This article first appeared in City & Country, The Edge Malaysia Weekly on September 26, 2022 - October 2, 2022

The Klang Valley housing market remained slow in the second quarter of this year, but demand has picked up, says Savills associate director of research and consultancy Fong Kean Hwa when presenting The Edge | Savills Klang Valley High-Rise Residential Property Monitor for 2Q2022.

“House prices in the subsale market continued to consolidate during the quarter in review. We observed an uptick in transaction activity in key markets such as Mont’Kiara as homebuyers and investors looked for bargains. We also saw opportunistic buying in places such as Kuala Lumpur city centre (KLCC), Bangsar and Petaling Jaya,” he adds.

Fong observes that first-time homebuyers still favour new projects, as reflected in the sales performance of new launches. “Most recent developments are high-density and offer compact units up to four bedrooms under 1,000 sq ft. Consequently, developers can keep selling prices competitive, targeting small families and young couples.”

Meanwhile, the completion of ongoing projects has remained constrained due to construction delays. “We expect new completions to be pushed to 2023. In the meantime, developers are offering rebates/incentives to offload the unsold units in these projects,” he says.

Fong adds that market challenges remain, due to rising interest rates and inflation. “While the current overnight policy rate remains benign for those not overborrowing, rising interest rates will continue to reduce homebuyers’ borrowing capacity. Slower demand coupled with impending supply and continued pressure on the cost of living will slow house price growth.

“We expect the short-term property market to remain on a sideways trend, awaiting more incentives. The recent stimulus announced by the government was the i-Miliki, which enables first-time homebuyers to enjoy a 100% stamp duty exemption for loan agreements and MOT (memorandum of transfer) for property priced below RM500,000 as well as a 50% discount for property priced above RM500,000 and up to RM1 million. This incentive’s effective date will be from June 1, 2022, until the end of 2023.”

