This article first appeared in The Edge Malaysia Weekly on December 27, 2021 - January 2, 2022

AT US$117.2 trillion (RM492.2 trillion), global stocks are off their all-time high but still worth some US$14 trillion more than the US$103 trillion at which they ended 2020. Malaysia-listed stocks, unfortunately, were worth about RM100 billion (US$42.6 billion) less this year at RM1.64 trillion on Dec 21 — wiping out last year’s gains.

So, winner selection was not as tough this year, with the bellwether FBM KLCI down 127 points year on year to just above 1,500 points at the time of writing and likely to end near its lowest level in at least a decade.

Only 71 recommendations for 58 stocks came in from 16 research outfits for the 16th edition of The Edge’s Best Call Awards, noticeably lower than last year’s record high of 131 recommendations for 90 stocks from 19 research houses. None came in for glove stocks this year.

Started in 2005 (we skipped one year but brought them back by popular demand), the awards are our best-effort attempt to recognise good fundamental stock analysis and its importance in the making of informed investment decisions. They are not meant to influence year-end appraisals or annual bonuses. Feedback is welcomed at bestcalls@bizedge.com.

Here are this year’s winners — selected based on submissions and publicly available data — in no particular order. Incidentally, eight of this year’s 12 winners are past winners — five won last year. Congratulations to all winners. To the unsung stellar stock pickers, keep up the good work. Have a restful festive season to power up for (what we hope will be a strong rebound) next year. Merry Christmas and Happy New Year 2022!

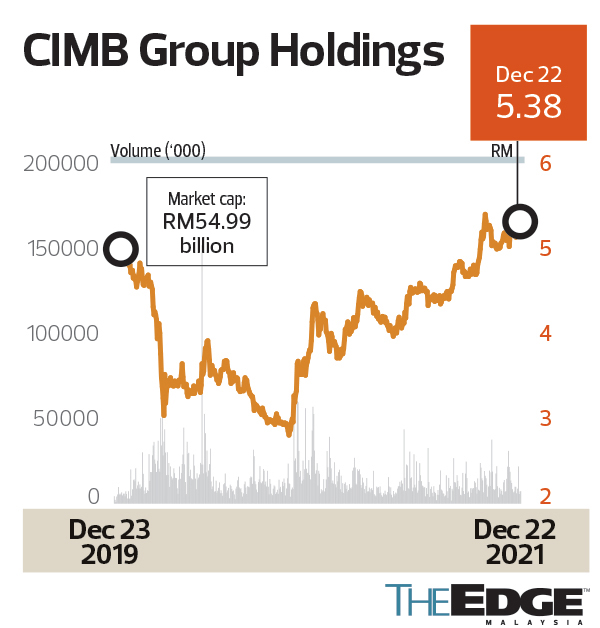

Credit Suisse head of research Danny Goh’s call on CIMB Group Holdings Bhd

When Credit Suisse’s Danny Goh raised his rating of CIMB Group Holdings Bhd to “outperform” from “underperform” on Nov 19, 2020, his RM4.50 target price implied 21% upside potential. At the time, consensus was overwhelmingly bearish on CIMB, with 15 “hold” and four “sell” recommendations. Two other analysts already had “buy” recommendations, but those had been maintained for at least six months — during which CIMB’s stock price skidded instead of rose. The upgrade was also reasonably near CIMB’s two-year low of RM2.81 on Nov 2 last year.

The upgrade was based on expectations of a recovery in 2022 return on equity (ROE) to 7.9% versus 3.5% in 2020 and 6.2% in 2021. “While the stock could face some near-term asset quality headwinds and earnings weakness, we believe that the risk-reward proposition looks more attractive as favourable vaccine development news improves the prospects of ROE recovery to pre-Covid levels,” Goh wrote in a 33-page banking sector report.

By Dec 1, his target price had been raised from RM6 to RM7.05 — the highest among 22 tracking CIMB, Bloomberg data shows. While the stock has eased from its recent high of RM5.41 on Oct 20 to RM5.38 on Dec 22, upside potential is 31% if he continues to be proved right.

