This article first appeared in Personal Wealth, The Edge Malaysia Weekly on April 3, 2017 - April 9, 2017

BlackRock, the world’s biggest asset manager, says in its 2017 Global Investment Outlook that the global economy’s capacity for rapid growth is dented because of ageing populations, weak productivity growth and excess savings.

Goldman Sachs says in its 2017 Investment Outlook that it expects low returns from traditional exposures such as equities, credits and rates given three factors — elevated evaluations, limited upside for corporate earnings from current levels and limits to economic growth potential.

Gunasegaran Krishnan, a financial planner and the founder of Wealth Street, says: “What financial planners must do now is understand their clients’ risk tolerance level, risk perception and expected returns to help them achieve their financial goals. Then, they need to rebalance their clients’ portfolios and invest in markets that have better gross domestic product growth.”

An extended period of low returns means that investors need a longer period to accumulate savings for their retirement. Personal Wealth speaks to financial planners about their strategies for negotiating these treacherous waters.

NEGATIVE SENTIMENT OVERBLOWN

Local financial planners do not see the low-yield environment as a hindrance to retirement planning. They say all investors need to do is look for other opportunities.

Gavin Teoh, advisory and practice director at Standard Financial Adviser Sdn Bhd, believes that retirement planning must continue regardless of the market conditions. However, before recommending any strategies to his clients, he needs to manage their behaviour.

“By end-2015, I observed that many clients dared not invest. Only aggressive investors were still going ahead. To a layman, volatility and uncertainty correlate heavily with feelings. Therefore, some actually divest themselves of their investments and reinvest the money in properties, which they are more familiar with,” he says.

“My advice to clients is to stay firm. If you are irrational and emotional, there is a tendency to abandon your retirement planning, which results in terrible consequences. It makes more sense to adjust your current portfolio to taper your worries or negative emotions.”

Felix Neoh, vice-president of client advisory at Whitman Independent Advisors Sdn Bhd, says the negative sentiment is overblown. “Questions such as ‘Are we transitioning into a period of extended poor returns?’ or ‘Is market volatility expected to rise?’ are nothing new. We have been here before and we will be here again.

“The global, regional and local markets have rallied since November last year. The US markets are at an all-time high — the Dow Jones Industrial Average is above 20,000 points while the broader S&P 500 index is above 2,300 points — pulling most global markets along the same positive trajectory. Even our FBM KLCI is hovering at the 1,700-point level.

“There are still robust growth opportunities in many regions, across many sectors and asset classes. As such, save for an unexpected and prolonged global recession. Investors should ignore the short-term market noise and execute their long-term investment strategy. Buy ‘best of breed’ investments, invest in a diversified portfolio, monitor its performance and strategise when necessary to take profit.”

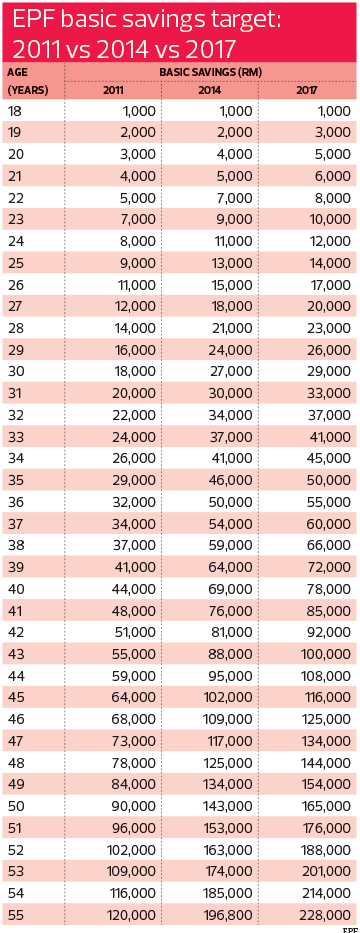

Neoh says if the money in your Employees Provident Fund account is your only source of retirement savings, then the downward trend in EPF dividends would be a concern. As it is, in 2015, two-thirds of EPF members aged 54 had less than RM50,000 in their accounts — way below the official minimum target of RM228,000 at age 55 set by the provident fund for its members. With dwindling dividends, escalating healthcare costs and inflation, these savings will disappear sooner than intended.

Gunasegaran says he is happy that EPF has approved unit trust funds that are fully invested offshore (with a minimum track record of three years). “Now, EPF members have access to more markets, which could give potentially better returns. For example, they can now move into emerging markets such as India.”