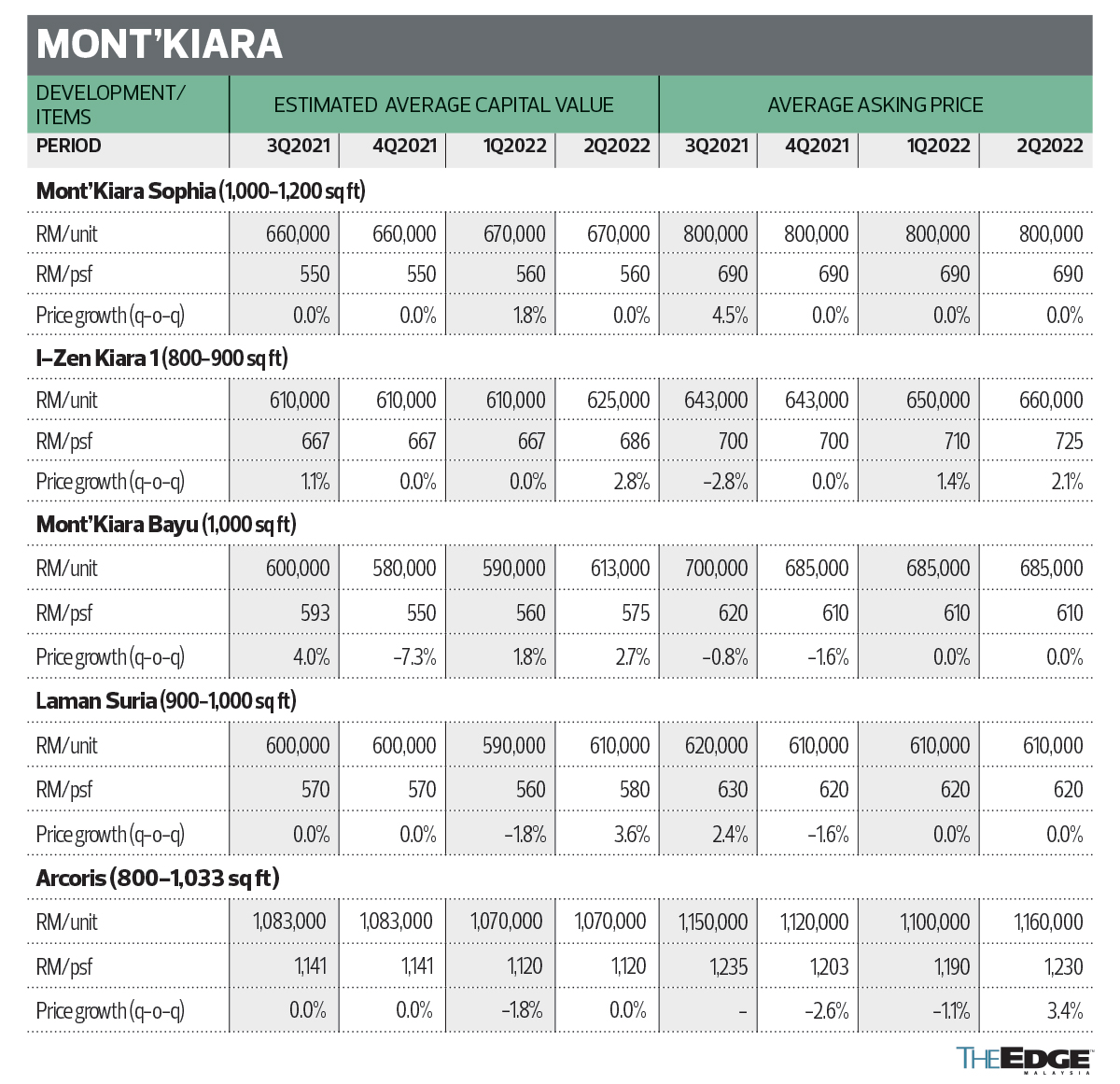

In Kuala Lumpur, Fong observed positive changes to capital values in terms of ringgit psf during the quarter in review for selected 2-bedroom units sampled in Bangsar and Mont’Kiara, with a quarter-on-quarter (q-o-q) growth of 0.3% and 1.6% respectively. On a year-on-year (y-o-y) basis, capital values in Bangsar remained stagnant while those in Mont’Kiara inched up by 0.9%.