UOB Kay Hian Research analysts Chloe Tan Jie Ying and Desmond Chong’s call on Optimax Holdings Bhd

Tan and Chong seem to have foresight in their coverage on Optimax, an eye specialist centre that is listed on the ACE Market.

They have recommended buying the stock since initiating coverage when Optimax sold shares at 30 sen apiece at IPO. Their target price was 72 sen then.

Their bullish view, however, was put to the test as the company announced a big earnings contraction 10 days after it was listed on Aug 18, 2020. It posted a net profit of RM60,000 for the second quarter ended June 30, 2020, versus RM2.5 million a year earlier. Nevertheless, the duo kept Optimax on their recommendation list, believing in an earnings recovery.

They were proven right. The company’s earnings bounced back in the second half of the financial year ended Dec 31, 2020 (FY2020), with an annual net profit of RM5.64 million, albeit lower. And that lifted the share price to an all-time high of RM1.76 in March.

The company achieved 145% growth in net profit to RM8.72 million in the nine-month period ended Sept 30, 2021.

UOB Kay Hian is the only house actively tracking the stock, according to Bloomberg data. It currently has a “buy” call, with a target price of RM1.60.

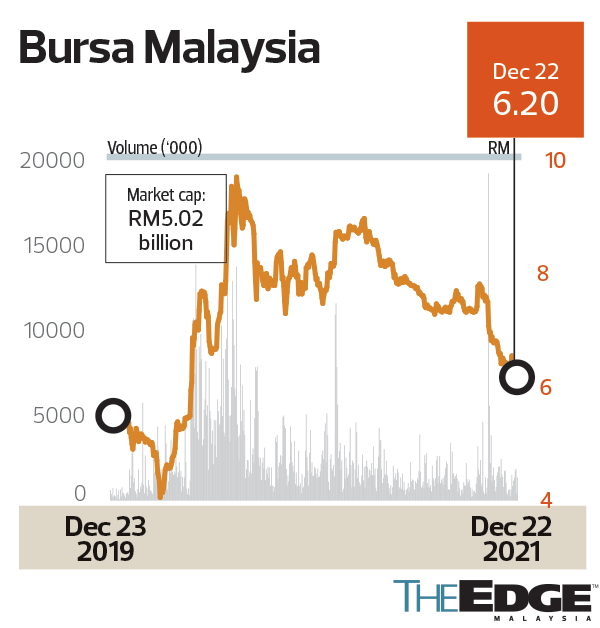

UOB Kay Hian Research analyst Keith Wee’s call on Bursa Malaysia Bhd

After a euphoric year in 2020, when trading volume hit a record high of 27.8 billion shares, it is not surprising that most would have thought the same might repeat this year when the government imposed the Full Movement Control Order (MCO) amid the resurgence of Covid-19 cases. And that would mean another bumper profit year for Bursa Malaysia.

However, the market excitement was not as great, suffice to say. The recovery theme play lost steam and the glove stocks fell out of favour as daily new Covid-19 cases breached the 10,000 level and hit 24,000 cases in August.

Wee noticed the changing tide and made a “sell” call on Bursa Malaysia’s shares in July — the first such recommendation among analysts tracked by Bloomberg. The “sell” call came after an earlier downgrade to “hold” from “buy” in February.

“We expect the stock to register three consecutive years of earnings contraction from 2021 to 2023 as ADV (average daily volume) is expected to continue normalising downwards off a high base,” Wee wrote in his July 14 report.

Since Wee’s downgrades, Bursa’s share price has been on a decline since April, from the RM9 level to a low of RM6.18.

Maybank Investment Bank Research analyst Wong Wei Sum’s call on Eco World Development Group Bhd

Most investors who bought Eco World Development Group Bhd shares between much of 2014 and 2020 would likely have had strong words for analysts who recommended a “buy”. In 2021, Maybank Investment Bank’s Wong Wei Sum was among property analysts who saw a turn in the tide early and grabbed the chance to wipe the slate clean on the beaten-down stock when upgrading the property sector to a “contrarian buy”.

