This article first appeared in The Edge Malaysia Weekly on July 27, 2020 - August 2, 2020

AFTER three months of closure owing to the Covid-19 restrictions in Malaysia, number forecast operators (NFOs) reopened their outlets on June 17 to sturdy sales, reflecting pent-up demand and business resilience amid a weaker economy.

Berjaya Sports Toto Bhd told institutional investors recently that, only a month after re-opening, its sales per draw has recovered to 75%-80% of pre-closure levels.

“BST stated that sales are returning in tandem with footfall. Since reopening, sales/draw has been recovering by 4% to 5% per week,” Maybank Investment Bank Research says in a July 20 report after speaking to the company’s management. “That said, BST concedes that fewer foreigners have been betting due to the government restricting their movement. Locals have also been betting more with illegal NFOs for fear of going out and betting at NFO outlets. All the same, BST hopes to drive sales/draw to pre-closure levels soon.”

BST declined comment on emailed queries by The Edge.

BST is the largest legal NFO in Malaysia with an estimated 676 outlets. While Magnum Bhd — the other Bursa Malaysia-listed NFO — has not revealed the exact quantum of recovery in its NFO sales, analysts believe it to be similar to that of BST.

Not surprisingly, gaming analysts expect that NFOs’ earnings will recover to pre-Covid-19 levels faster than that of casino players.

“In terms of revenue recovery to pre-MCO (Movement Control Order) levels, we expect NFOs’ to be earlier than casinos due to the former’s closer proximity to customers, zero reliance on foreign tourist arrivals and fewer constraints in the implementation of SOP (standard operating procedure) measures,” says CGS-CIMB Research in a July 17 report on the gaming sector. It has “add” calls on both BST and Magnum.

It believes gross NFO sales may gradually recover to pre-MCO levels only by year-end, given stringent SOPs at outlets and potentially lower disposable incomes of punters. Note that Covid-19 has resulted in a wave of job and salary cuts.

Interestingly, some observers argue that people have a higher tendency to buy lottery tickets, which are “small-ticket” items, when worried about job security and income. This is one of the reasons the segment is recession-proof, they say.

But the segment is not without its challenges. Apart from the risk of a strong resurgence in the number of Covid-19 cases, which may result in the return of restrictions, there is also speculation that the government may impose a gaming tax hike as a way to increase tax revenue. The last time there was such a hike was 10 years ago, on July 1, 2010.

Additionally, there may be more special draws allowed. Special draws provide minimal earnings enhancement to NFOs and come with additional 10% tax. “We estimate that the NFO sector contributes RM2 billion in taxes a year. Special draws will help ‘claw back’ about RM0.5 billion in taxes foregone when NFO outlets were closed,” says Maybank IB.

According to Kenanga Research, in the three months that the NFO outlets were closed, BST had to cancel 40 draws in total, while Magnum cancelled 39 draws.