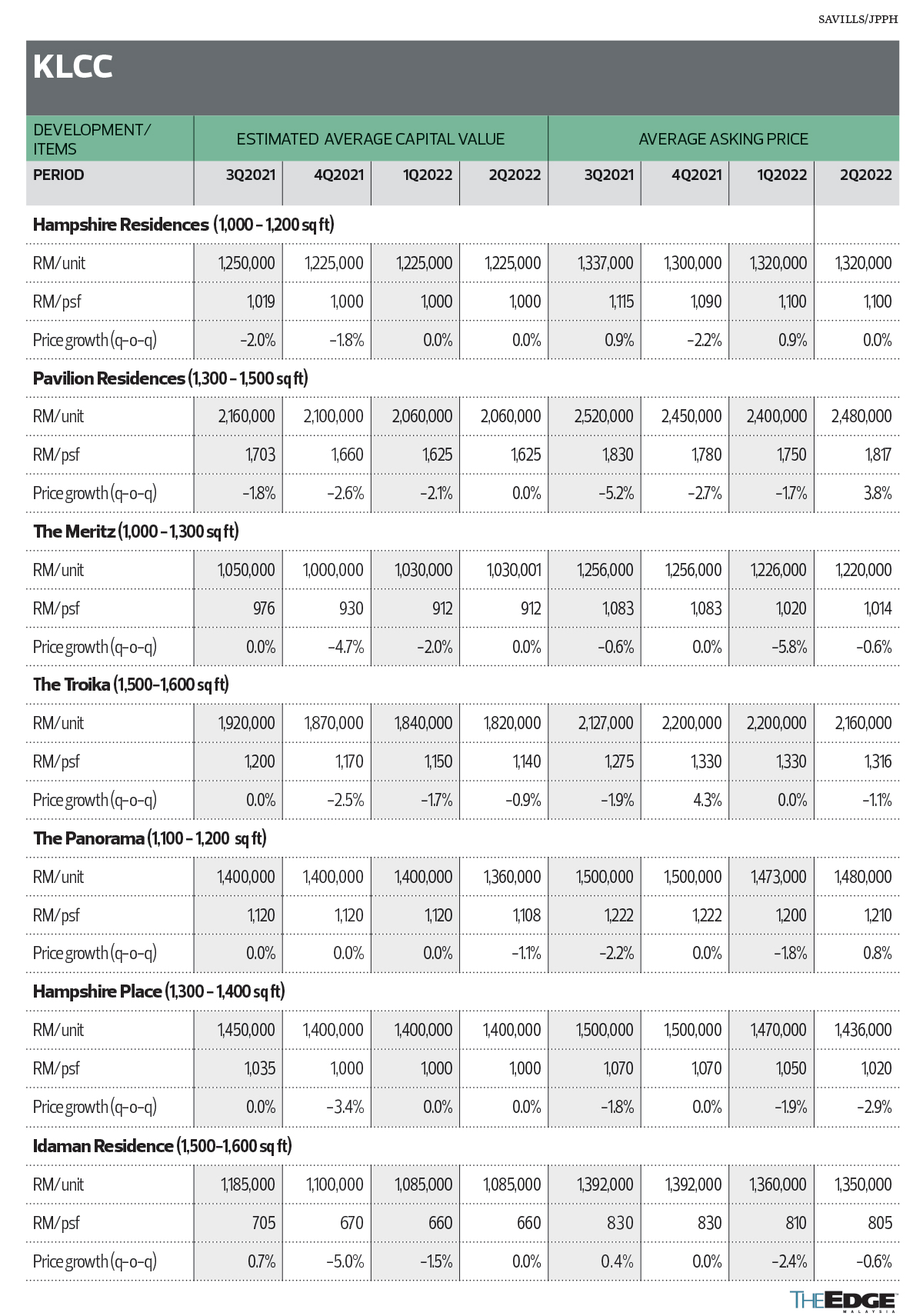

On the other hand, KLCC continued to face headwinds, he says, with capital values declining 0.3% q-o-q and 4.6% y-o-y.

The average price gap between capital values and asking prices in KLCC and Bangsar narrowed to 11% and 6% respectively during the quarter, whereas in Mont’Kiara the price gap remained at 10%.

In Selangor, the average capital value psf of the sampled 2- and 3-bedroom units remained relatively stable in 2Q2022 compared with the previous quarter.

