This article first appeared in The Edge Malaysia Weekly on August 1, 2022 - August 7, 2022

A growing number of small and medium enterprises (SMEs) are stepping forward to ask for assistance to cope with their loan repayments, according to Koong Lin Loong, treasurer-general and chairman of the SMEs committee at the Associated Chinese Chambers of Commerce and Industry of Malaysia (ACCCIM).

Koong tells The Edge that the financial impact on SMEs after more than two years of the Covid-19 pandemic, compounded by current hurdles such as rising raw material prices, high operating costs and labour shortages, have led to cash flow issues and forced many businesses to their knees.

“Many SMEs are in a bind as they may come to a point where they can no longer service their loans, yet their cash-strapped plight renders their businesses ineligible for new borrowings,” he says, adding that other SME groups lament similar concerns.

As it stands, moratoriums and repayment assistance plans offered by banks to SMEs affected by the pandemic — under the government’s Pemulih relief package last year — have come to an end. However, it is understood that the lenders continue to provide their own financial assistance schemes, if needed.

A survey by the National Chamber of Commerce and Industry of Malaysia (NCCIM) shows that 52.3% of its SME respondents face hitches when applying for working capital loans while the loan applications of 78.6% of micro enterprises and 63.6% of small enterprises are rejected.

A senior banker, who wishes to remain anonymous, tells The Edge that banks may have tightened their lending criteria for SMEs, but not to the extent that the businesses are unable to obtain financing. “It is more about being vigilant in their ability to collect, such that their cash flow cycle isn’t stuck. We continue to lend and we continue to stick to quite aggressive targets actually.”

Nevertheless, this senior banker and another whom The Edge spoke to separately, say the SME space is one that financial institutions are watching closely. “It is an area of concern, especially on the manufacturing side. The worry is that SMEs are facing issues with collection, so cash flow becomes a problem. You can already see that the inventory cycles are a lot slower,” says the first banker.

The loan repayment assistance programmes extended at the height of the pandemic were meant to provide some respite to SMEs. But now, with the economy having reopened, many businesses have not been able to transition back to their normal repayment schedules.

“The majority are actually not graduating out of their payment relief plan. That is a concern,” says the banker. “I believe that is being seen not just at our bank, but across many banks. It [the graduation] is coming through quite slowly and is an indicator that not everything is quite back to normal.”

The banker adds, “Given that, the other concern is whether banks can ‘price up’ [after the recent overnight policy rate (OPR) hike] for SMEs that took the payment restructuring. It is looking unlikely.”

The OPR has risen twice this year — by 25 basis points each on May 11 and July 6 — which resulted in banks increasing their lending rates.

Nevertheless, despite rising headwinds for SMEs, the banker does not expect to see an increase in SME delinquencies for now.

Kenanga Research senior analyst Clement Chua opines that should there be an uptick, the impact on banks will be minimal as they are still “sheltered” by substantial pre-emptive loan provisions and management overlays made in the last two years.

“Most banks are [understood to want to] abstain from performing write-backs until 2023 when, hopefully, clear and sustainable repayment trends are established. This is the tone set by the central bank,” he explains.

Indeed, the senior banker concurs that should there be a rise in delinquencies, the bank’s pre-emptive provisions thus far are “more than adequate” to cover them. “But there is always a worry, in the sense that you never quite know [whether things will get worse than expected].”

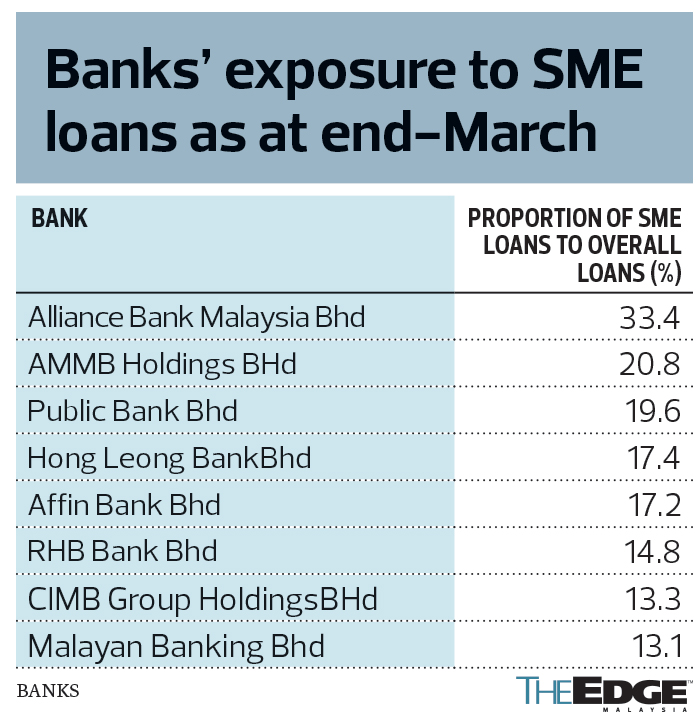

According to analysts, the banks with the highest SME mix in their loan portfolio are Alliance Bank Malaysia Bhd, AMMB Holdings Bhd, Public Bank Bhd and Hong Leong Bank Bhd (see table).

