This article first appeared in The Edge Malaysia Weekly on June 20, 2022 - June 26, 2022

ALL eyes are on RHB Banking Group’s newly minted group managing director (MD) and group CEO Mohd Rashid Mohamad as he steers the fourth-largest banking group by assets forward in a tough operating landscape.

“It’s very challenging, especially now in a fast-changing market environment, and as we face potential risks such as geopolitical and inflationary,” acknowledges Rashid in his first exclusive interview as group MD/CEO.

Competition has intensified, given new entrants into the market, which are not just new banks but also technology companies that compete for the same pie. Rashid adds that this has partly affected the profitability of the industry, along with many other factors.

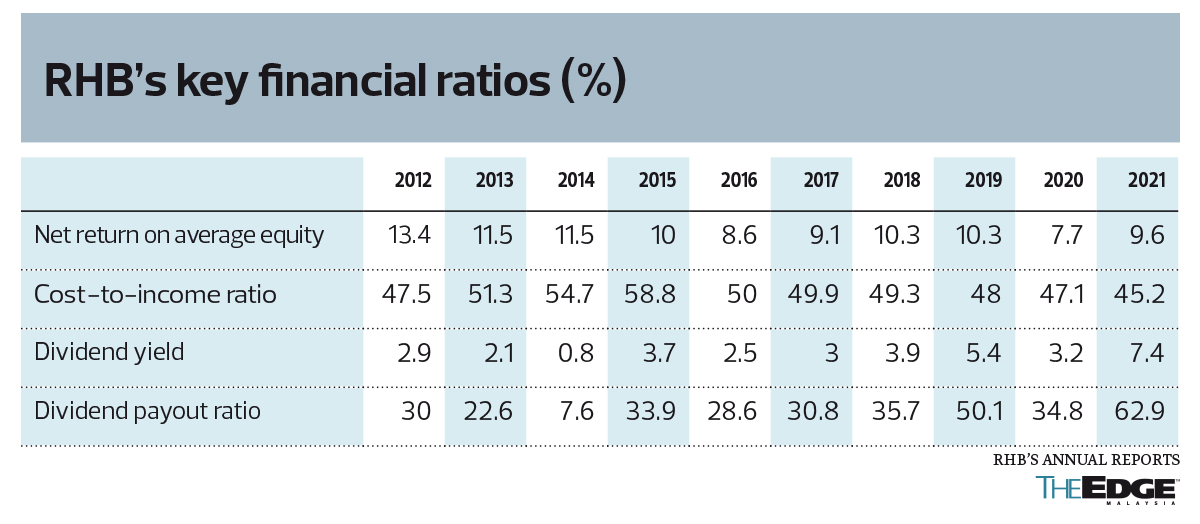

He notes that banks globally no longer see “high ROEs” as before. For RHB Bank Bhd, its return on equity (ROE) in the past 10 financial years hit a high of 13.4% in FY2012 before falling to a low of 7.7% in FY2020 and improving to 9.6% in FY2021 (see chart).

“What is important is that customers’ expectations have rapidly changed,” he says.

As such, Rashid believes that providing excellent service is very important. “This is why when we announced Together We Progress 24 [TWP24] — we want to anchor [it] on how we serve our customers better. Customer experience is important, service excellence is key.”

TWP24, RHB’s three-year corporate strategy (2022-2024), is aimed at driving the group’s ambition to be a leader in service excellence in line with its new purpose statement of “Making Progress Happen for Everyone”, centred around three strategic objectives: be everyone’s primary bank, prioritise customer experience and drive quality growth.

“This is where I want to put more emphasis, over the next three years. I’ve given my commitment, and the senior management is also committed — that we want to be the best service bank, that’s the aim,” he adds.

A number of key targets have been set, including an ROE of 11.5% from 9.6% currently and cost-to-income ratio (CIR) of 44.5% or less by 2024 (from 45.2% as at end-2021) as well as non-financial targets, such as having at least 65% of its systems modernised, at least 50% of its processes automated and over 95% of its transactions digitalised, all by 2024.

Its sustainability targets include mobilising RM20 billion into sustainable financial services and a financial inclusion target of empowering two million people by 2026, and for the group to become carbon neutral by 2030.

TWP24 comes after the completion of RHB’s five-year corporate strategy FIT22 (Fund Our Journey, Invest to Win and Transform the Organisation), which aimed to strengthen its presence in Malaysia while focusing on its strength overseas and building a winning operating model through digital transformation.

Rashid explains that RHB is looking at a three-year horizon for TWP24 rather than the typical five years. “We also need to appreciate market agility, the fast-changing business environment and customer expectations. The next three years will be important.”