Thus, he says, if a financial planner knows how to properly rebalance their clients’ portfolios according to the market and can help clients see that long-term investing, say a minimum of 10 years, is a good period for them to lock in a particular strategy, then the current market does not mean anything.

ASSET ALLOCATION STRATEGIES

Whatever the market situation, the client’s risk tolerance and appetite must be taken into consideration. Financial planners must also consider their clients’ wealth, says Teoh.

“For instance, before 2015, I would recommend a 20% to 35% allocation to local equities. This included blue chips with the option of small-cap funds, as per clients’ risk tolerance. But after the drop in oil prices and other black swan events, I reduced the allocation for local equities to 15% and increased the allocation for regional (Asia) and global equities or equity income. Whatever the asset allocation is, it must reflect the client’s investment philosophy,” he says.

Teoh says he is not averse to local equities as one needs to have these stocks in their portfolio. “There is no forex risk with this and retirement is usually planned in the local context. Also, I believe that Malaysia is a defensive market and it is resilient.

“Because of all the negative news, people forget that the International Monetary Fund (IMF) expects positive economic growth from us, of 4.5% this year, a lower budget deficit of 3% of GDP, a positive current account balance and catalysts from mega infrastructure projects.”

He points out that every investor has his own level of loss aversion. “We all have a certain level of fear of loss. When a situation exceeds our accepted level, we begin to behave irrationally and do everything in our power to feel the opposite. Thus, from a psychology and risk management perspective, this will lead to the practice of speculation, which endangers their savings and retirement plan.”

One strategy that investors can employ is buy into local funds or assets in the construction, plantation and export sectors as they are anticipated to do well this year, he adds.

Neoh says the Pareto principle (80% of the results come from 20% of the investments) only holds true to a certain extent. “This principle is more suitable for conservative investors who wish to preserve their portfolio value or grow their portfolio at a slower but more stable pace, rather than grow the value of their investments over time.

“Say a Pareto-based portfolio generates an annualised return of only 4% per annum. It would take 18 years to double his investment. But with a diversified portfolio that matches his risk profile, a balanced investor could receive an annualised return of 8% per annum, thereby enabling him to double his money in just nine years.

“For example, a moderate risk investor might find it appropriate to invest 10% of his assets in low-risk investments (such as bonds, money market instruments and cash), 80% in moderate-risk investments (such as balanced funds and properties) and 10% in high-risk investments (such as growth funds or direct share investments).”

In more challenging market conditions, investors may opt to increase their holdings of defensive investments as a tactical move over a shorter period, says Neoh. But over the long term, they should remain true to their risk profile and utilise an asset allocation strategy that matches their risk tolerance.

The rule of thumb in investing, says Neoh, is to diversify your assets into different asset classes, geographic locations and currencies, in accordance with your risk profile. “Ultimately, clients will need to expose their investments to a higher level of risk in the bid to gain higher returns. But it should still be within their risk profile. Ideally, clients should only invest the funds they can set aside for at least three years and more, if they have already made provisions for their cash reserves.”

Also, as alternative investments are becoming easier for investors to access, they must find out everything before making the investment, he says. “Equities, bonds, properties, precious metals, resources and liquid assets are among the common asset classes that have withstood the test of time in helping investors grow their net worth. Alternative assets such as cryptocurrencies are considered high risk. As such, a moderate investor would best cap his investment at 10% allocation to this investable asset. The key is to invest within a measured percentage of asset allocation suitable to your risk profile.”

According to the Private Pension Administrator Malaysia, which oversees the Private Retirement Scheme (PRS), investors who are a long way from retirement should save one-third of their monthly income now to achieve two-thirds replacement income after retiring at age 60.

“If one contributes 11% of his salary to the EPF, then he should save at least another 22% for other investments. However, if you are only starting to save for retirement in your forties or fifties, then expect to save a much higher amount to achieve the two-thirds replacement income goal,” says Neoh.

He also recommends that working youths aged 20 to 30 should take advantage of the PRS Youth Incentive. Under Budget 2017, youths who contribute RM1,000 to the PRS in these two years will receive an incentive of RM1,000 from the government.

Meanwhile, EPF contributors can take advantage of the Members Investment Scheme to invest in approved funds to boost their overall retirement savings. “This is a golden opportunity for Malaysians to invest in approved foreign funds to increase their holdings in foreign assets and reduce their bias towards Malaysian-centric investments,” says Neoh.

