This article first appeared in Capital, The Edge Malaysia Weekly on November 7, 2022 - November 13, 2022

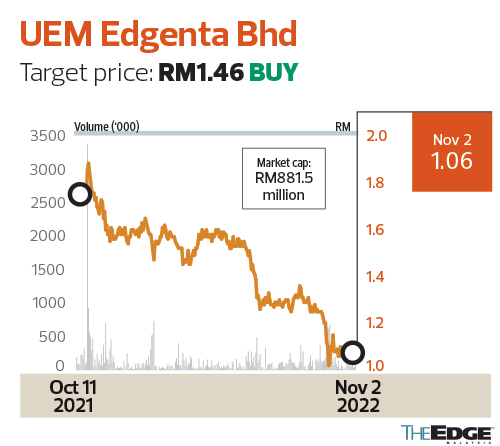

UEM Edgenta Bhd

Target price: RM1.46 BUY

RHB RESEARCH (OCT 31): UEME should see a pick-up in 2H22 top-line growth, underpinned by a seasonally stronger 4Q and its robust balance sheet (low gearing ratio of 0.1 times) that should support its dividend payout policy of 50% to 80%. While having cost escalation clauses in its contracts, management remains steadfast in optimising costs by incorporating technology-based solutions to increase productivity. UEME’s commercial order book from the healthcare segment inched up to 44% of the total healthcare order book versus the pre-Covid-19 pandemic’s 20% to 39%. Notwithstanding its ability to continue clinching new commercial contracts from overseas, the group is committed towards becoming a tech-enabled solutions provider in the healthcare services industry by 2025 via various offerings: (i) biomedical engineering maintenance services (BEMS); (ii) implementing mobile on-site testing facilities (MOSTFacs) for Covid-19 screening; and (iii) initiating a replacement through maintenance (RTM) programme for the Health Ministry’s medical equipment.

We expect healthcare to continue delivering stellar growth, underpinned by the return of patient visits to hospitals. UEME’s pioneering tech-enabled solutions should drive healthcare digitalisation while it moves up the value chain under its Edgenta of the Future 2025 (EoTF 2025) strategy.

Following the full reopening of the economy, we expect UEME to take full advantage of higher road maintenance and pavement works from PLUS Expressways Bhd on higher road traffic volumes. It expects stronger seasonality in 4Q, accounting for 30% of full-year revenue, as customers will attempt to utilise their annual budget towards the end of the year. UEME has secured 61% of its full-year order book target of RM1.2 billion to RM1.3 billion. Its order book stood at RM10.5 billion as at June and should provide the group with earnings visibility for the next four to five years.