“FIT22 has helped us fix some of the basics over the last five years and it was focused more on domestic business. Foundations were put in place and now, we just need to grow,” he adds.

Under TWP24 and as part of RHB’s efforts to enhance service excellence, Rashid says the bank will commit over RM500 million for IT, digital and culture training, which includes over RM400 million in capital expenditure for IT and digital modernisation initiatives and over RM100 million in operational improvement spend (including Smart Automation initiatives) and service culture training across the next three years.

“Service is a space that perhaps we can still win. If you ask me, if I want to be the biggest bank, most profitable bank in town? To be more realistic, other banks are also growing. Can I outbid the biggest bank in town? For now, maybe not. But we have to have the right vision.

“Becoming No 1 or 2 will be a consequence of serving our customers better. We want to become the primary bank of customers,” he says.

But every other bank will try to service their customers better — what would set RHB apart?

Rashid believes that many banks treat service as BAU (business as usual) and RHB wants to go beyond that by focusing on three main touchpoints: digital offerings, call centres and branches.

“The employee experience is also important. We recently launched a branch adoption programme where each senior management will adopt six or seven branches. We meet them physically, and hear from the branches their pain points and the operational burdens. It’s [about] going to the ground and gathering feedback from them, and improving our internal processes,” he adds.

RHB will also look into targeted segments that continues from FIT22. From a retail perspective, RHB will improve on the wealth management business, says Rashid, as the bank has observed that customers have been increasingly looking at investment avenues in the last three years.

“There’s no one product that fits every customer. It needs to be hyper-personalised,” he notes.

“We also want to focus on Islamic wealth management. We believe focus on that segment has not been addressed by many banks, but investor demand is there,” he adds, noting that the bank is targeting a three-year compound annual growth rate (CAGR) of 37% for Islamic investment and bancassurance AUM (assets under management) by 2024.

On this, Rashid says RHB will look at the entire Islamic wealth management ecosystem that will include saving, lending, borrowing, insurance protection and will management.

RHB will also focus on small- to mid-cap companies with targets to hit overall PLC (public limited company) client penetration of 80.6% (for mid-cap) and 76.2% (small-cap) by 2024. In 2017 to 2021, mid-cap penetration grew from 57.3% to 72.3% (15.0%). The group says the growth of mid-cap penetration will likely plateau once it approaches 85% to 90%.

“As such, we will be putting more focus on deepening our share of wallet with each client,” Rashid says.

Under TWP24, RHB also wants to focus on integrating its overseas business based on the hub and spoke model where the hub of business experts would serve the entire “overseas” country, depending on where the subject matter experts are.

RHB also targets a three-year CAGR of 14% for Singapore’s gross loans.

Currently, international operations account for about 12.6% of RHB’s gross loans — with Singapore contributing more than half of that — while the remaining 90% is contributed from home ground.

At home, RHB has always been associated with talk of potential mergers and acquisitions (M&A). What is Rashid’s position on banking M&As in the current environment?

“I believe that M&As or other inorganic opportunities are driven by business needs and considerations. If you’re asking me whether there is anything on the table right now, no, there is nothing. But would we as a team continue exploring? I think it’s only fair for us to look at opportunities if we want to grow inorganically. However, TWP24 is all about growing organically,” he says (see “No M&A plans on the table, but opportunities will be assessed” on Page 74).

On inorganic opportunities, RHB also has a 40% stake in the Boost-RHB JV digital bank, which also serves as a hedge against possible cannibalisation of its traditional business in the longer run, says Rashid (see “Digital banking venture a hedge against possible cannibalisation” on page 74).

Is highest dividend payout sustainable?

RHB rewarded shareholders with its highest-ever dividend payout in FY2021 following a good set of results. It paid a total dividend per share of 40 sen last year, which translates into a payout ratio of 63% (see chart).

Is this highest dividend payout one-off or is it sustainable?

Rashid says RHB has a dividend policy of a minimum of 30% of net profits. “Before the pandemic, we declared a dividend payout of 50.1% in FY2019. The first year of Covid-19, we declared less. However, if you look at the average of two years, that’s near to 50%. So the expectation perhaps normalised at 30% to 50%.”

“Of course, at the end of the day, it depends on how we perform. The better we perform, the more dividends we will share. We have the advantage of having a strong capital position.”

RHB’s capital ratio is one of the highest in the industry, with the group’s common equity tier-1 (CET-1) and total capital ratio at 16.8% and 19.4% respectively as at March 31, 2022.

