This article first appeared in City & Country, The Edge Malaysia Weekly on June 6, 2022 - June 12, 2022

Sentment in the Greater KL property market has generally improved during the first quarter of the year, says Savills Malaysia associate director, research and consultancy Fong Kean Hwa in presenting the 1Q2022 The Edge | Savills Klang Valley High-Rise Residential Property Monitor.

“Many developers have reported encouraging take-up rates for their ongoing projects, especially for landed properties and some high-rise residential properties in KL and Selangor. We have also observed that more recent projects that were delayed since 2020 are coming to market,” he says.

With the absence of the Home Ownership Campaign this year, Fong observes that developers continued to drive sales by offering new deals and financing options.

As for subsale properties, he says the secondary market remained weak in the quarter under review. “The current buyer’s market is still favoured by investors/upgraders seeking value-buy units for long-term capital appreciation.”

Meanwhile, he notes that the short-term market may be uncertain, but the outlook for the overall residential market remains positive as sentiment improves. “Market activity is expected to strengthen as we enter the endemic phase [of Covid-19]. Supporting factors, in our view, are mainly the continued low borrowing rates (despite the small rate hike), and the willingness of banks to approve loans. Long-term positive trends such as high urbanisation, strong loan growth and steadying house prices will continue to drive the residential market.”

Says Fong, the economic outlook for Malaysia in 2022 is expected to be more optimistic as most indicators, such as gross domestic product (GDP), business confidence index and consumer confidence index, show improvements. “Malaysia’s GDP increased by 3.1% in 2021, and Bank Negara Malaysia forecasts GDP to expand between 5.3% and 6.3% in 2022.”

Household and business financing are also expected to continue to support economic activities due to the low overnight policy rate and improved labour market, he says. “However, downside risks remain due to developments surrounding Covid-19, geopolitical conflicts and rising cost prices.”

Referring to the latest National Property Information Centre (Napic) report, Fong says the property market performance improved slightly in 2021, but remained below pre-2020 levels.

“The country recorded 300,947 transactions worth RM144.87 billion in 2021, a 1.5% increase in transaction volume and a 21.7% increase in value compared with 2020.

“The residential sector led the overall property market activity in the country, contributing 66.2% of the transaction volume in 2021, with 198,812 transactions worth RM76.9 billion. Market activity in Kuala Lumpur and Selangor grew by 4.9% and 10.7% year on year, respectively,” he says.

