This article first appeared in The Edge Malaysia Weekly on May 3, 2021 - May 9, 2021

PRITI Gathani has been in the restaurant business for the past nine years. Together with her partners, she operates four restaurants under WTF Restaurants Sdn Bhd. On March 13, the group opened its first grocery outlet in the affluent neighbourhood of Bangsar called The Hauz of Spize by WTF.

Gathani says although WTF had always been keen to venture into the grocery retail segment, it had not felt compelled to do so until now. “We realised that no matter what happened, people need their basic groceries,” she tells The Edge, referring to the Covid-19 pandemic and the imposition of the Movement Control Order (MCO), which kept people at home. “Many people have also turned into home chefs,” observes the proud owner of The Hauz of Spize by WTF, which offers fresh vegetables, organic food and hand-ground spices.

The WTF group and its business partner in this venture, Mike Udani, are planning to open a chain of grocery stores. They expect it will take eight months for the first store to see a return on investment.

WTF is not the only newcomer in the grocery retail sphere. QRA — a premium supermarket chain majority-owned by Charles Tseng@Charles Tseng Chia Chun (30.37%) and David Lee Tseng (28.89%) — has already opened two stores this year and will reportedly add more. Incidentally, both shareholders also own a stake in The Food Purveyor, which operates Village Grocer.

Just last month, Bursa Malaysia-listed MyNews Holdings Bhd brought in South Korea’s largest convenience store brand, CU, by BGF Retail Co Ltd. MyNews plans to open 500 stores in five years while e-government services provider MyEG Services Bhd, which had earlier announced an online grocery store called BELI, will be launching up to 50 physical stores within the next two years.

And the grocery retail scene is about to get a lot more interesting — and crowded — with real estate tycoon Tan Sri Desmond Lim Siew Choon investing in a super-premium grocer called The Food Merchant. The first of many more stores to come is slated for opening in the third quarter of the year (see ‘Desmond Lim bets on grocery business’).

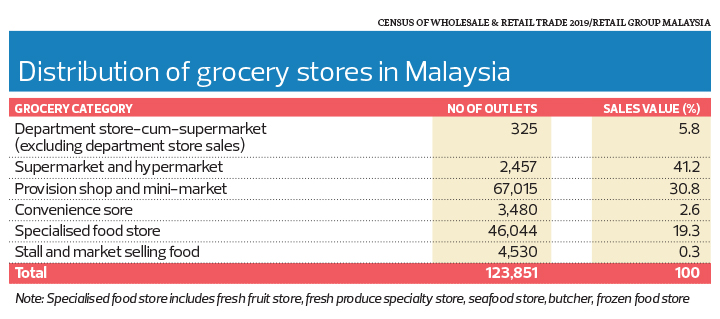

Apart from these new entrants and brands in the market, existing grocers are also expanding. Popular neighbourhood retailer 99 Speedmart plans to add an average of 25 stores a month, and KK Mart 10 a month (see “99 Speedmart and KK Super Mart hasten expansion).

The past year saw Tesco plc and Sime Darby Bhd selling their entire interest in Tesco Stores (M) Sdn Bhd to Thailand’s Charoen Pokphand Group’s (CP Group) CP Retail Development Co Ltd. The Tesco stores have since been renamed Lotus’s.

In December, Singapore-based private equity firm KV Asia Capital Pte Ltd exited from TF Value-Mart, which operates hypermarkets in secondary towns. The sale of the RM1.5 billion revenue business involved a management buyout, assisted by financing from Intermediate Capital Group plc.

What is driving the interest and prompting investors to plough billions of ringgit into the grocery retail segment, and is the Malaysian market large enough for so many players?

Data from Euromonitor International shows that the value of Malaysian grocery retailers was estimated at RM71.08 billion in 2020 and is projected to jump 30% to RM91.79 billion in 2025. It is expected to expand to RM74.74 billion this year (see table).

In its Retailing in Malaysia report (March 2021), the market research firm said that while non-grocery retailers were severely impacted by the pandemic, grocer retailers performed well, with the pandemic creating opportunities to revive and stimulate sales. “Several months of home seclusion and the closure of food service outlets forced consumers to cook at home, which boosted sales of grocery retailers, with home cooking trends also being driven by the rise in online cooking videos and demonstrations offering home-cooking inspiration.”

Retail Group Malaysia’s managing director Tan Hai Hsin agrees that the sudden interest in grocery retailing is a result of the pandemic. “Grocery operators (including supermarkets, hypermarkets, mini-markets, provision shops and wet markets) gained more during this pandemic period as dine-in was not permitted for many months.”

As Malaysians cook more at home, they are frequenting grocers more often. At the same time, consumers who want fewer items have shied away from crowds at larger stores, boosting the sales of smaller grocers. “Thus, mini-markets and independent food stores performed well during the pandemic period,” Tan adds.

But supermarkets have evolved too and are now more attractive to shoppers.

“The changing face and offerings of a typical supermarket has helped make the category very interesting and engaging as far as shopper experience is concerned,” Savills Malaysia associate director and head of retail services, Murli Menon, tells The Edge. He adds that more growth can be expected as operators innovate and upgrade their game to offer shoppers an improved and more diverse experience.

Supermarkets are typically a mall’s anchor tenant, and the role and significance of grocers was raised by the pandemic and restrictions during the MCO, says Murli, who notes that supermarkets were perhaps the only category of retailer that enjoyed a growth in sales during the period. “The impact of e-commerce on this category is also less compared to fashion, etc, given the logistics requirement to meet the expectations of a much shorter delivery lead time.”