Given this, would RHB pay more dividends moving forward?

Rashid says he has sat down with the management team to see how they can best put the capital to use.

“That is one key — that we want to expand. Sometimes, having a high capital ratio also indicates opportunities to expand our business further,” he says.

On putting the capital to better use, Rashid points out that TWP24 itself takes that into consideration. “Expanding into mid-cap and small-cap, I think, would put the capital to better use. That clearly requires higher RWA [risk weighted assets]. I’m not saying that we go down the credit curve, but based on our credit parameters, we basically diversify our credit exposure to mid-cap and small-cap,” he says.

RHB Bank’s net profit for FY2021 grew 28.8% to RM2.62 billion, surpassing pre-Covid-19 earnings of RM2.48 billion in FY2019.

Declining to give guidance on earnings, Rashid stresses that RHB aims to deliver ROE of 11.5% by 2024. On its target to improve CIR, he says that would involve more of growing income than cost-cutting initiatives. He assures that there will be no job cuts.

For FY2021, RHB saw mark-to-market losses of RM239 million. There is talk that such losses at RHB could be a lot larger this year, perhaps even start to increase in 2Q2022, given the interest-rate hike and spike in bond yields.

On this, Rashid comments: “High interest rates and bond yields would expose all financial institutions holding fixed income securities for regulatory, liquidity and investment purposes to adverse mark-to-market movements. In anticipation of a higher interest rate in 2022, we have adopted a defensive investment and trading strategy, and shall continuously rebalance our portfolio to manage our exposure within the approved limits.”

Asset quality better than pre-pandemic

Interestingly, Rashid shares that asset quality today is better than before the pandemic. “Before the pandemic, our GIL [gross impaired loans] ratio was at 1.97%. We closed the first quarter at 1.50%. This is despite seeing most of the repayment assistance ending in December 2021.”

“We monitor asset quality closely. The one thing that I can share with you, which is quite promising, is that of those that came out of this repayment assistance, 94% of our customers have started resuming their instalments,” he adds.

Rashid lists oil and gas, manufacturing, property and construction as well as hospitality as some corporate and commercial banking sectors that remain vulnerable following the Covid-19 pandemic.

As for SMEs, construction and hospitality remain vulnerable, he notes.

On the topic of rising fraud cases, Rashid says statistically, fraud cases in RHB have come down quite substantially over the period of 2020 to 2022. There were 1,594 fraud cases in 2020 and 736 cases in 2021.

“We have a dedicated 24/7 monitoring and detection team. This team monitors every transaction and also looks at the suspicious transactions. We also use a lot of data analytics to understand and identify demographics and trends. I think we have improved a lot in terms of fraud identification,” says Rashid.

TWP24 a game changer for RHB?

Analysts see TWP24 as a positive continuation of FIT22, but believe the jury is still out when it comes to whether the latest strategy will be a game changer.

“It’s good that they came up with the new strategy so fast … but that’s also partly due to Rashid being part of management during FIT22. That’s the beauty of this CEO appointment — that he is internal and there are few disruptions to BAU at the bank. Whether TWP24 is a game-changer remains to be seen ... It is more of a good continuation of FIT22,” says a head of research.

Another head of research was hoping for more “aggressive targets”, adding that the group seems to be “playing it safe”.

Nevertheless, the head of research at a foreign bank says RHB’s stock today remains “glaringly cheap” with a valuation of about 0.86 times price to book.

The sector’s average price-to-book ratio is 1.23 times for 2021 with Public Bank Bhd the highest at 1.82 times and Affin Bank the lowest at 0.41 times.

“RHB is still one of our top banking picks premised on the fact that they have a high capital position — so there is a lot of room to optimise the capital. The credit culture has also changed for the better there with asset quality remaining intact and they have done pretty well in managing cost and digital assets have been decent,” he notes.

“On areas of improvement — they have been losing market share in low-cost deposit franchises. So, they will need to fix that,” he adds.

RHB is also one of the top banking picks for CGS-CIMB Research “as its CY2022F dividend yield of 5.6% is among the highest in the sector, while its CY2022F P/E of 8.9x is attractive versus the sector’s 12.2x”.

In a June 15 report, CGS-CIMB Research regards RHB as one of the biggest beneficiaries of overnight policy rate (OPR) hikes among the big banks.

The local research house has an “add” call to the stock and a target price of RM7.70. Fourteen out of 17 analysts polled with Bloomberg have a “buy” on the stock, while two have a “hold” and only one has a “sell” with a 12-month consensus target price of RM6.82.