Under normal market conditions, aggressive investors would be happy to see returns of 12% per annum while less aggressive investors would be pleased with 8%, he says. “But in challenging market conditions, investors face the dilemma of taking a higher level of risk than they are accustomed to in order to maintain their expected rate of return. As markets eventually normalise, it pays to stay invested for the long term within your risk profile rather than make decisions based on temporary or short-term market conditions.”

He adds that if investors only want to invest in local equities, they must invest in the best performing equity funds in the market rather than stick with the best performer from a single fund manager. “In bullish market conditions, perhaps the performance difference between the two funds may be small. But in challenging market conditions, the performance difference could be glaring.”

Gunasegaran advises older investors to seek funds from abroad, especially emerging market ones. “In terms of targeted returns, when a return target of 10% is not achievable locally, go offshore where the markets are performing better. Some of the markets, such as emerging markets, are giving very good returns,” he says.

“India, for example, has been giving double-digit returns for the past three years. The country is expected to produce better returns as its policies change.”

He says for investors in the 40 to 45 age group who are seeking a return of 12% to 15%, he would allocate 80% of their portfolio to equities and 20% to fixed income. “For those with a moderate risk appetite and would be happy with a return of 8% to 10%, I would allocate 65% to 70% to equities and the rest to fixed income. For those with a low risk appetite and would be happy with a return of 6% to 8%, I would allocate 30% to 40% to equities and the balance to fixed income.”

Alfred Sek, managing director of Excellente Consultancy Sdn Bhd and president of the Association of Financial Advisers, says he also prefers investing in emerging markets as there is more potential for growth. “For example, India is growing and it has a huge population. Telecommunications company Reliance Jio Infocomm Ltd managed to secure 100 million subscribers in just 170 days. You cannot achieve this quantum in Malaysia.

“Vietnam, Cambodia, Thailand and Myanmar are good emerging markets to venture into as they are starting from a low base, thus there are more opportunities. I am not saying that Malaysia’s economy is no good, but the size of the population plays a role.”

When it comes to asset allocation, he says it depends on the client’s wealth, age and how liquid he wants the plan to be. “For someone conservative, I would allocate 50% to 60% to fixed-income funds, 30% to balanced funds and the rest to aggressive or growth funds. For those who are very risk averse, I would recommend putting their money in capital-protected investments.”

EARNING MORE VERSUS SAVING MORE

Neoh says four factors must be taken into consideration if you want to grow your wealth — increase your savings, increase the return on investment, reduce investment risk and reduce cost or expenditure.

“Your savings is your most powerful net worth builder. To increase your net worth exponentially, you need to invest. And to invest, you need to have capital. So, the more you save, the more investment capital you have at your disposal,” he says.

“The higher the return on investment, the faster your net worth will grow. Employ effective investment strategies to diversify your investment portfolio to achieve targeted returns while reducing the volatility of investments.

“While you are taking active steps to grow your net worth, you also need to take measures to mitigate any risks of losing what you have already accumulated. Investors need to mindful of the different levels of risks they are exposed to and take the time to do research on the options available before parting with their hard-earned money.

“One should also strive to minimise all unnecessary costs that limit net worth growth. Costs can materialise in various guises — in the form of high financing rates and charges, unnecessary or overlapping insurance policies and high investment sales charges.”

Sek believes that one needs to save regardless of the market conditions. “Do not have the perception that you should only save when market conditions are bad. Make it a habit to save in good times and bad. Whatever it is, it depends on how much you earn and your commitments,” he says.

“If you are earning RM2,000 a month, 10% savings is RM200. If you are earning RM20,000, it is RM2,000. So, if you are able to increase your savings without putting yourself in a pinch, go ahead. If not, stick with the plan of saving 10% of your salary.”

Neoh says whether or not one should increase his savings is subjective. “If a client has limited financial resources and yet doubles his savings because he anticipates a shortfall in his retirement fund, then this invites financial catastrophe. However, if he has excess financial resources, then he should increase the quantum of his savings because a bigger nest egg is always better.”

In light of these circumstances, having multiple streams of income is beneficial as it provides an additional source of investment capital. Gunasegaran says the surplus from additional streams of income is the key to having a great retirement nest egg.

“Investors should seek multiple sources of income that will help them increase or double their savings for their investment accumulation strategy. I believe this is the key to having a great retirement lifestyle,” he says.

