another highway operator, Prolintas, a unit of Permodalan Nasional Bhd, had approached the government for a restructuring exercise.

In mid-July, when asked whether there were any updates on the restructuring of the highway concessionaires, Fadillah said in a brief WhatsApp message, “No decision yet. Will let you know once a decision is made at Cabinet level.”

Gamuda’s share price has since rebounded from the 17-month low. Closing at RM2.80 last Thursday, the company was valued at RM7.04 billion, which puts its largest shareholder the Employees Provident Fund’s 14.63% stake at slightly more than RM1 billion.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Sapura Energy bags multiple contracts worth nearly RM100 mil

- Anwar, Xi witness exchange of 31 MOUs and documents to advance Malaysia-China cooperation

- Bina Puri announces boardroom changes, founder director Tan Cheng Kiat retires

- King confident Malaysia, China will continue to empower cooperation

- Bank Rakyat flags challenging 2025, keeps 17% dividend for FY2024

- Putrajaya orders temporary closure of KL Tower, says past concessionaire's stay 'unlawful'

- Meta saw TikTok as ‘highly urgent’ threat, Zuckerberg says at antitrust trial

- Sapura Industrial, Gas Malaysia, CapitaLand, Hextar Technologies, Golden Land, Skyworld, Sapura Energy, Bina Puri, Paragon Globe, OCK Group, Nextgreen, Nexgram

- Ivory Properties aborts land disposal deal with Chin Hin following liquidation of subsidiary

- Tesla slumps below 50% share of California’s electric car market