Clients who picked up Eco World, which has a “hands-on and creative management team”, around 45 sen apiece when Wong upgraded the stock to a “buy” from a “hold” on Dec 14, 2020, would have benefitted, as Eco World shares surged 178% to as high as RM1.25 on Oct 28 this year. Gains were still 88.88% when measured from the upgrade to Dec 22’s 85 sen close.

With her 93 sen target price breached, Wong rightly told clients to “take profits off the table” as she cut her call to a “sell” on Nov 1, near the stock’s peak. With Eco World slipping 29% from as high as RM1.10 on Oct 28 to 85 sen on Dec 8, Wong raised the stock to a “hold”. Eco World closed at 85 sen on Dec 22.

The downgrade on Eco World was part of what she calls “a contrarian tactical negative” view on the property sector. Noting that “the recovery theme is now overplayed”, she flagged headwinds from a potential interest rate hike and political uncertainties ahead of the 15th General Election.

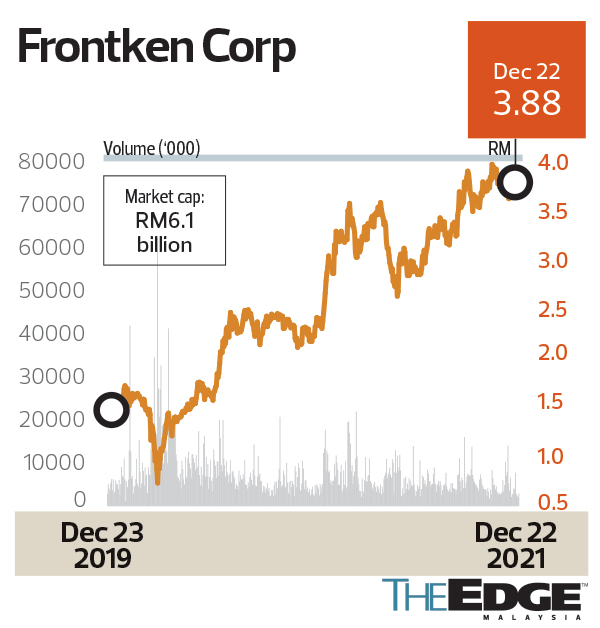

Hong Leong Investment Bank Research analyst Tan J Young’s call on Frontken Corp Bhd

At its peak of RM4.05 on Nov 8, shares in Frontken Corp Bhd were up 73% year to date (YTD) and were only 10 sen shy of Hong Leong Investment Bank Research’s Tan J Young’s price target of RM4.15, which had just been raised from RM3.88 on Nov 4 after strong 3QFY2021 results.

Closing at RM3.88 on Dec 22, the stock was still up 66% YTD, more than the 57% gained last year. It surged 229.5% in 2019, the year Tan’s call on Frontken was also named among the winners of The Edge Best Call Awards.

Investors familiar with his recommendation and who followed it would have already pocketed just over 800% in total return in just over three years (averaging 92% a year) if they bought in August 2018, when Tan started coverage with a “buy”. Total return would double to 1,600% (averaging 90% a year) if counted from his “non-rated” call in July 2017 when the share price was only 33 sen, Bloomberg data shows.

Whether he scores a hat-trick should be interesting, with the current RM4.15 target price pegged at 50 times FY2023 earnings. In his latest update note, dated Nov 4, Tan said he liked Frontken for its unique exposure to leading-edge semiconductor fronted supply chain, multi-year growth ahead on the back of sustainable global semiconductor market outlook, robust fab investment, leading-edge technology (below seven nanometre) and strong robust balance sheet (RM282 million net cash, or 18 sen per share) to support its Taiwan expansion.