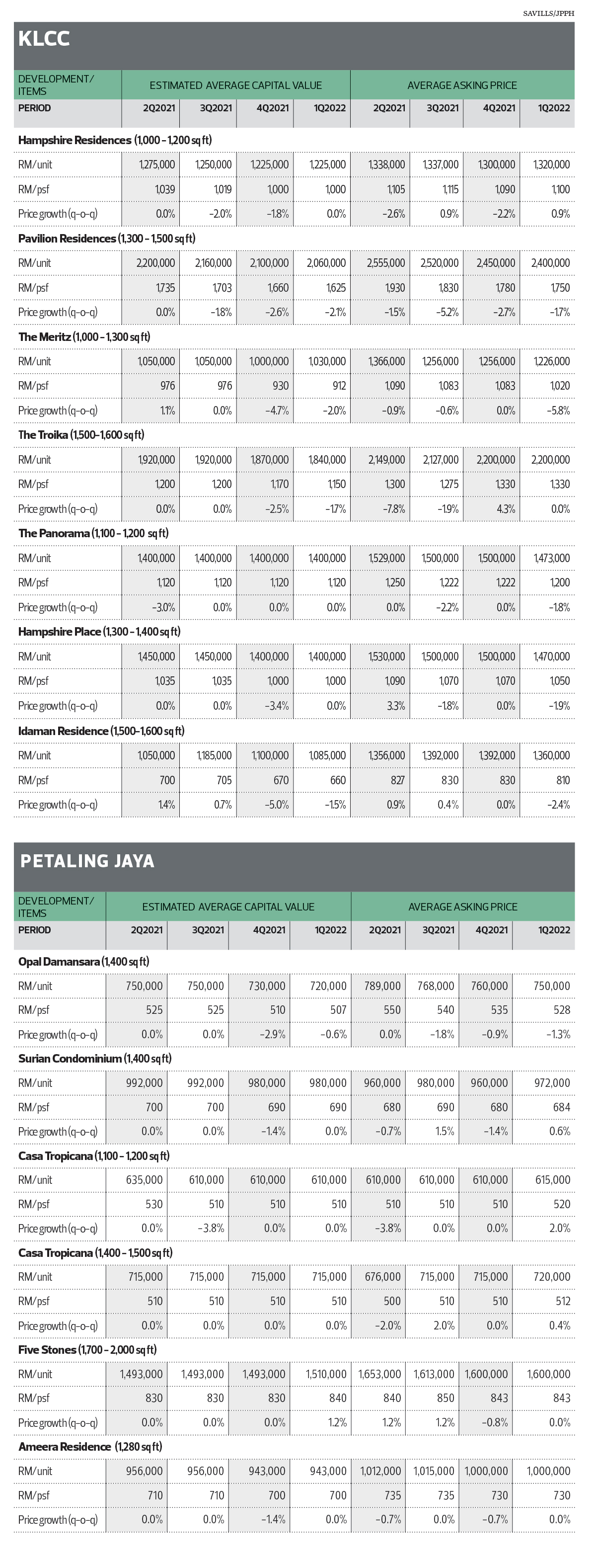

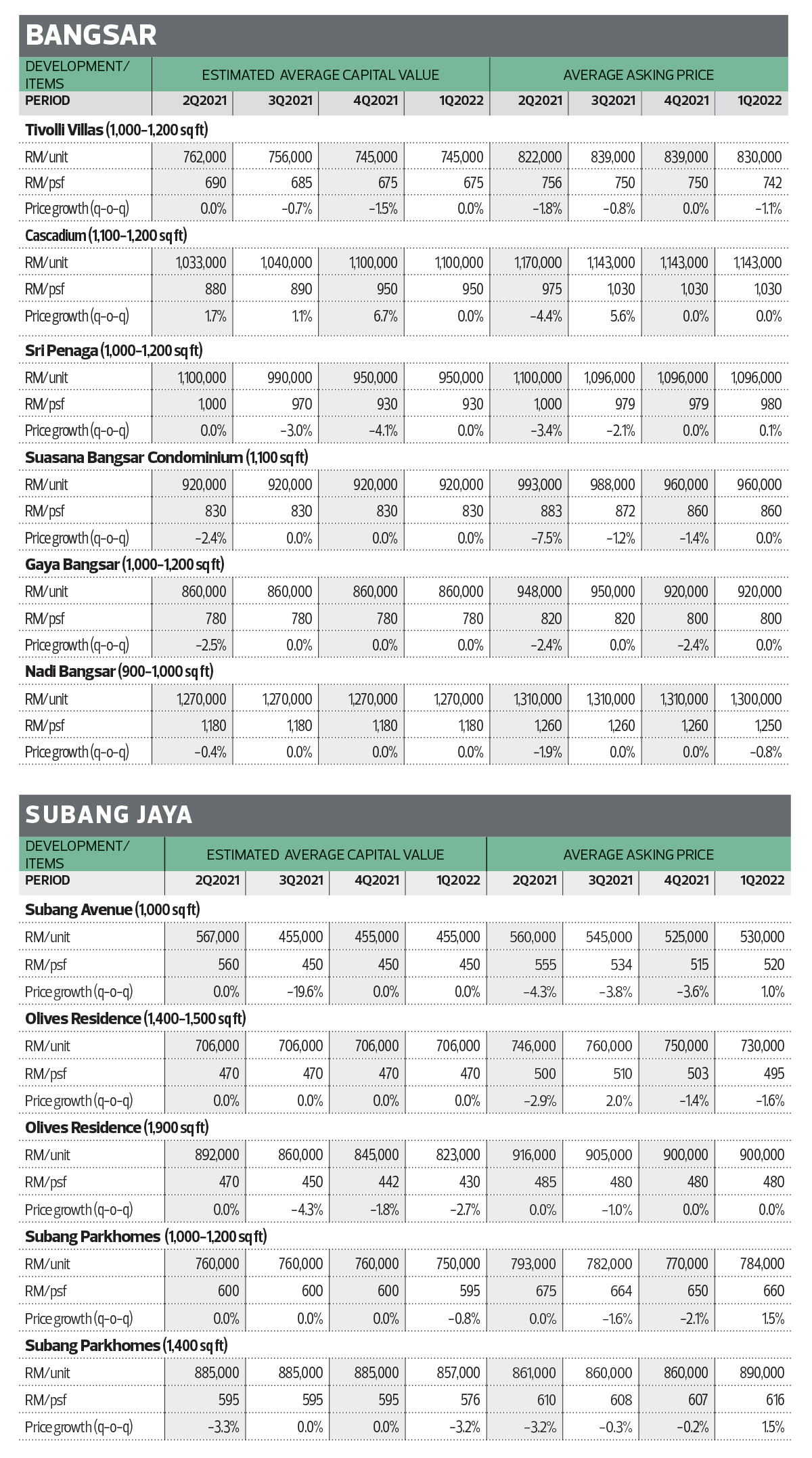

Small price movements in KLCC and Mont’Kiara; unchanged for Bangsar

The average capital value of the sampled 2-bedroom units in KLCC and Mont’Kiara saw a small change during the quarter under review, whereas similar units in Bangsar remained unchanged from the previous quarter.