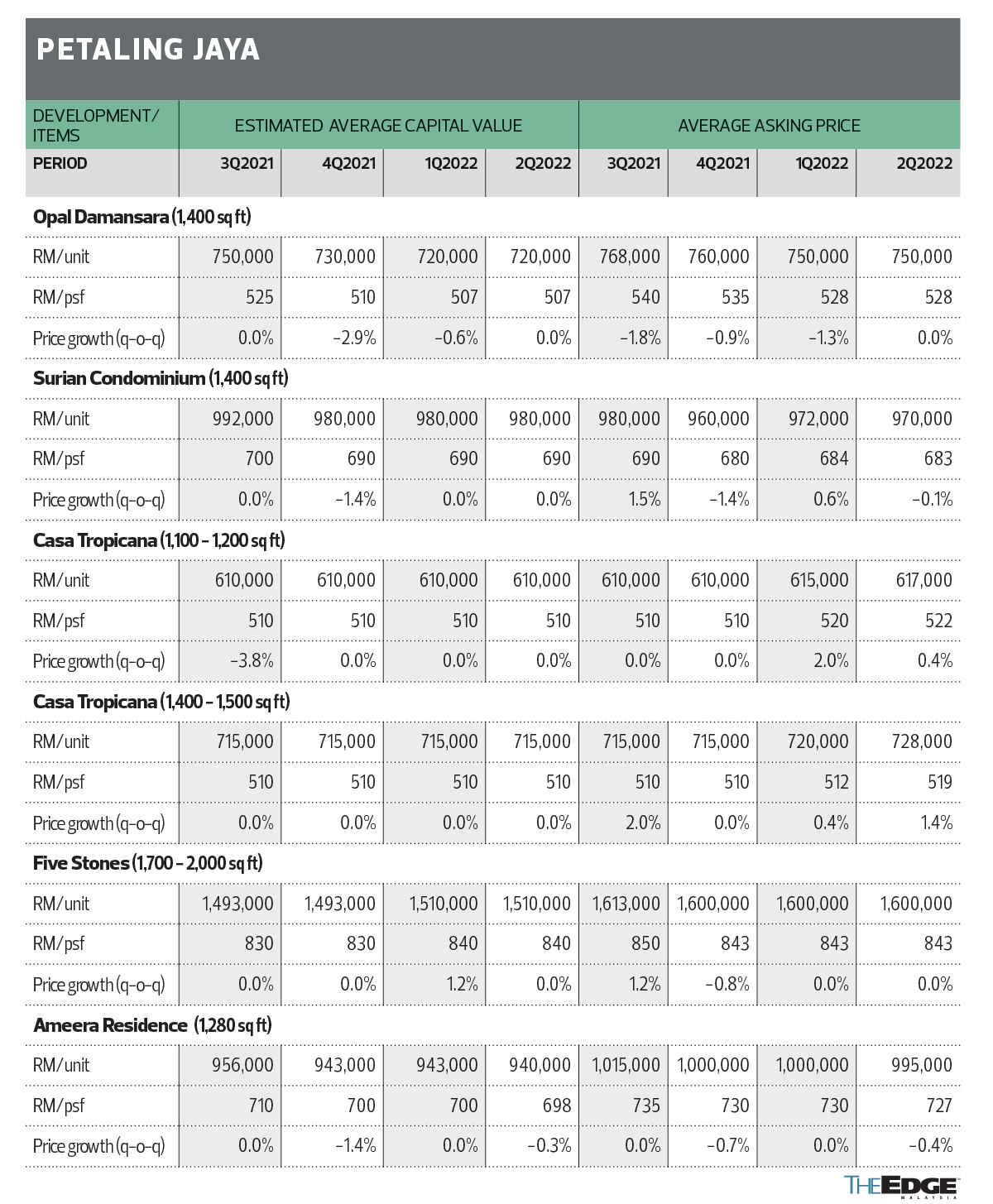

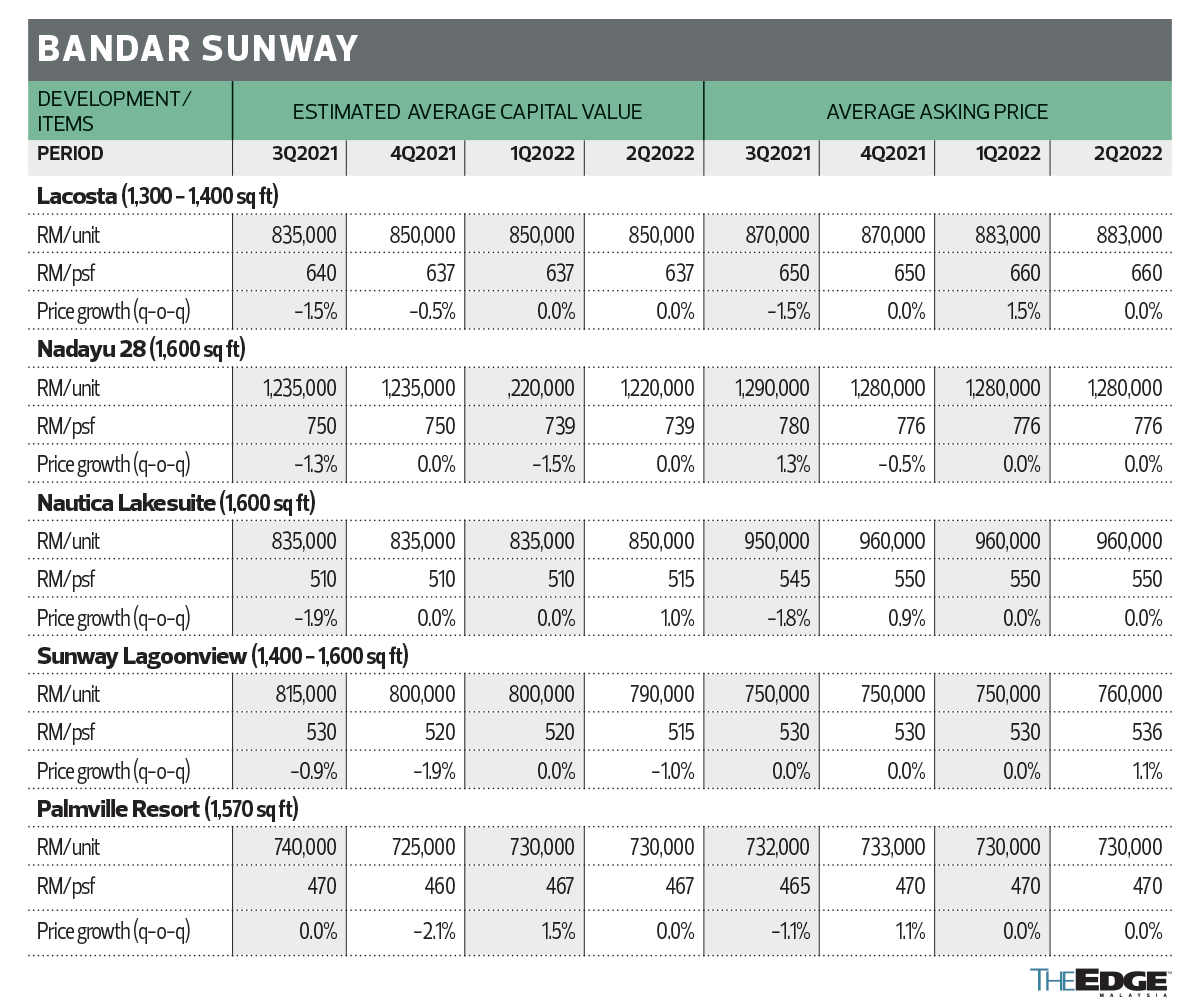

Asking prices of the sampled properties stayed relatively firm, and the average price gap between capital values and asking prices remained at 2% in Petaling Jaya and 4% in Bandar Sunway. In contrast, Subang Jaya had a slightly wider price gap of 9%, says Fong.

Some positive changes in Kuala Lumpur

In the KLCC market, the capital values of sampled properties averaged RM1,064 psf in 2Q2022, declining 0.3% q-o-q and 4.6% y-o-y. The asking price of 2-bedroom units fell 3.6% y-o-y and 0.3% q-o-q, indicating that the subsale market in the KLCC area remained challenging.