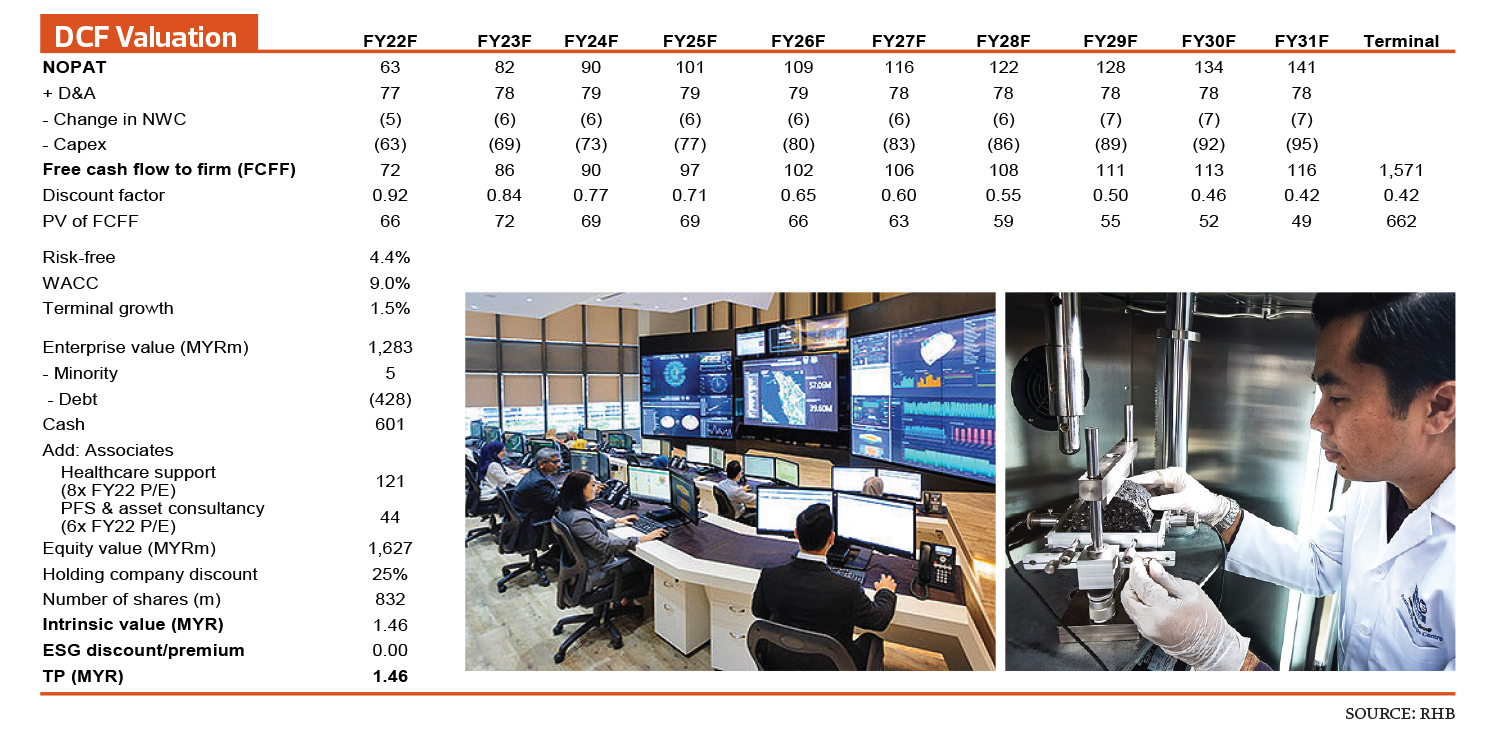

We reduce our earnings estimates for FY22F to FY23F by 6% and 1%, respectively, due to potential cost pressures weighing on their margins. We raise our rating on UEME to “buy” and set a new target price (TP) of RM1.46 with a 0% ESG premium/discount to our intrinsic value. Apart from being a key proxy for reopening borders, we see bargain valuations emerging, as UEME is currently trading at 11 times forward P/E, 1.2SD below its historical mean.

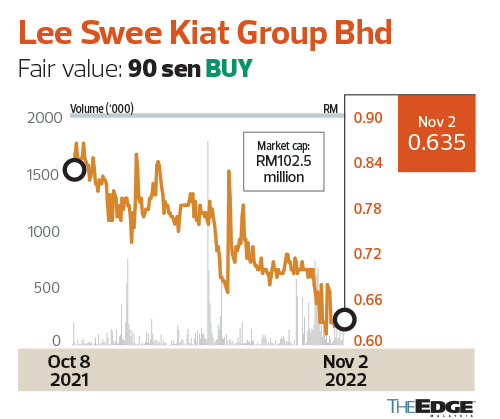

Lee Swee Kiat Group Bhd

Fair value: 90 sen BUY

AMINVESTMENT BANK (OCT 31): We maintain our “buy” call on LSK with a lower fair value of 90 sen per share, down from RM1 per share previously, based on an FY23F target PE of 11.7 times, at parity to its five-year median. The lower fair value is primarily due to lower earnings estimates, as we reduced FY22F to FY24F earnings by 8.1%/10%/7.5%, owing to the sales performance for the Cuckoo-Napure A-series mattresses falling short of expectations in FY21 and 9MFY22. The stock currently trades at a compelling FY23F PE of 8.2 times, which is an unjustified 30% discount to its five-year median of 11.7 times while offering a decent dividend yield of 4.8%.