According to Fong, the price gap between capital value and asking price in KLCC narrowed during the quarter under review at 11%. This was followed by Mont’Kiara at 10% and Bangsar at 6%.

In KLCC, the average capital value of the sampled units averaged RM1,067 psf during the review period, declining by 4.5% year on year (y-o-y) and 1.1% quarter on quarter (q-o-q).

The asking prices for similar types of 2-bedroom units in KLCC declined 5.4% y-o-y and 1.7% q-o-q.

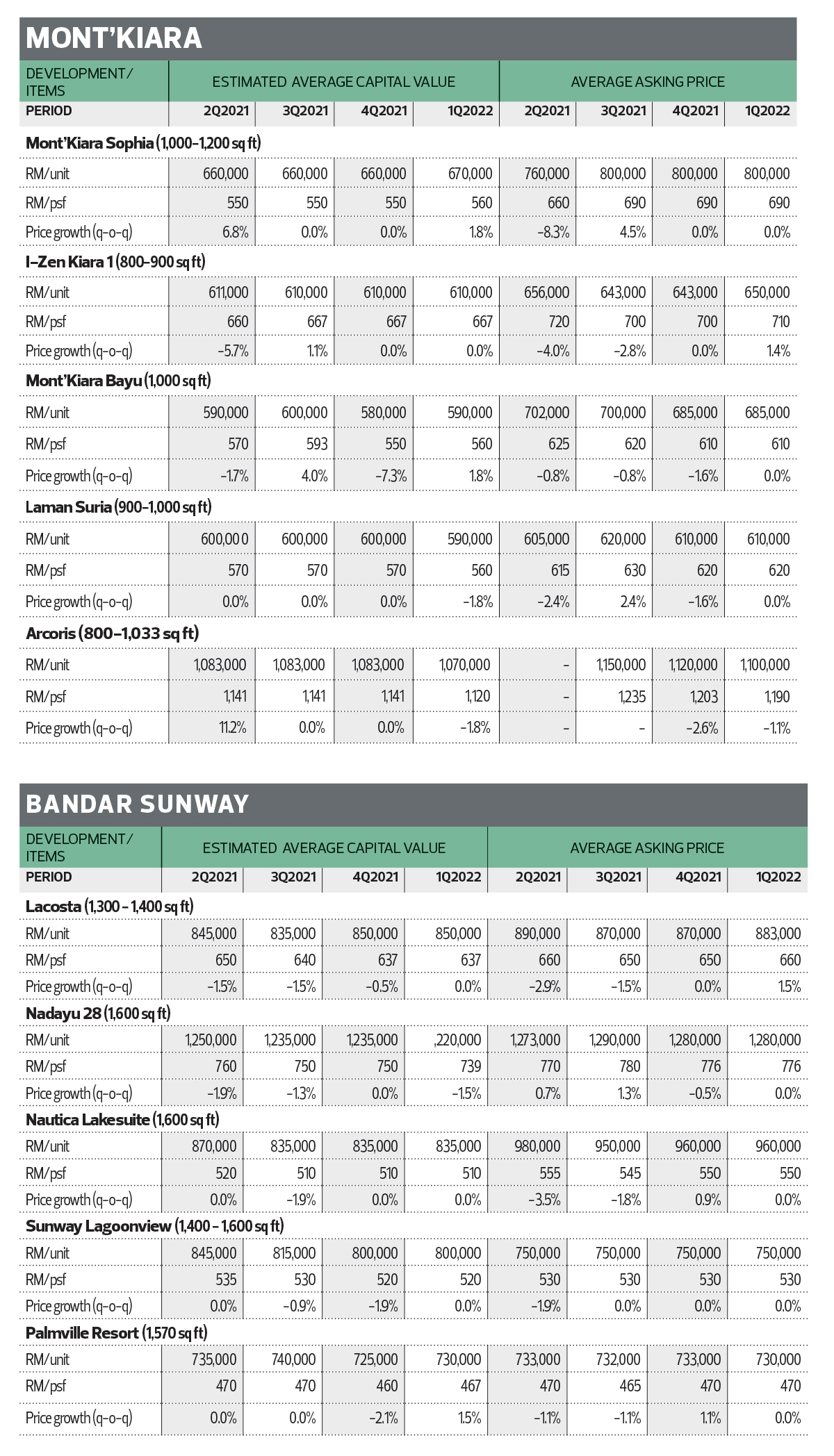

In Mont’Kiara, the average capital value for the sampled units was relatively stable in 1Q2022, compared with the previous quarter registering a small change, dropping 0.3%. On a y-o-y basis, the average capital value increased by 2.2% to RM693 psf.

“Asking prices in Mont’Kiara have remained soft since last quarter. However, the overall Mont’Kiara market is still relatively active compared with KLCC and Bangsar,” says Fong.