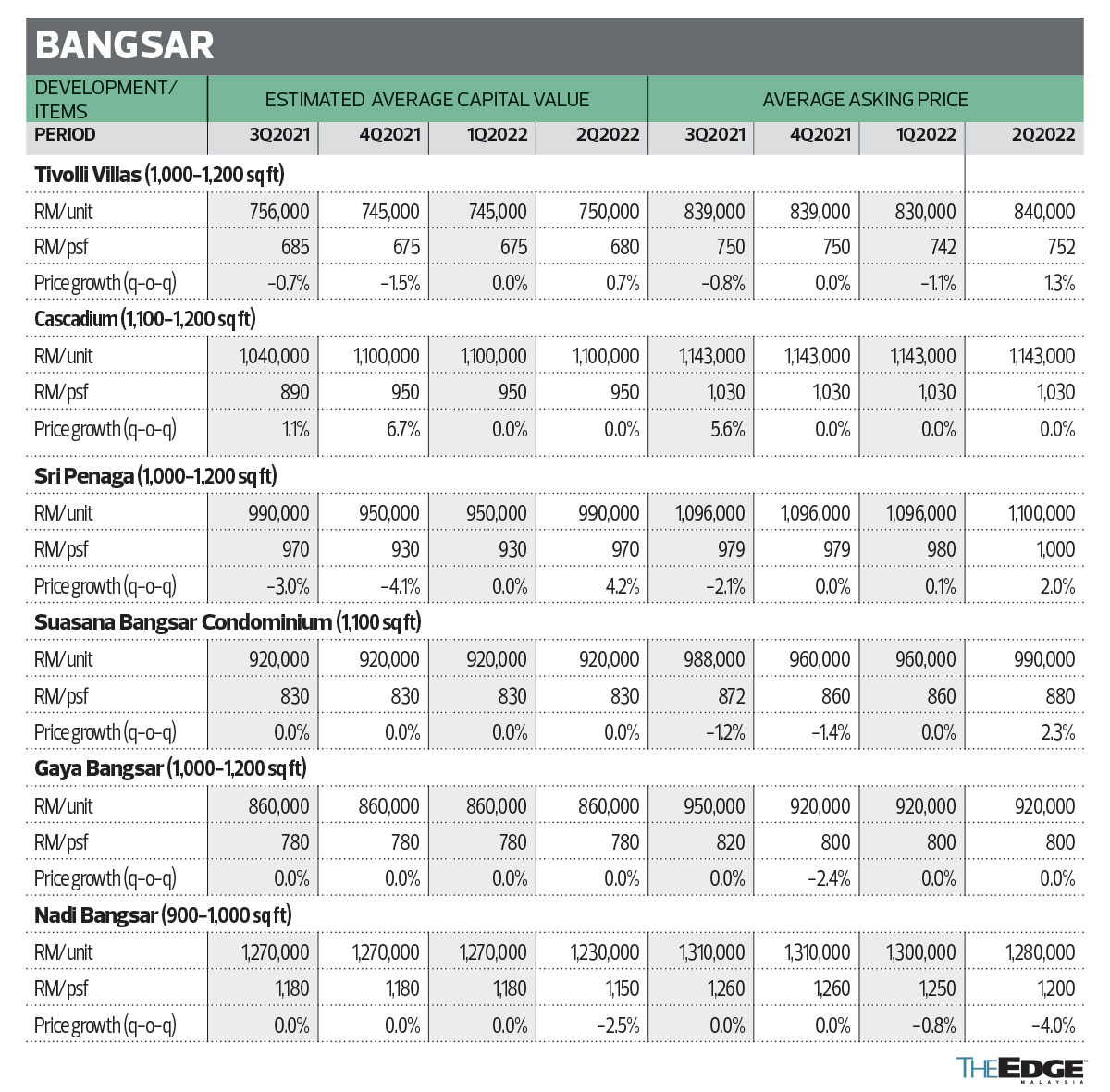

In Bangsar, capital values grew 0.3% q-o-q on average to RM893 psf during the period in review and remained relatively stable compared with the previous quarter. Similarly, the average asking price remained unchanged q-o-q at RM944 psf.

Ongoing projects in Bangsar are Residensi 38 by UDA Holdings Bhd, Bangsar Hill Park by Bangsar Hill Park Development Sdn Bhd, One Eleven Menerung by BRDB Developments Sdn Bhd and Alfa Bangsar by City Motors Group.

Residensi 38 Bangsar is a leasehold development that is slated for completion in 2Q2024. Priced at about RM1,070 psf, the units will have built-ups of 580 to 1,442 sq ft.

Also a leasehold project, Bangsar Hill Park will offer units with built-ups of 917 to 1,478 sq ft and priced at RM845 to RM1,000 psf. The project is scheduled for completion in 2025.

One Eleven Menerung is a freehold development. The 23-storey apartment block is situated next to One Menerung and will comprise 111 units, with built-ups ranging from 1,001 to 3,714 sq ft and priced from RM1,800 psf, or RM1.8 million.

As for Alfa Bangsar, the freehold serviced apartment project will comprise 178 units, with built-ups ranging from 570 to 997 sq ft and prices from RM963,000 to RM1.684 million. The project is slated for completion in 3Q2024.

In Mont’Kiara, the average capital value of the sampled units edged up 1.6% q-o-q during the period in review to RM704 psf. According to Fong, market activity saw an improvement in 2Q2022 with more transactions concluded.

Ongoing projects in Mont’Kiara include Allevia and Residensi Astrea, both developed by UEM Sunrise Bhd. To be completed this year, the latter will offer units with built-ups of 1,364 to 1,859 sq ft and prices from RM850 psf. The former, which will be completed in 2025, will have units ranging from 1,700 to 2,600 sq ft and priced from RM800 to RM900 psf.