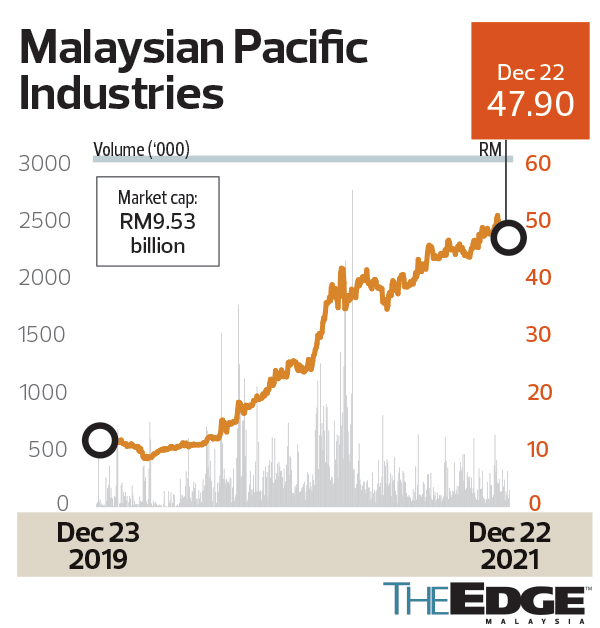

TA Research analyst Wilson Loo Jia Chern’s call on Malaysian Pacific Industries Bhd

Wilson Loo was not the one who unearthed this gem. MPI was already a darling among investors in the early 2000s amid the dotcom boom. In the current semiconductor boom that started in 2020 and gathered steam in 2021, Loo was one of many with resounding “buy” calls, but he was the first to raise the target price for MPI above the RM50 mark. He upgraded the stock to “buy” from “hold” in late November last year when it was hovering at RM25.

On March 2, when the share price was at a new height of RM41.70, he pegged a target price of RM54.35 from RM48.60. The share price exceeded RM50 briefly in early December.

MPI, which provides turnkey packaging and test services to chip makers, remains a favoured choice as a proxy to ride the semiconductor boom. The counter has been a “screaming buy” amid expectation of continued strong global chip demand fuelled by the chip shortage in the near term and the rising number of smart gadgets, be it a floor sweeper robot or an electric vehicle, in the long term.

It is worth noting that Samuel Tan Kai Bin of Kenanga Investment Bank and Mohd Shanaz Noor Azam of CGS-CIMB Research, who have been the “genuine MPI bulls”, have not downgraded their “buy” calls since April last year, when the stock was barely RM10.

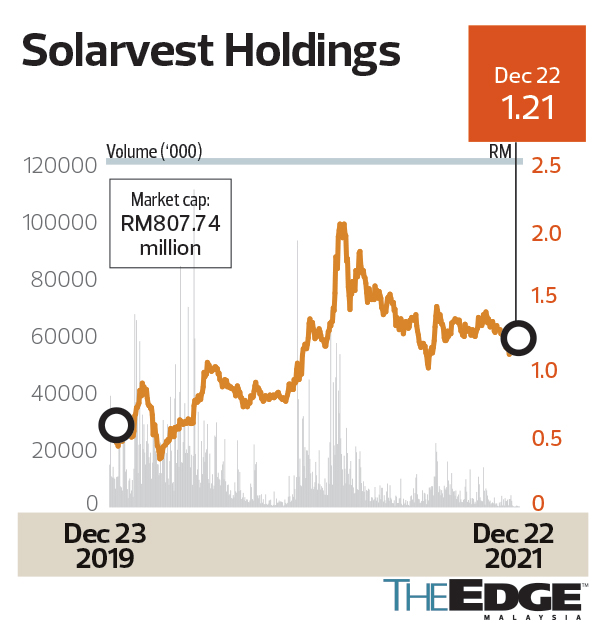

RHB Research analysts Lee Meng Horng and Loo Tungwye’s call on Solarvest Holdings Bhd

Crunching numbers is not the most difficult part of an analyst’s job; the main challenge is making a timely “sell” call when the share price is rallying, and vice versa when the price slumps.