Ongoing projects in Mont’Kiara include Allevia Mont’Kiara and Residensi Astrea, both by UEM Sunrise Bhd. The former is offering units ranging from 1,700 to 2,600 sq ft and priced between RM800 and RM900 psf, whereas the latter is offering units ranging from 1,364 to 1,859 sq ft, priced from RM850 psf. Allevia Mont’Kiara and Residensi Astrea are slated to be completed by 2025 and 2022 respectively.

In Bangsar, the average capital value of the sampled units remained unchanged from the previous quarter at RM891 psf. Prices have, however, marginally declined by 0.8% y-o-y.

The average asking price for similar 2-bedroom units in Bangsar also dipped by 4.1% y-o-y to about RM944 psf in 1Q2022.

Ongoing projects in Bangsar include One Eleven Menerung by BRDB Developments Sdn Bhd, Alfa Bangsar by City Motors Group, Residensi 38 by UDA Holdings Bhd and Bangsar Hill Park by Bangsar Hill Park Development Sdn Bhd.

Launched in February, One Eleven Menerung is a high-end freehold project offering 111 units in a 23-storey apartment next to One Menerung. The units will come in built-ups ranging from 1,001 to 3,714 sq ft, priced from RM1.8 million or RM1,800 psf.

As for Alfa Bangsar, the freehold serviced apartment located in Jalan Maarof is offering 178 units ranging from 570 to 997 sq ft at prices from RM963,000 to RM1.68 million. This project is targeted to be completed in 3Q2024.

The leasehold Residensi 38 project is offering units of 580 to 1,442 sq ft at around RM1,070 psf. The project is scheduled to be completed by 2Q2024.

The Bangsar Hill Park development, which is also leasehold, is offering units ranging from 917 to 1,478 sq ft at prices from RM845 to RM1,000 psf. The project has a 2025 completion date.

Average prices remain unchanged in Bandar Sunway, Petaling Jaya; decline in Subang Jaya

Compared with the previous quarter, the average capital value of the sampled 2- and 3-bedroom units in Bandar Sunway and Petaling Jaya remained unchanged in 1Q2022, whereas Subang Jaya’s capital value registered a drop.

The price gap between the capital value and asking price remained at 2% for Petaling Jaya. In contrast, the price gaps in Bandar Sunway and Subang Jaya have slightly widened at 4% and 10% respectively, notes Fong.

In Subang Jaya, the average capital value of the sampled units declined by 6.5% y-o-y and 1.4% q-o-q to RM504 psf during the review period. According to Fong, this was mainly caused by the larger units at Olive Residence and Subang Parkhomes.

However, the asking price in Subang Jaya increased to RM554 psf in 1Q2022 from RM551 psf in the last quarter.

“While we expect the subsale market in Subang Jaya to remain challenging in the near term, we notice that there is increasing buying interest in this area,” says Fong. He explains that Subang Jaya’s selling points are always its freehold status and location with ample amenities, including the rail transport system.

Ongoing projects in Subang Jaya include Aurora @ Subang Jaya City Centre (SJCC) by Sime Darby Property Bhd; Dorsett Waterfront Subang by Malaysia Land Properties Sdn Bhd (Mayland); Southplace Residences @ Tropicana Metropark by Tropicana Corp Bhd; and Alira @ Metropark (Phase 1) by MCT Bhd.

Prices of the new projects are RM600 to RM700 psf at Alira @ Metropark (Phase 1); RM740 psf at Aurora @ SJCC; RM780 psf at Southplace Residences @ Tropicana Metropark; and RM800 psf at Dorsett Waterfront Subang.

In Bandar Sunway, the average capital value of the sampled properties was stable during the quarter under review, but recorded a drop by 2.9% y-o-y.

“Although the subsale market in this area is still inactive, the asking prices have stabilised during the reviewed quarter,” notes Fong.

An ongoing project in Bandar Sunway is Union Suites by Symphony Life Bhd.

In Petaling Jaya, the average capital value of the sampled units remained unchanged q-o-q, but registered a decline by 1.3% on a y-o-y basis.

“We observe a similar trend for asking prices,” says Fong. “The price gap between the capital value and asking price remains narrow, indicating a buyers’ market in this amenity-rich location.”

Ongoing projects in Petaling Jaya include Tropicana Miyu by Tropicana Temokin Sdn Bhd in Seksyen 17; Megah Rise by PPB Properties in Taman Megah (SS24); The Mate by OCR Group Bhd at Damansara Jaya;

D’Cosmos Residences by Exsim Group in Damansara Perdana; and Ruby Seapark Residences by Midas De Sdn Bhd in Sea Park.

Additionally, there are three ongoing projects in Kelana Jaya, namely, The Arcuz by Exsim Group; Sunway Serene by Sunway Property and Panorama Residences by LLC Properties Sdn Bhd.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.