This article first appeared in The Edge Malaysia Weekly on March 15, 2021 - March 21, 2021

EVEN though the outlook for cement producers has improved, the demand for their products remains uncertain, as major infrastructure projects proposed under Budget 2021 have yet to be implemented.

Some RM37 billion of direct infrastructure spending had been allocated in the budget to spur the economy over the short to long term. As at March, however, many major projects had yet to be launched or tenders awarded.

“Demand for cement has always been a function of projects, mega or otherwise. What has been lagging is the flow of projects since the start of Covid-19,” says an analyst covering the building materials industry.

The flow of construction jobs has been anaemic since last year, as some developers scaled back launches and public sector jobs, including mega infrastructure projects, have yet to be implemented.

Coupled with the scrapping of the Kuala Lumpur-Singapore High Speed Rail (HSR) project, the cement industry has yet to see any catalytic events that would result in higher demand for its products, according to observers.

“I can safely say that most players, be they contractors or cement players, are still waiting for Budget 2021 contracts to kick off at a steadier pace,” says the analyst. He hopes the second half will be a better period for the rollout of projects.

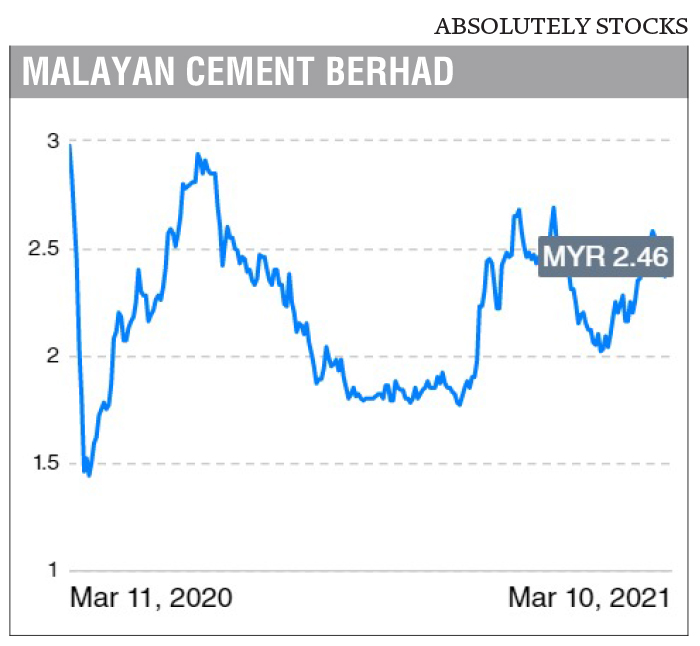

In the first half of the financial year ending June 30, 2021 (1HFY2021), Malayan Cement Bhd reported an operational profit of RM8.6 million. In the same six-month period in 2019, it reported a loss from operations of RM73.9 million.

The company had changed its financial year-end to June 30 from Dec 31.

However, owing to RM21.65 million in financial costs incurred during the six-month period, tax of RM1.74 million and share of results in a joint venture of RM8 million, it reported a net loss of RM6.8 million.

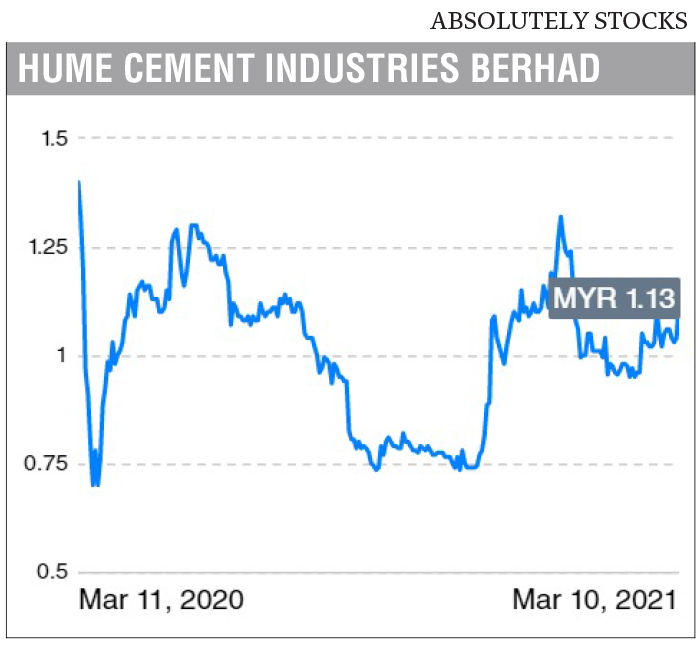

Hume Cement Industries Bhd (HCI) also reported an increase in profitability during the six-month period ended Dec 31, 2020 (1HFY2021). The group reported an operating profit of RM15.73 million during the period, compared with an operating loss of RM22.39 million in the corresponding period last year.

During the period under review, HCI reported a net profit of RM1.87 million, compared with a net loss of RM31.3 million in the corresponding period last year.

However, a closer look at the financial reports shows that the performance of cement producers has declined quarter on quarter. In the second quarter ended Dec 31, 2020, Malayan Cement made a RM3.76 million loss from operations, compared with a RM12.32 million profit in the preceding quarter.