Lee and Loo initiated coverage on Solarvest in September 2020 when the share price was 87.5 sen, given the growing interest in renewable energy companies. Besides being a contractor that builds solar photovoltaic (PV) energy generating facilities, Solarvest is building its own solar farms to cultivate recurring income streams in Manjung, Perak, and Kuala Selangor.

The stock soared to a record high of RM2.07 in February. Soon after, they told clients to take profit after the rally.

“We subsequently downgraded our call to ‘take profit’ on Feb 15, as we believed the valuation had more than priced in the positive outcome of the LSS4 (large scale solar 4) tender, even under a blue sky scenario,” the duo wrote in their submission to The Edge. They revised their call to “neutral” after a 21% drop in the share price roughly two weeks later, on Feb 26.

Those who have followed their recommendations since September should be a happy lot as Solarvest reversed its uptrend and headed to a low of RM1.02 in July. Meanwhile, investors holding onto the stock would have enjoyed bonus issues of shares and warrants.

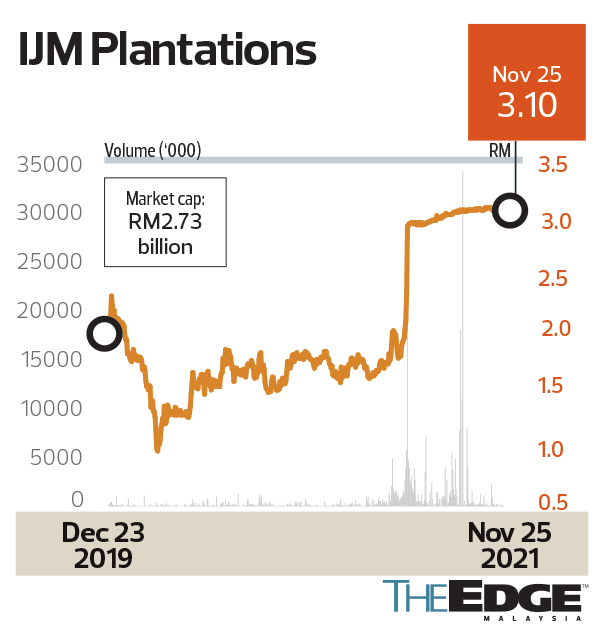

Hong Leong Investment Bank Research analyst Chye Wen Fei’s call on IJM Plantations Bhd

Crude palm oil prices leapt above the RM3,000 level in January amid the unexpected commodity boom. However, most plantation analysts were hesitant to recommend oil palm planters listed on Bursa, although these companies had delivered stellar earnings.

The cautious consensus views were due mainly to the increasing awareness of ESG compliance. Like it or not, plantation companies have always been associated with deforestation.

However, Chye made a bold move in recommending that her clients buy IJM Plantations shares when the stock was trading at the RM1.80 level in January this year.

Those who bought the plantation counter should be happy simply because the share price soared to RM3.10 — a return of 72%, or RM1.30 per share. The return would be even higher if one had bought shares in early February, when the stock hit a low of RM1.58.

We agree with the analyst who pointed out in her submission that while the outperformance of the counter was very much due to the takeover offer made by Kuala Lumpur Kepong Bhd in June, “credit should be given to those who had the courage to upgrade the stock when sentiment on the sector was lukewarm, at best”.

RHB Research’s veteran plantation analyst Hoe Lee Leng is another contrarian who recommended the stock. She upgraded the counter in late February.