Pandemic-proof and big enough for new players?

Judging by the number of new entrants into the grocery business and the performance of grocers over the past year, starting a grocery business appears to be worth a shot even though the segment is notorious for its extremely low margins.

Perhaps 2020 was unique, in that the pandemic boosted demand for groceries, which in turn helped several grocers to ring up record profits. For example, the net profit of Trendcell Sdn Bhd, the operator of Village Grocer, surged 143% to RM67.04 million, while that of KK Supermart & Superstore rose 87.05% to RM33.76 million. Both companies’ financial year end is June 30.

TF Value Mart also chalked up record net profits of RM60 million for the financial year ended Dec 31, 2020, from RM47 million in FY2019.

Tan does not think Malaysia’s market is big enough to accommodate the surge in new store openings, based on Walmart’s decision to not commence operations here when it surveyed the market years ago.

Murli thinks otherwise. He believes there is still room for growth in grocery retailing given that, on average, Malaysian homes spend a third of their monthly income on food and food-related expenses. But he cautions, “There is still room for consolidation and weeding out — to replace the weaker and non-efficient operators over a period of time, especially as economies of scale and introduction of newer technologies start to play a more important role.”

Not to be left behind, a number of upscale and premium grocers — including new entrant QRA and existing players such as Jaya Grocer, Village Grocer and Mercato — have also been opening or adding stores, prompting the question of whether Malaysians are affluent enough to support all these players.

“Definitely, no,” Tan declares, unless the premium supermarkets and mass-market grocers can compete on price. “If a premium supermarket is selling a basket of basic fresh food, fresh meat, canned food and general household items at the same prices as the hypermarket, they will continue to attract crowds.”

Moreover, he observes that affluent residents do not always shop at premium supermarkets. Pointing to Cold Storage as an example, he says it was considered a premium supermarket operator in Malaysia until the Asian financial crisis in 1998. But even before the emergence of competitors (such as Jaya Grocer, Village Grocer, Ben’s Independent Grocer), Tan says the market share of Cold Storage had been falling as its regular customers were shopping in mass-market grocery stores.

”While there is definitely a market for premium grocery retailing, premium supermarkets will always remain a niche given the local market size and average household income,” Murli opines. “Besides, consumers are becoming more and more value conscious across all categories — be it fashion/accessories or grocery shopping. The bigger chain operators are able to vary and adjust their product mix according to the catchment and hence able to straddle regular as well as premium categories as needed.”

But mergers and acquisitions and consolidation may be inevitable if the market becomes too saturated.

The Edge understands that several players are seeking buyers for their grocery business. One such player is Pahang-based Tunas Manja Group (TMG). It is learnt that the retailer, predominantly located in secondary towns, has approached other retailers regarding a sale. TMG, which has an estimated annual revenue of about RM1 billion, operates 64 stores under the brands of TMG Mart, TMG Express and TMG Plus. Tunas Manja Sdn Bhd’s shareholder and director Datuk Chin Yoke Kan did not respond to a query by The Edge seeking comments.

Etiqa Insurance and Takaful Bhd chief strategy officer Chris Eng foresees further consolidation in the industry. “It would appear that with a population of around 32 million, the Malaysian retail market is not large enough for so many players. As such, consolidation is expected to happen,” he tells The Edge.

“Even without the reimposition of a strict MCO, a rise in Covid-19 cases will lead to reduced outdoor mobility and may challenge the prospects of small convenience stores as Malaysians will prefer larger grocery stores to make less frequent grocery trips,” he says, pointing to the earnings of MyNews and QL Resources in 2020 (see “MyNews, 7-Eleven, Mr DIY are top picks for convenience, specialty stores”).

“As such, consolidation is likely to continue to happen in the larger hypermarkets and start to happen in the smaller convenience store space,” he adds.

Grocers suitable for Malaysia

Apart from new and improved online grocery shopping experiences, fresh grocery concepts can also be expected.

Tan believes that two concepts previously unsuccessful in Malaysia could make a comeback. One is the membership-only supermarket and the other, unmanned grocery stores.

Examples of the former include Makro from the Netherlands and Booker Cash & Carry from the UK — both had operated here — and Sam’s Club and Costco, which are now in Asia. These are discount supermarkets and wholesale supermarkets such as Lidl or Aldi, which sell goods in large quantities in multiple packs or large containers. Tan says AEON BiG, Mydin and NSK have started sections that allow shoppers to buy things in bulk.

On unmanned grocery stores, he says there were a few in the Klang Valley and Penang for a short period of time but they failed. These outlets were very popular in China too but shut down by the thousands a year later. In these stores, shoppers use their handphones to enter the store and make payment at the cashier’s counter themselves.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Petronas Gas, RHB Bank, Lien Hoe, Mayu Global, Binastra, Skygate, Tomei, Binasat, Aurelius Technologies, Kerjaya Prospek, Scope Industries, Keyfield International, Bank Rakyat

- Ahmad Shahril appointed as Bank Rakyat CEO

- At US antitrust trial, Meta's Zuckerberg admits he bought Instagram because it was 'better'

- Putrajaya has greenlit RM16.4b helicopter assembly plant in Melaka, says CM

- Scope Industries to exit manufacturing via RM96.7 mil sale of subsidiary

- US tariffs may cost chip equipment makers more than $1 billion, industry estimates

- US futures slide on Nvidia curbs, minerals probe

- Stocks halt rally amid lingering trade-war risks

- How much does Malaysia trade with the US?

- At US antitrust trial, Meta's Zuckerberg admits he bought Instagram because it was 'better'