Capital values in Selangor remain mostly subdued

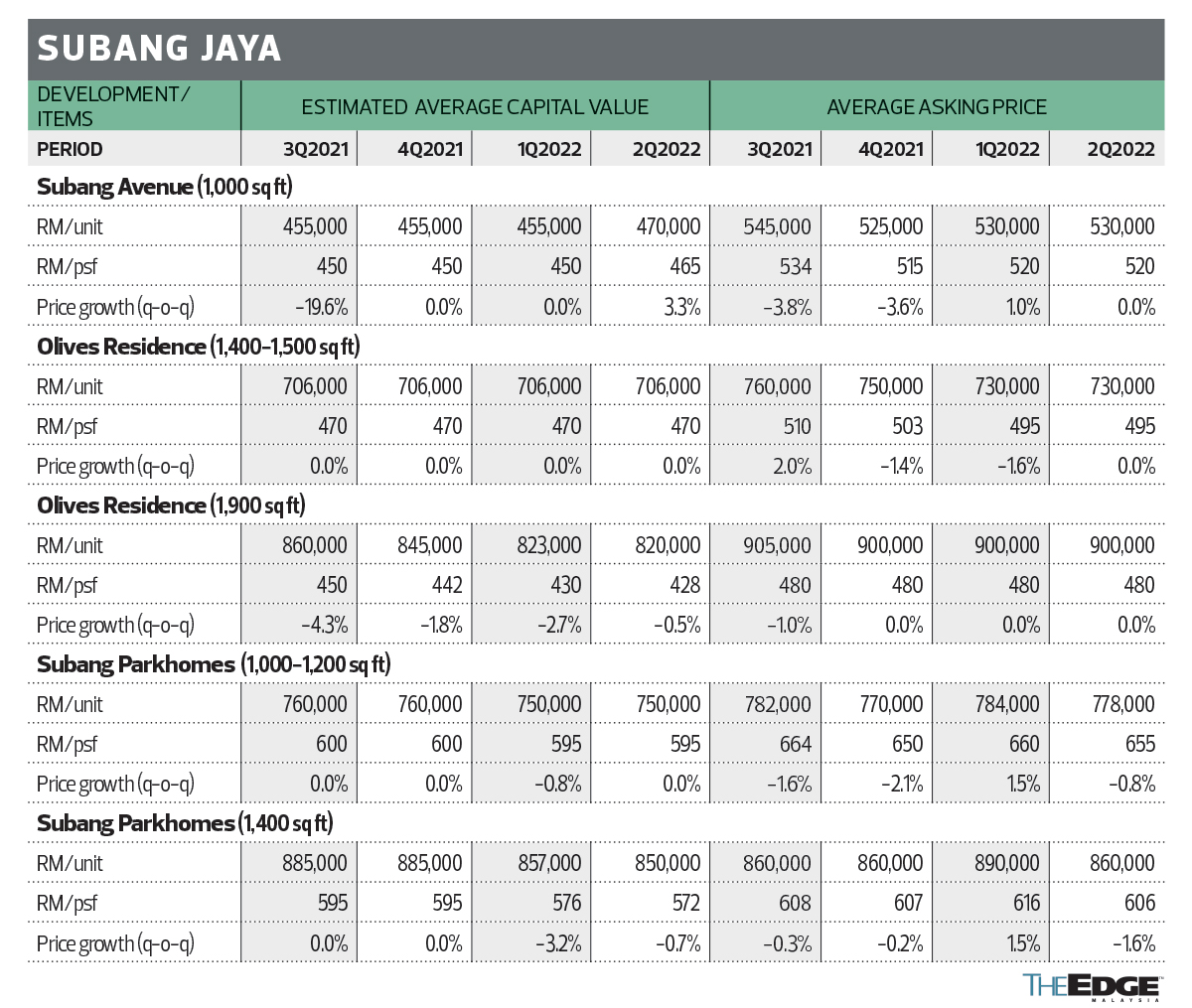

In Subang Jaya, the average capital value of the sampled units was down 6.1% y-o-y but up 0.4% q-o-q to RM506 psf in 2Q2022. The average asking price still hovered above RM550 psf during the quarter in review.