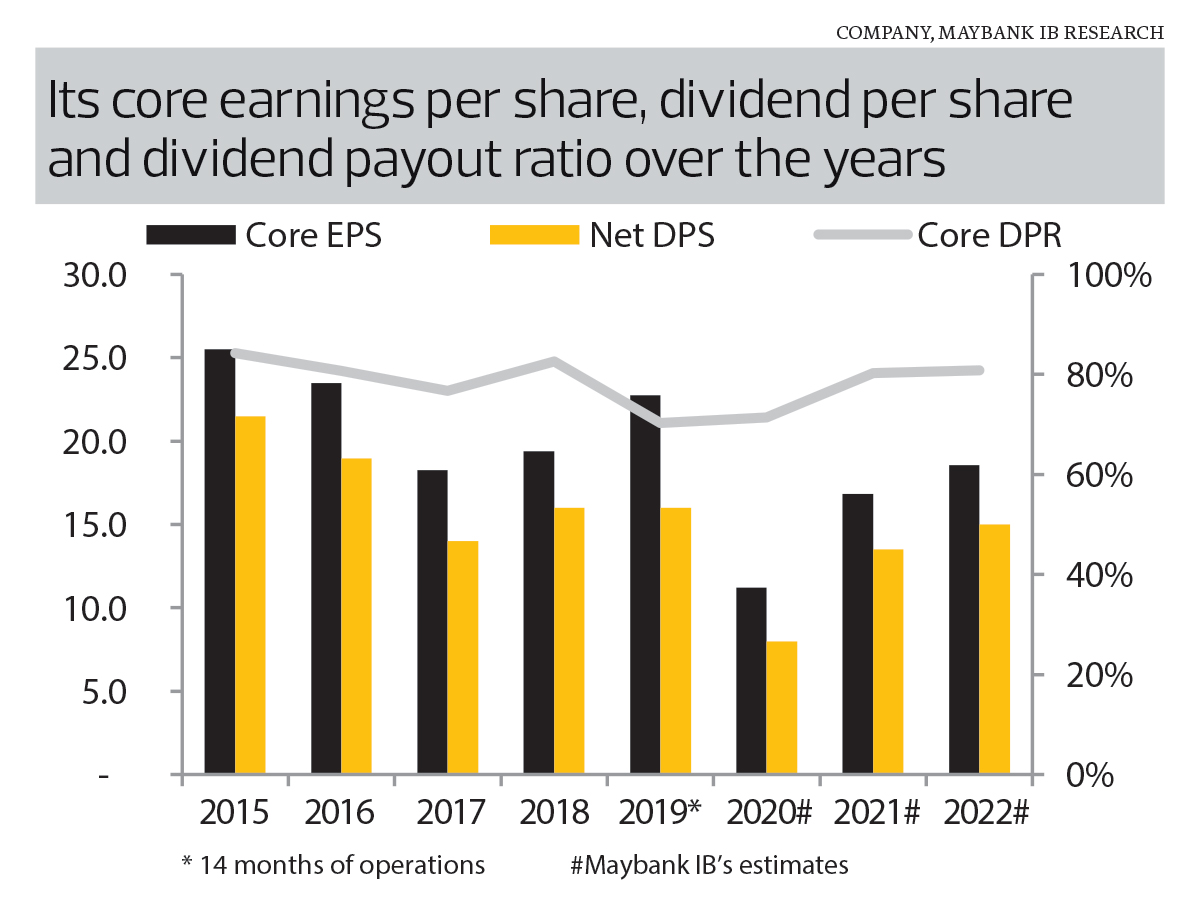

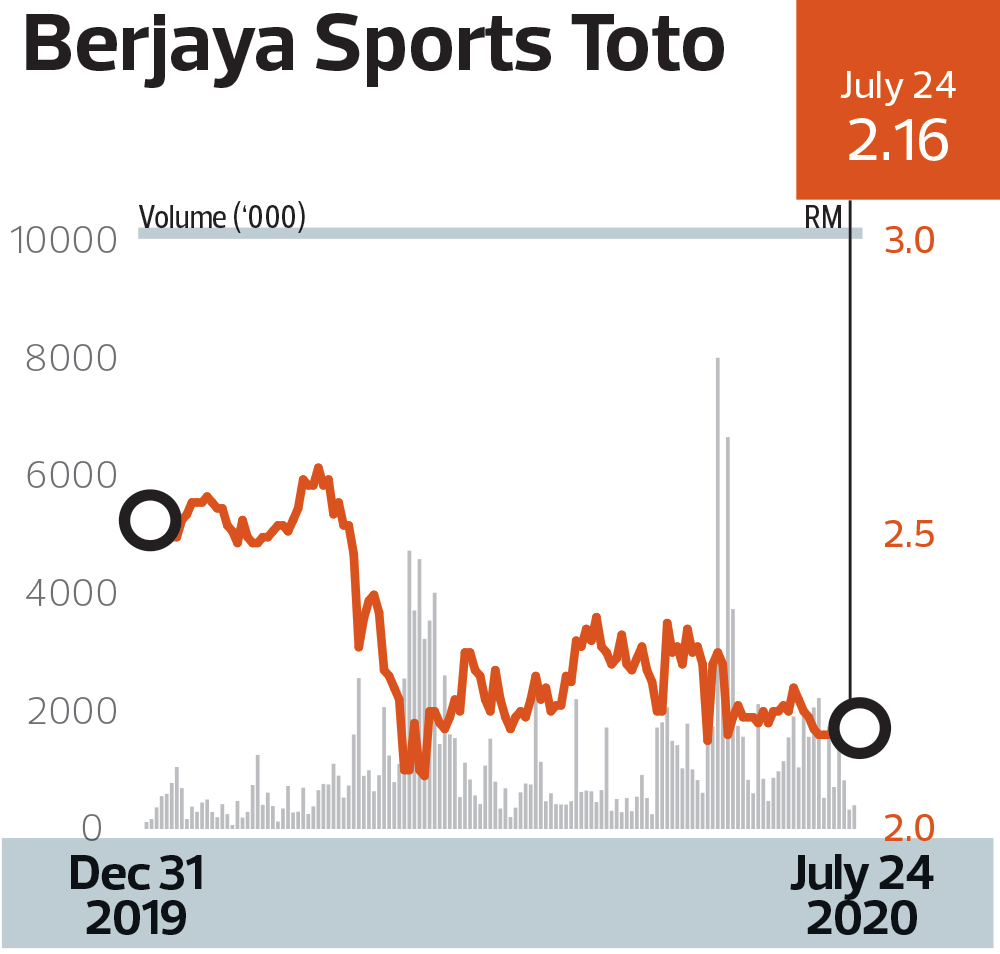

BST is Kenanga Research’s top stock pick in the gaming sector, with the target price pegged at RM2.55. The stock, which has shed 14.4% year to date to RM2.17 as at last Thursday, giving it a market capitalisation of RM2.9 billion, is liked for its resilient earnings and attractive dividend yield of about 7%.

At RM2.17, the stock is not too far off its recent lows, thus offering investors a timely opportunity to accumulate the shares, Kenanga says. It closed at a 52-week low of RM2.09 on March 19.

“BST’s selling point is its high dividend yield amid this low interest rate environment. People buy BST for dividends,” TA Securities analyst Tan Kam Meng tells The Edge. At RM2.17, the stock is trading at an attractive price-earnings ratio of about 11 times based on his projected earnings for FY2021. He projects an 8.3% yield.

Most analysts have a “buy” call on the stock despite the likelihood that BST may report a loss in the final quarter of its financial year ended June 30, 2020 (FY2020) — because of the outlet closures — and not be able to declare a final dividend.

Bloomberg data shows that of 11 analysts that track the stock, seven have a “buy” call while three have a “hold” and one, a “sell”. The average 12-month target price was RM2.54, which suggests further upside.

