This article first appeared in The Edge Financial Daily, on November 3, 2015.

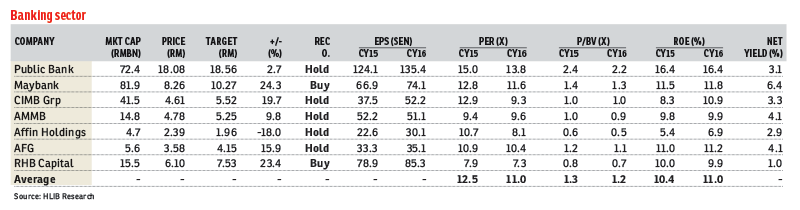

Banking sector

Maintain neutral with top picks being Malayan Banking Bhd and RHB Capital Bhd: Loan growth slowed to 9.7% year-on-year versus 10.2% in August, mainly attributed to the household segment, whereby growth slowed to 8.1% (from 8.3% in August) while business was sustained.

Leading indicators were mixed on a month-on-month (m-o-m) basis: number of applications lower but approvals higher. The approval rate remained below the 50% mark, but improved to 43.2% from the previous month’s all-time low of 41.6%.

The loan deposit ratio (LDR) and net LDR improved to 85.4% and 84.1% on Sep 15 respectively. Excess liquidity expanded RM242.8 billion on Sept 15. While liquidity was still ample to fund domestic economic growth, the higher LDR (albeit having declined on a m-o-m basis) could limit loan growth, albeit still supportive of credit expansion.

We keep our 2015 loan growth projection at 8% despite stronger year-to-date growth given a higher base, slower application growth, near-record-low approval rate and higher LDR. Expectations of a stronger business segment mitigating household slowdown materialised with challenges from internal and external headwinds, as well as weaker leading indicators.

Decline in the average lending rate to only five basis points above the all-time low, intense competition for deposits and the higher LDR will continue to exert pressure on margins.

Solid asset quality and capital ratios are intact to support growth and capital management, especially with dividend reinvestment plans.

Risks include a recession and its impact on asset quality, portfolio losses and non-interest income growth.

The banking sector is the best proxy for the 11th Malaysia Plan and the Refinery and Petrochemicals Integrated Development project, domestic consumption (albeit slower) and the economy; strong asset quality; robust capital ratios; and capital management.

Negatives include competitive pressure on margins, the goods and services tax’s impact on consumer sentiment, a tougher environment increasing chances of defaults and portfolio losses from foreign outflows. — Hong Leong IB Research, Nov 2

- Genting agrees to RM46m fine as part of settlement for complaint against its Las Vegas resort

- Lim Seong Hai Capital opens 17% lower on ACE Market debut

- Malaysia Airlines’ parent opts for 30 new Boeing aircraft for second stage of fleet renewal

- Top Glove faces rising risks from Chinese rivals, analysts flag after weaker-than-expected 2Q

- Nestlé Malaysia breaks ground for RM250m regional logistics hub in Port Klang

- Anwar urges amicable resolution to temple relocation issue

- Main Market-bound HI Mobility’s IPO shares oversubscribed by 6.6 times

- Salzgitter blames weak sales outlook on Germany's stagnation, trade tensions

- FBM KLCI up 0.09% to 1,505.45 on March 21, 2025

- Despite job cuts, VW still employs far more people than global rivals