RHB’s stock closed at RM5.86 on Thursday, up 8.92% in the past year, and valuing the group at RM24.28 billion.

Digital banking venture a hedge against possible cannibalisation

Rapidly changing consumer needs and the entry of non-banking players into the financial sector have prompted RHB Bank Bhd to evolve to remain relevant, leading it to bid for the digital banking licence.

While some of RHB’s peers had partnered up with or taken a stake in e-wallet players, group managing director and group CEO Mohd Rashid Mohamad says RHB had yet to do so until its 60:40 joint venture (JV) with Axiata Group Bhd, via the latter’s fintech arm, Boost Holdings Sdn Bhd.

The JV is one of five entities that have been granted licences, the others being GXS Bank Pte Ltd-Kuok Brothers Sdn Bhd, Sea Ltd-YTL Digital Capital Sdn Bhd, AEON Financial Service Co Ltd-AEON Credit Service (M) Bhd-MoneyLion Inc consortia, and the consortium led by KAF Investment Bank Sdn Bhd.

He says RHB’s 40% stake in the Boost-RHB JV also acts as a hedge against the possible cannibalisation of its traditional business in the longer run.

“We cannot discount the possibility that the preferences of customers will be different in the long run.

“At the end of the day, we need to remain relevant. We need to evolve. If there are changes or threats or competition coming from different segments outside of traditional banking, we need to adapt,” Rashid says, noting that 93% of transactions by the bank’s customers were done digitally last year.

While some banks have said that they do not require the digital banking licence to compete in the digital banking space, Rashid says the decision to partner up with Boost was a deliberate move.

He says RHB could go it alone and take on the entire investment for the digital bank “experiment”, but having a partner in the venture means that the bank only needs to fork out 40% of the investment.

Rashid adds that the partnership with Boost also grants the bank the perspective of an external, non-banking player.

“If you look at us licence-wise, we could do it ourselves. But it’s not just about the licence — it’s also about getting ideas externally, rather than trying to figure it out by ourselves.

“That itself is differentiating us from our competitors,” he explains.

In a way, Rashid says the partnership creates an “internal competitor” for RHB, to push the bank further in its digital evolution. “It also means that we have first-hand insight into the development and evolution of services in the [non-bank financial services] segment, and if something is proven to work, we will have the advantage of replicating it in RHB.”

He adds that the partnership is an extension of RHB’s existing digital transformation, which enables the bank to find new ways of developing digital products faster.

Asked if there is space in the market for digital banks, he replies that there is a reason why the central bank granted these licences, which is to address the underserved and unserved market, pointing out that there are still 10 million to 13 million underserved micro SMEs and individuals.

“These people are going to small credit lenders. When digital banks come into the picture, there will be an alternative channel for them, which is supervised by Bank Negara, with a lot more transparency. People will feel safer dealing with digital banks,” he says.

Moreover, Rashid adds that RHB is not currently serving this segment of the population and, therefore, the venture will allow the bank to serve those that are not well covered by traditional banks.

However, the interest rates charged by the digital bank would need to reflect the credit standing of the borrower, which could mean higher rates as these borrowers likely do not meet the requirements to obtain financing from traditional banks.

Besides that, the size of loans granted would not be as big as what the banks typically deal with, and the tenor of financing will be shorter, he adds.

Meanwhile, he clarifies that the JV company — currently being structured — will be a separate legal entity from RHB and have a separate management. RHB will have representation on the board, although the details are still being worked out.

The partners are also in the midst of finalising their capex requirements for the venture, Rashid says, pointing out that Bank Negara requires a minimum of RM100 million in paid-up capital.

Typically, he says, setting up a digital bank could cost between RM400 million and RM1 billion on average over a period of five to seven years.

Timeline-wise, the digital bank venture is expected to be set up within 12 to 18 months’ time — well within the 24 months allowed by Bank Negara.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Bukit Aman calls up corporate figures to assist in investigations on MBI's money trail — sources

- Affin Bank may come under investors' scrutiny for weakening capital position, RHB flags

- HK billionaire Lee Shau-Kee’s sons get control of US$10b Henderson stake

- Cuckoo launches Malaysia’s biggest IPO in seven months at RM1.29 per share

- Astro tests new record low as results disappoint, analysts flag uncertain future

- Fuel prices unchanged till April 2

- Electrician jailed, fined for cheating over TNB meter modification

- Chinese influencer deported from Taiwan for backing invasion

- FBM KLCI rises 0.29% to 1,518.05 on March 26, 2025

- Govt to expand Sumbangan Asas Rahmah initiative, benefiting 5.4 mil recipients from April