“We expect 4QFY2020 to be loss-making but recommend a ‘buy’ as we forecast dividends to resume from 1QFY2021,” says Maybank IB, which nevertheless cut the target price by 8 sen to RM2.80. It expects BST’s final quarter core net loss to come in at between RM15 million and RM20 million. For the full year, it sees the company making a stronger core net profit of RM226 million in FY2021 after an estimated RM151 million in FY2020.

BST has foreign operations, but the earnings contribution is small. BST’s 88%-owned motor dealership in the UK, known as H.R. Owen, reopened on June 1, but sales have been slow. “That said, BST expects its luxury car sales to recover faster than mainstream ones,” says Maybank IB. Apart from that, BST has a 35% stake in Philippine Gaming Management Corp, which remains shut.

For the nine months of FY2020, BST’s reported a net profit of RM177.5 million on the back RM4.18 billion in revenue. Cumulative dividend per share (DPS) stood at 8 sen. There are no year-ago comparison figures as the company changed its financial year-end last year to June from April. For the third quarter, net profit fell 21.5% q-o-q to RM48.6 million. It did not declare a dividend.

As for Magnum, of the six analysts that track the stock, five have a “buy” and one, a “hold”. The average 12-month target price was RM2.57, suggesting further upside from its RM2.20 closing last Thursday which gave it a market capitalisation of RM3.13 billion. The stock has shed 12.1% YTD.

Magnum reported a net profit of RM55.59 million for the first quarter of the financial year ending Dec 31, 2020, slightly down from RM60 million in the same quarter a year earlier. DPS fell to 2.5 sen from 4 sen.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.