KUALA LUMPUR (Aug 22): Fitch Solutions Country Risk and Industry Research anticipates the current downward trend in crude palm oil (CPO) prices to continue in the next four years to a low of RM2,600 per tonne in 2026.

The research outfit expects the edible oil prices to decline 23.1% year-on-year to RM4,000 per tonne next year. It reasons that the effects of one-off events that occurred in the first half of 2022 — the Russia-Ukraine conflict and the Indonesian palm oil export ban — are to ease further.

Its assessment is that CPO prices are to continue their downturn to an average palm oil price of RM3,033 per tonne between 2024 and 2026 in view of consistent annual surpluses set to weigh on prices. It forecasts annual average palm oil prices of RM3,500 per tonne for 2024, RM3,000 per tonne for 2025 and RM2,600 per tonne for 2026, according to a note it issued on Monday (Aug 22).

It noted that this forecast is founded on its palm oil production and consumption forecasts, which foresee the global palm oil market to generate an annual production surplus from 2022 to 2026 — rising from 2.5 million tonnes in 2022 and 2023, to 3.9 million tonnes in 2026. It noted that this is still below the record high surplus of 4.5 million tonnes generated in 2017 and 2018.

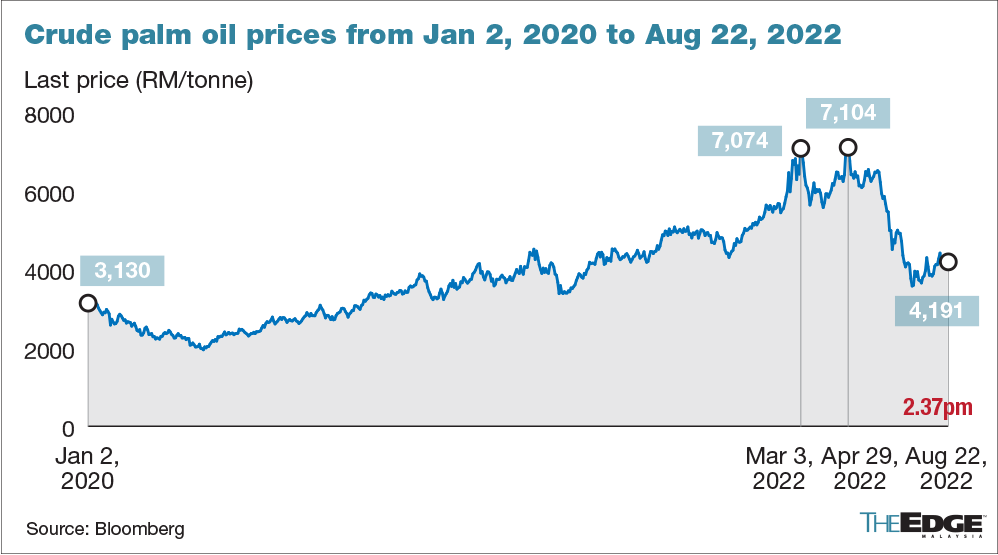

Fitch Solutions noted that palm oil prices touched RM7,074 per tonne on March 3, following the Russian invasion of Ukraine in February this year, while it climbed to a height of RM7,104 per tonne on April 29 — a day after the Indonesian government implemented its ban on the export of palm oil.

“We do not see a return to the historically elevated price levels evident in 1HFY22 (first half of 2022), in no small part as we do not expect Indonesia to reintroduce its short-lived palm oil ban of 2Q2022 (second quarter of 2022).

“We also highlight the loosening of the aggregate vegetable oils market more generally as indicative of less acute upward price pressure in the rest of 3Q2022 and during 4Q2022,” it added.

Over the next five-year period, Fitch Solutions forecasts a production compound annual growth rate (CAGR) of 3.9%, led amongst the largest producers by Nigeria (CAGR of 5%), Colombia (4.8%), and Indonesia (4.3%). As for the demand, it foresees a consumption CAGR of 3.6%, led by mainland China (CAGR of 9.6%) where it predicted that per capita palm oil consumption will rise from 3.49kg (in 2021 and 2022) to 4.98kg (in 2025 and 2026).

“Overall, we see global palm oil production and consumption increasing from 76.6 million to 89.3 million tonnes (up 12.7 million tonnes) and from 74.1 million to 85.4 million tonnes (up 11.3 million tonnes) by the end of our forecast horizon,” it added.

On the potential risks to its forecast, Fitch Solutions noted that there is a short-term downside risk for palm oil prices to diminish further in view that the Indonesian government could strengthen its efforts to accelerate export sales, which would in turn prompt a price depression in the market.

It said this could be an action the Indonesian government may take as the nation’s large accumulated palm oil inventories have yet to start to decline, which indicates that palm oil demand may be weaker than expected through the remainder of 2022.

Fitch Solution pegs the average CPO prices in the next four months to decline to RM4,750 per tonne for the rest of 2022.

The research house noted that this is in line with its unchanged annual average palm oil price forecast of RM5,200 per tonne for 2022.

Meanwhile, a potential long-term upside risk to these forecasts is Indonesia and Malaysia’s “eventual” transformation from reliance on extensive production growth to intensive, yield-driven growth.

“The increasing prominence of sustainability concerns, both inside the major producing nations (Indonesia and Malaysia) as well as in consuming nations, and the increasing scarcity of available land into which to expand palm oil production further will necessitate a fundamental shift in industry strategy to one focused on intensive, yield- and investment-driven growth.

“The extent to which this transformation is achieved will determine, to a large extent, future output growth and so progress that is slower than expected will weigh on output and pose an upside price risk,” the research house explained.