“While we expect the subsale market in Subang Jaya to remain challenging in the near term, we noticed growing buying interest in this area. Its freehold land status and amenity-rich location, including rail transport system, are always its selling points,” says Fong.

New projects in Subang Jaya include Aurora @ Subang Jaya City Centre (SJCC) by Sime Darby Property Bhd, Dorsett Place Waterfront by Mayland Valiant Sdn Bhd, Southplace Residences @ Tropicana Metropark by Tropicana Corp Bhd and Alira @ Tropicana Metropark by MCT Bhd.

The units at Aurora @ SJCC, which is slated for completion in 2023, are priced from RM740 psf, whereas those at Dorsett Place Subang Jaya, with built-ups ranging from 400 to 1,515 sq ft, are priced at about RM800 psf.

Southplace Residences @ Tropicana Metropark will comprise 656 units, with built-ups of 500 to 700 sq ft and priced at RM780 psf. This project is scheduled for completion in 2024.

Phase 1 of Alira @ Tropicana Metropark comprises 492 units, with built-ups ranging from 695 to 998 sq ft and priced at RM600 to RM700 psf. According to Fong, the project is reportedly over 85% sold and Phase 2 is open for sale.

In Bandar Sunway, the average capital value of the sampled units were unchanged q-o-q at RM575 psf but dropped 2.1% y-o-y. “Although the subsale market in this area was still inactive, asking prices stabilised during the quarter in review,” he says.

Newer developments in Bandar Sunway include Union Suites by Symphony Life and Greenfield Residence by Cicet Asia Development Sdn Bhd.

In Petaling Jaya, the average capital value of the sampled units was unchanged q-o-q but registered a decline of 1.3% y-o-y. The asking price also remained unchanged during the quarter in review.

Fong notes that the gap between capital values and asking prices in Petaling Jaya remained thin, indicating a buyer’s market in this amenity-rich location. “We also observed some units that are up for sale below the average market value.”

New launches in Petaling Jaya include Sunway D’Hill Residences by Sunway PKNS Sdn Bhd in Kota Damansara, Myara Park by Puncakdana Group in Ara Damansara, Mahogany Residences by Asian Pac Holdings Bhd in Kota Damansara, Stellar Damansara Jaya by OCR Group Bhd, Helix2 @ PJ South by Eupe Corp Bhd and Dwitara Residences @ Surya PJ South also by Asian Pac Holdings.

According to Fong, Stellar Damansara Jaya is offering 88 units, with built-ups from 2,000 sq ft and priced at RM750 to RM850 psf, whereas Helix2 targets first-time homebuyers with more compact unit sizes and selling prices from RM310,000. Selling prices at Dwitara Residences start from RM471 psf.

Other ongoing projects in Petaling Jaya include Tropicana Miyu by Tropicana Temokin Sdn Bhd in Section 17; Megah Rise by PPB Group Bhd in SS24, or Taman Megah; The Arcuz by Exsim Group, Sunway Serene by Sunway Property and Panorama Residences by LLC Properties Sdn Bhd in Kelana Jaya; The Mate by OCR Group Bhd in Damansara Jaya; Seapark Residences, also known as Ruby Seapark, by Midas De Sdn Bhd in Section 21; and Central Park Damansara by Exsim Group in Damansara Perdana.

Central Park Damansara has opened six phases for sale. They are D’Quince Residences with 1,310 units, D’Vervain Residences with 1,066 units, D’Cosmos Residences with 402 units, D’Erica Residences with 1,143 units, D’Clover Residences with 593 units and D’Terra Residences with 593 units.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Global funds hit pause on Indonesia after Prabowo policy changes

- Aaron Chia-Soh Wooi Yik claim their first-ever Badminton Asian Championship title

- Miti to present new analysis on impact of US tariffs at National Geo-Economic Action Council meeting on Monday

- Trump warns tariffs are coming for electronics after reprieve

- US, Asian stock futures rise after Trump pauses tech tariffs

- Olam to focus on food ingredients business, sell the rest

- Apple was on brink of crisis before Trump tariff concession

- Trump remains in ‘excellent health’, White House physician says

- London property faces worst hit from trade war, Rightmove says

- Bridgewater's Ray Dalio says Trump trade war has put US 'close to a recession'