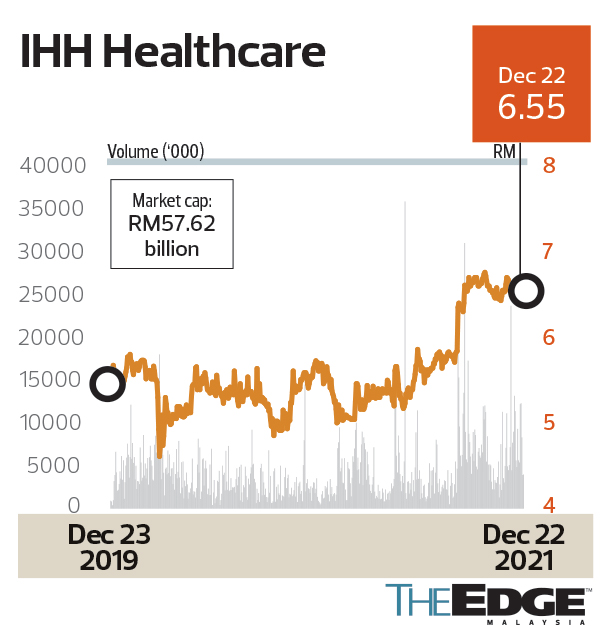

Kenanga Investment Bank Research analyst Raymond Choo Ping Khoon’s call on IHH Healthcare Bhd

When Kenanga Investment Bank Research’s Raymond Choo upgraded his recommendation on IHH Healthcare Bhd to “outperform” on March 1 this year, he was the last of more than 20 analysts to have a “buy” call. The upgrade was significant precisely because Choo had kept an “underperform” call on IHH against a “buy” consensus for more than two years.

Investors closely tracking IHH would know the fact that the stock is up by one-fifth YTD signified a reversal in its share price trajectory — before 2021, IHH last saw double-digit y-o-y stock price gains in 2015. When upgrading IHH and lifting his target price from RM4.56 to RM5.85 on March 1, Choo noted that IHH’s operations in India and Turkey (Acibadem) had returned to the black after several quarters in the red. Helped by the easing of travel and local movement restrictions, revenue and earnings rebounded. The group also further deleveraged its non-lira debt in its Turkish operations from €288 million at end-2019 to €37 million as at end-2020. From RM5.46, IHH rose 24% to close as high as RM6.76 on Oct 14 this year and was still hovering at RM6.55 on Dec 22. Even at RM6.55, investors who bought on Choo’s upgrade would be sitting on a 24% total return — not too shabby for a big cap stock such as IHH. Choo had since Nov 23 downgraded IHH to a “market perform” or a “neutral”, with an unchanged target price of RM6.65.