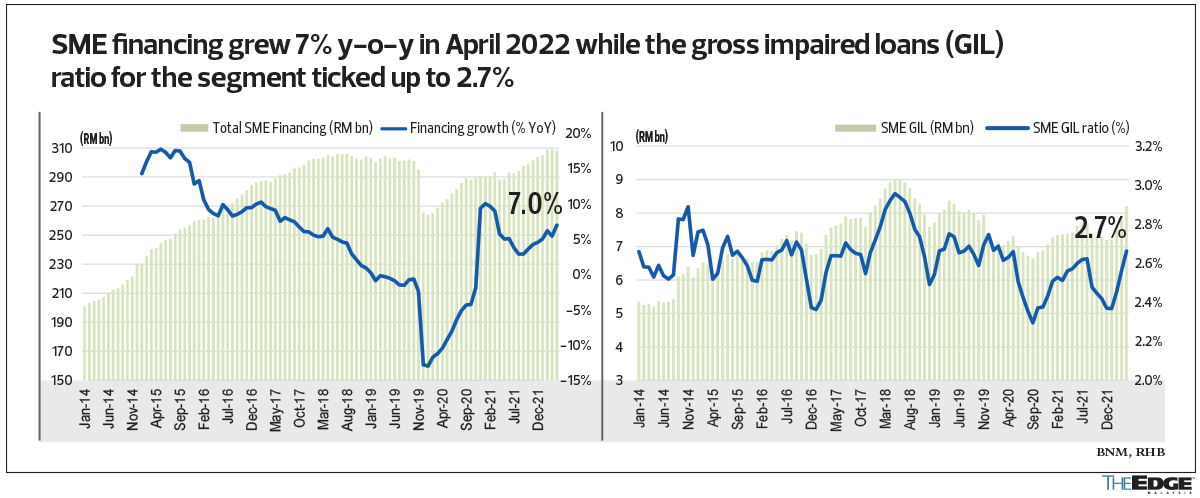

Bank Negara Malaysia data shows that SME loans in the banking system grew 7% year on year in April, but contracted 0.2% from the previous month. “Growth was primarily driven by the wholesale and retail trade sector, which was up 10.2% y-o-y (and down 0.2% month on month),” says RHB Research in a July 1 report.

Socio-Economic Research Centre executive director Lee Heng Guie points out that SMEs’ bankability has always been a “major contentious issue” because of their lack of proper documentation and financial statements. To plug financing gaps for SMEs, he recommends leveraging their annual tax submission forms to the Inland Revenue Board (LHDN) for an assessment of their bankability and creating a centralised system for SMEs to synchronise the loan applications.

“Establish an alternative financing platform to gather non-bank equity and venture capital financing modes. Innovative alternative financial instruments — whether based on debt, equity or even invoice-based financing — will be critical in meeting the needs of high-growth businesses across various phases of their life cycle,” Lee suggests.

Mismatch between product and need

For now, a pertinent problem is the mismatch between banking products and the needs of businesses, Koong opines.

For instance, an SME may need a sum for automation and digitalisation of its operations. But without the right loan product tailored to the SME’s needs, it has no choice but to take a conventional working capital loan — which commands a higher interest rate — from the bank.

“The higher cost of finance isn’t helpful to the business. Banks today are very selective. Unless applicants are able to give banks the assurance of their ability to comply with repayment terms, they will not get the help they need. And this is the crux of the problem — they are not able to give that assurance because their sales will not pick up quickly enough,” says Koong.

“This is an impossible situation, having just emerged from years of pandemic while the world is still fighting new variants of the coronavirus, and now facing the effects of higher inflation, interest rates and a geopolitical war. Banks need the confidence that SMEs are unable to offer during this difficult period.

“There are, of course, businesses that are favourable to banks such as furniture exporters, whose products are in constant demand, so much so that they have had to cut back due to the labour shortage. But since banks are able to see that these businesses’ order books remain high for the next 12 months, lending to the players in this sector is not an issue.

“Neither is lending to IT businesses that sell computers and accessories as demand has risen rapidly over the course of the pandemic. On the other hand, tourism and related industries face resistance from banks due to their high-risk nature.”

He notes that most SMES are cash-strapped, with many businesses operating on credit. “It is not that banks are unwilling to give out loans. First, with businesses facing a 60% cut in profitability, banks cannot take that risk. [Bear in mind that] banks do not get a share of the businesses’ profits when they give SMEs more time. Banks need to recoup their principal fast,” he adds.

Alternative means of financing

Meanwhile, it is not surprising that SMEs would seek alternative means of funding as alternative financing providers are able to offer faster turnaround times while having less stringent approval criteria than banks.

To that end, it is worth noting that peer-to-peer (P2P) financing players — such as digital supply-chain financing company Capital Bay (CapBay) and Fundaztic, in which property developer Paramount Corp Bhd has equity interest — have seen growth in their SME financing applications this year.

“Based on our engagement with businesses, SMEs are more aware of alternative financing, potentially due to the pandemic as well as the difficulties they face in obtaining financing via the conventional route,” says Fundaztic acting CEO and head of sales Jeff Tan.

Lending based on potential repayments instead of historical track record, fintech platforms’ agility and faster turnaround times, from first engagement to drawdown within 10 days compared with up to several months with banks, are the main reasons SMEs cite for borrowing from a P2P financing platform, he adds.

CapBay says it has seen consistent growth in applications over the course of the pandemic, while Fundaztic hit its highest disbursement rate in June.

“Towards the end of the first quarter (1Q2022) and going into 2Q, we saw 40% more applications than in 4Q2021, although we have to factor in the fact that we usually observe natural growth of 20% per quarter. With moratoriums from banks gradually tapering off, SMEs are looking for other means of financing. This is something for us to look into,” says CapBay CEO Ang Xing Xian.

CapBay, which has clientele predominantly reliant on public sector and government-linked-company projects, says a good number of its applicants are small companies with requests for capital expenditure and working capital funding ranging from RM250,000 to RM1 million, with interest charges going from 7% to 13%.

“Others have opted for [other] quick routes such as virtual credit cards, which advances cash to the company, while some simply use the conventional credit card as it is affordable [and easier] to just pay the 5% to 18% interest rate per annum,” says Koong.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.