LSK guided that domestic demand in October has started to exhibit some softness. LSK recorded total sales of 9,000-10,000 A-series mattresses in 9MFY22, which were 29% to 43% higher than the 7,000 achieved in FY21. However, this accounts for only 35% to 38% of management’s initial FY22F target of 26,000. LSK attributed the below-target performance to higher inflation and rising interest rates which dampened customers’ purchasing power. Hence, LSK lowered its FY22F target to 12,000-14,000 (46% to 54% downward revision).

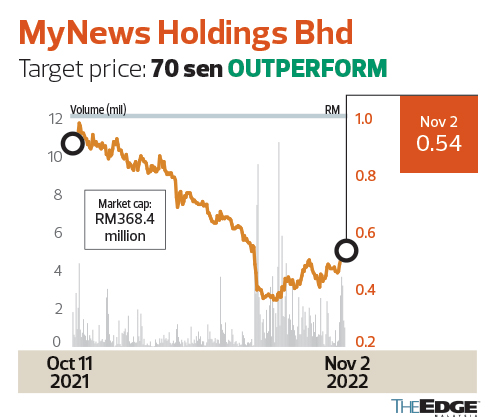

MyNews Holdings Bhd

Target price: 70 sen OUTPERFORM

KENANGA RESEARCH (OCT 31): MyNews guided its top-line and earnings momentum to be sustained into 4QFY22 (August to October 2022), driven by the return of shoppers, commuters and office crowds as economic activities gradually normalise to pre-pandemic levels. Recall that it reported a 21% q-o-q jump in top-line in 3QFY22 (May to July 2022) that helped to significantly narrow its net loss to RM1.5 million from RM10.2 million in the preceding quarter. It appeared even more confident that its food processing centre would turn around by 1QFY23, as utilisation at the loss-making unit rose further to 80% to 90% (from 60% to 65% one to two months ago), which is way above the breakeven level of 70%.

MyNews guided for store counts of 461 for MyNews and WHSmith, and 126 for CU as at end-FY22 (after factoring in the closure of four stores by FY22). We foresee a more aggressive store expansion plan by MyNews. Correspondingly, we upgrade our TP by 35% to 70 sen, from 52 sen, based on an unchanged 22 times FY23F PER, in line with the sector’s average forward multiple.

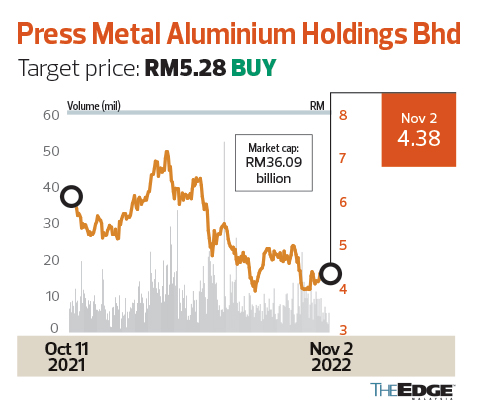

Press Metal Aluminium Holdings Bhd

Target price: RM5.28 BUY

HONG LEONG INVESTMENT BANK RESEARCH (OCT 31): PMETAL’s 3Q22 results are tentatively scheduled for release on Nov 29. We expect core earnings for the quarter to come in within the range of RM315 million to RM365 million (-11% to -23% q-o-q, +16% to 34% y-o-y), barring any unforeseen swings in cost structure. This is based on London Metal Exchange aluminium spot prices which averaged US$2,357 (RM11,174) per tonne in 3Q22 (versus the average of US$2,896/tonne in 2Q22 and US$2,652/tonne in 3Q21).

From Bloomberg data, we noticed a significant uptick in carbon anode prices — averaging at RMB6,532/tonne in 9M22 (which was a 66% increase from RMB3,943/tonne in 9M21). We highlight that carbon anode serves as a catalyst in the production of aluminium and is part of the production cost of PMETAL. With that, we are expecting some profit margin squeeze in 3Q22 earnings q-o-q, coupled with lower revenue due to the recent dip in aluminium spot prices.

Our 3Q22 core earnings estimate indicates that 9M22’s cumulative profits would range from RM1,145 million to RM1,195 million, signalling a 54% to 61% y-o-y growth from RM744 million in 9M22. This would make up about 74% to 77% of our FY22F full-year forecast and 71% to 74% of full-year consensus estimates.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.