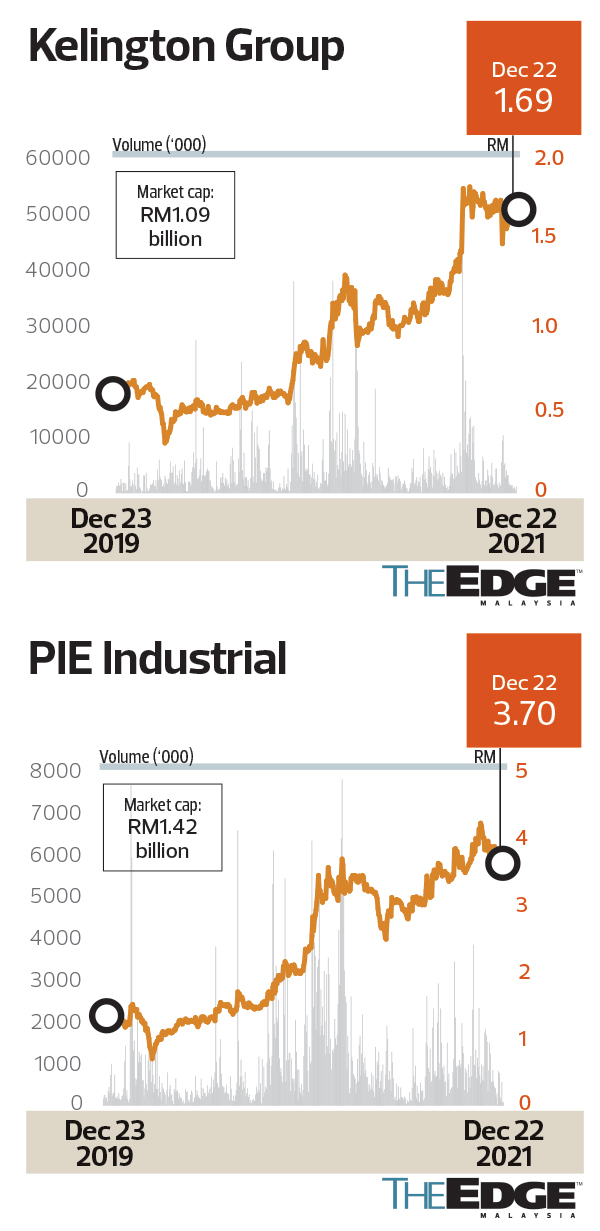

Kenanga Investment Bank Research analyst Samuel Tan Kai Bin’s call on Kelington Group Bhd and PIE Industrial Bhd

Kenanga Investment Bank Research’s Samuel Tan Kai Bin was not the earliest to initiate coverage on Kelington Group Bhd, a beneficiary of the ongoing semiconductor wafer fab expansion. Yet, investors who bought the stock when Tan started coverage on it with an “outperform” call on Nov 9, 2020, would have seen its share price triple within 11 months from 65 sen to as high as RM1.83 on Sept 29, 2021.

At the time, Tan’s 96 sen target price was significantly higher than that of the other two analysts, who had “neutral” recommendations and target prices of 57 sen and 61 sen respectively, according to Bloomberg data. The bullishness proved right as Kelington’s share price surged 38% over three weeks from 65.4 sen to above 90 sen on Nov 30, 2020. According to Tan’s submission, investors who tracked Kenanga’s call since the initiation date would have gained 235% when factoring in its 1:1 bonus issue in June 2021 and 1:3 free warrants in July 2021. Total return was 156% between Nov 9, 2020 and Dec 22, 2021, according to Bloomberg data.

Tan’s target price has since Sept 15 been revised from RM1.50 to RM2.50, the highest among five analysts covering the stock, according to Bloomberg data. If Tan is right, there is 48% upside potential from Kelington’s RM1.69 close on Dec 22.

Recognising PIE Industrial Bhd as a hidden gem in the electronics manufacturing services (EMS) space, Tan upgraded his recommendation to “outperform” on Jan 8 this year, with a RM3.30 target price, as the stock fetched RM2.61 on the open market. The upgrade followed positive feedback from PIE’s management, premised on stronger prospects from a new customer. At the time, the only other coverage had a RM1.98 target price and “neutral” call, Bloomberg data shows.

After 4QFY2020 earnings came in above expectations, Tan raised his target price to RM4 on March 1 and highlighted the possibility of a new key customer bringing more business that would enable PIE’s earnings to stay healthy. His target price was raised further to RM4.30 on Nov 22, following the release of strong 3QFY2021 numbers. Telling clients that PIE was “emerging as the go-to EMS solutions provider”, Tan said the group could choose jobs that contributed to its margins because it had spent years honing its capabilities.

Investors who bought PIE shares on Jan 8 would have enjoyed more than 60% gains in just 10 months, as the stock rose as high as RM4.22 on Nov 11. While the stock price has since eased 12% to close at RM3.70 on Dec 22, investors are unlikely to brush off PIE, simply because it is 51.42%-owned by Taiwan’s Pan International Industrial Corp, which is in turn 27.3%-owned by iPhone-maker Foxconn, or Hon Hai Precision Industry Co Ltd (the world’s biggest EMS player). Tan’s RM4.30 target price implies 16.2% upside potential.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Tan Kean Soon steps down as T7 Global executive deputy chairman, board says no operational impact

- Huawei posts surprise loss after aggressive tech research

- Perak emerges as Malaysia's No 1 sweet corn producer

- China's Xi to visit Malaysia in April, SCMP reports

- Thai watchdog had flagged concerns over building that collapsed in earthquake, Reuters told