“Moving forward, people may want to look for jobs that are flexible, where they can work from home like in the developed markets. So, local companies should not forbid their employees from doing business outside their working hours. In this environment, you can no longer depend on a single income.”

Neoh says employees must take into consideration their employers’ policies and views with regards to this. “I think the guiding principle is that these activities should not encroach on company time or be at the expense of company resources, or result in any conflicts of interest. If it meets this principle, then my personal view is that it should not be an issue.

“Nevertheless, I feel that perhaps it is timely for the government/Ministry of Human Resources to step in to formalise this. After all, it is a growing trend and the reality is that many Malaysians will find it difficult to rely on a single source of income.

“The alternative, perhaps, would be to increase wages as a way of reducing the need for part-time work — a difficult proposition in these challenging market conditions. Otherwise, employers are better off formalising the option to work outside of office hours in order to establish clear guidelines for their employees to follow and minimise future disputes.”

MOVING FORWARD

As the ageing population increases, financial planners think there will be a corresponding rise in annuity products as well as the need for elderly care. Teoh says in Japan, which has the highest number of elderly in the world, insurance companies are involved in aged care.

“So, when the insured retires or approaches old age, the insurance companies there have products that pay for their lodgings and the services they require. I hope this will catch on in Malaysia,” he says.

However, Neoh cautions that annuities should not be the only means of retirement funding. “Annuities are more common in developed markets than in countries such as Malaysia. While there are merits for retirees to consider annuities as a means of ensuring the stability of their cash flow to fund their retirement needs, there are risks to relying solely on annuities as the only means of funding one’s retirement.

“Some of the concerns raised are the lack of liquidity (Can you cancel your annuity and get back a fair value?), low returns (Does it keep pace with the real rate of return?), early death (What happens to the investment principal if the annuitant dies soon after setting up the annuity?) and costs (Are low-cost investment products more cost-efficient?).

“However, there has been an increase in the development of more consumer-friendly annuity structures such as fixed indexed annuities that offer a guaranteed minimum income benefit and the chance of principal upside pegged to a market-based index.”

Sek says a number of developers in Malaysia are toying with the idea of building a communal home care, where they have hospitals or healthcare facilities within a housing community. “In countries with a growing ageing population, there is a demand for this. Perhaps we will see infrastructure like this in Malaysia in the future and the cost to live in these communities could be factored into retirement plans.”

From an asset manager’s perspective

Jason Chong, chief investment officer and managing director at Manulife Asset Management Services Bhd, says as the market has been volatile the last couple of years, the company has launched new mandates to meet changing client needs.

“We have put in a feature to give fund managers more flexibility to switch between equities, fixed income and cash. And if all hell breaks loose, they can hold cash. In the past, funds were benchmarked against an index. As a fund manager, your key performance indicator is to outperform the benchmark,” he says.

“As returns have been negative in the past few years, if your fund is down 2% and the market is down 5%, you have done a good job. But of course, investors will be unhappy as the returns are still negative. Thus, investment styles are moving towards seeking absolute returns or total returns, as opposed to relative returns.”

Chong says this impacts retirement planning as financial planners need to get their clients to adjust their expectations. “The most important point is that investors need to accept that returns are going to be lower going forward. Gone are the days when you could expect your [local] funds to give a return of 10% to 12% per annum consistently.

“So, because of lower expected returns, an investor saving for retirement will have to start saving earlier or else he will never meet his financial objectives. For example, healthcare costs are growing at 12% per annum. If you do not start saving earlier, you will not be able to keep up with the cost escalation. So, if you only start investing 10 years before retirement, I think it is too late.”

He says the man in the street can apply the rule of 72 — a rough calculation to see how many years they need to double their money. “If you put your money in a fixed deposit with a 3% annual return, it will take you 24 years to double your money (72 divided by 3). If a fund can give you, say, an average return of 6% to 8% per annum over the medium to long term, it will take you 9 to 12 years to double your money.”

Investors could consider alternative assets as a diversification tool. Chong says Manulife is ahead of the curve and has long invested in alternative investments in areas such as agriculture.

“Do you know that we are the largest owner of timberland and farmland in the world? The global population is growing and people still need to eat. These are long gestation projects, but they are more tangible and you can see where your money is going. As resources are becoming scarcer, these kinds of investments will pay off over time. Agriculture is here to stay. However, this fund is not available in Malaysia yet.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.