The group said it recorded a profit in the first quarter because of cost-cutting and streamlining measures in operations, distributions and logistics undertaken by YTL Cement Bhd, its holding company.

The losses in 2QFY2021 were due to the decline in domestic cement sales volume, following the disruption of construction activities after the reinstatement of the Conditional Movement Control Order (CMCO) in November 2020.

However, HCI managed to remain in the black in 2QFY2021, but posted a lower net profit of RM331,000, compared with RM1.54 million in the preceding quarter.

The higher profitability of cement producers in the six-month period to end-December 2020, compared with the corresponding period in 2019, was partly because of lower energy costs. Moreover, they provided a lower rebate on the price of a bag of cement during the period.

The average price of bulk cement has hovered between RM200 and RM210 per tonne this year because of the disruption in construction activities due to the second MCO.

Hong Leong Investment Bank Research analyst Jeremy Goh, in a Feb 26 report on Malayan Cement, anticipates that the weak sales volume of cement will continue due to suboptimal productivity.

“Implementation of expansionary Budget 2021 remains a key catalyst for cement demand. However, budget execution remains uncertain, given the government’s focus on taming Covid-19, rollout of the vaccination programme and possible election in 2H2021,” he says.

Infrastructure players hope the budget allocated for the scrapped HSR project will be channelled towards other infrastructure projects.

The Master Builders Association Malaysia (MBAM) believes the budget could be channelled towards enhancing the Gemas-JB electrified double tracking project or towards the upgrade of the existing Keretapi Tanah Melayu Bhd Electric Train Service from Padang Besar to Gemas.

“This will not create any redundancy for domestic transportation but would still create some jobs for local construction players,” the association tells The Edge.

While MBAM understands that the bigger priority is to curb the spread of Covid-19, it hopes more jobs will be rolled out in a timely manner as high-impact infrastructure projects have a multiplier effect and can help revive the economy.

The local cement industry has been in the doldrums in the past five years as the economy expanded at sub-5%, except for 2017, when gross domestic product grew 5.8%. At the same time, it was beset with overcapacity, which led to slimmer margins.

Analysts had anticipated that 2020 would be the turning point for the industry, as there were several major infrastructure projects in the pipeline planned by the previous Barisan Nasional government.

The East Coast Rail Link, MRT Line 2 and 3, Pan Borneo Highway, HSR, Gemas-Johor Baru double-tracking project, and a few major property development projects were anticipated to raise the demand for cement.

However, those projects were put on hold for review by the Pakatan Harapan government after it won the 14th general election in May 2018. Another change in government in March 2020, along with the outbreak of the Covid-19 pandemic, effectively put an end to the anticipated revival in cement demand last year.

Currently, the declaration of a national emergency and political tensions between various camps in the Perikatan Nasional coalition appear to have hindered economic planning and infrastructure spending.

“Tok Pa (Minister of Economic Affairs Datuk Seri Mustapa Mohamed) recently said the 12th Malaysia Plan would be tabled when parliament reconvenes. I am not sure whether parliament will reconvene after the emergency is over,” another analyst tells The Edge.

“So, the situation (for the cement industry) is still status quo since the end of last year. It is best that we continue to monitor movements on the ground and not jump the gun.”

Sharizan Rosely, an analyst with CGSCIMB Research, says in a Feb 26 report that accelerated recovery in cement demand is unlikely to happen this year, owing to the timing of the rollout of key projects.

Nevertheless, the research firm continues to expect Malayan Cement’s earnings to turn around in the coming quarters on the back of gradual demand recovery, better average selling prices, and continued cost-efficiency measures.

The streamlining measures between YTL Cement and Malayan Cement have shown results. According to Sharizan, operating costs at Malayan Cement fell a steeper 29.2% in 1HFY2021 compared with the 21.3% fall in revenue.

At the same time, the group’s margins before interest, taxes, depreciation and amortisation improved to 11.8% compared with 1.9% in the corresponding period.

The rollout of Covid-19 vaccines has stirred hope of light at the end of the tunnel for the Malaysian economy. But it is unclear when demand for cement products will recover.

Malayan Cement’s share price has been hovering between RM1.98 and RM2.60 this year. The counter was trading at RM2.50 last Thursday, which translates into a price-to-book ratio of 0.9 times — a fair level, going by analysts’ targets. Both Goh of HLIB Research and Sharizan of CGSCIMB Research have a “hold” call on the stock, with a target price of RM2.49 and RM2.50 respectively.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Tesla’s retail fans buy the stock at a pace never seen before

- Five Malaysians charged in ‘pump-and-dump’ stock fraud scheme with US$214 mil seized

- MACC seeking Erdasan's suspended ED Mak Siew Wei to assist in investigation

- MAG's purchase of new Boeing aircraft strengthens Malaysia's position in global aviation industry — Zafrul

- Trump pulls security clearances for Kamala Harris, Hillary Clinton

- Pro-Trump senator meets China’s economy tsar amid trade tensions

- Bayer hit with US$2 bil Roundup verdict in US state of Georgia cancer case

- Japan, China, South Korea meet at geopolitical 'turning point in history'

- Trump pulls security clearances for Kamala Harris, Hillary Clinton

- Thailand drafts law to speed up US$29 bil transport link